Payroll tax obligations are the mandatory employer and employee contributions required by federal and state agencies to fund Social Security, Medicare, unemployment insurance, and income tax withholding. Every business with at least one employee must comply with these requirements, and the IRS enforces them through Form 941, Form 940, and W-2 filings. Getting payroll tax obligations explained clearly before you hire your first employee saves you from penalties, back taxes, and audits. This guide covers every layer: tax types, deposit schedules, reporting deadlines, and the compliance mistakes that cost small business owners the most.

What are the main types of payroll taxes and who pays them?

Payroll taxes fall into four main categories, and each one has a different payer, rate, and wage base. Knowing who owes what is the foundation of understanding payroll taxes correctly.

Federal income tax withholding comes entirely from the employee’s paycheck. You withhold the amount based on the employee’s Form W-4 and the IRS withholding tables. You never match this tax. You simply collect it and send it to the IRS on the employee’s behalf.

FICA taxes cover Social Security and Medicare. Both you and your employee split these equally. Social Security is taxed at 6.2% on each side, up to the 2026 wage base. Medicare is taxed at 1.45% on each side, with no wage cap. On top of that, employers must withhold an additional 0.9% Medicare surtax on wages over $200,000, paid by the employee only with no employer match. That surtax catches many small business owners off guard when a key employee crosses that threshold mid-year.

FUTA is the Federal Unemployment Tax Act tax, and it is paid entirely by you, the employer. The FUTA rate is 6.0% on the first $7,000 of wages per employee, but employers who pay state unemployment taxes on time receive up to a 5.4% credit, dropping the effective rate to just 0.6%. That credit is not automatic. You must stay current on your state unemployment tax payments to keep it.

SUTA is the State Unemployment Tax Act tax, also paid by the employer. Rates vary by state and by your company’s claims history. New employers typically receive an assigned rate until they build enough history for experience rating.

| Tax Type | Rate | Who Pays | Wage Base |

|---|---|---|---|

| Federal income tax withholding | Varies by W-4 | Employee only | No cap |

| Social Security (FICA) | 6.2% each | Employee + Employer | 2026 wage base |

| Medicare (FICA) | 1.45% each | Employee + Employer | No cap |

| Additional Medicare Tax | 0.9% | Employee only | Wages over $200,000 |

| FUTA | 0.6% effective | Employer only | First $7,000 per employee |

| SUTA | Varies by state | Employer only | Varies by state |

How do withholding, deposit schedules, and reporting work?

Withholding is the starting point, but depositing and reporting on time is where most small businesses run into trouble. The IRS assigns you a deposit schedule based on your tax liability in a prior 12-month period called the lookback period. New employers default to monthly depositors, while businesses with more than $50,000 in payroll tax liability during the lookback period move to a semiweekly schedule. That distinction matters because missing a semiweekly deadline by even one day triggers penalties.

All deposits must be made by electronic funds transfer through the IRS Electronic Federal Tax Payment System, known as EFTPS. Paper checks are not an option for most employers. Setting up EFTPS before your first payroll run is a non-negotiable step.

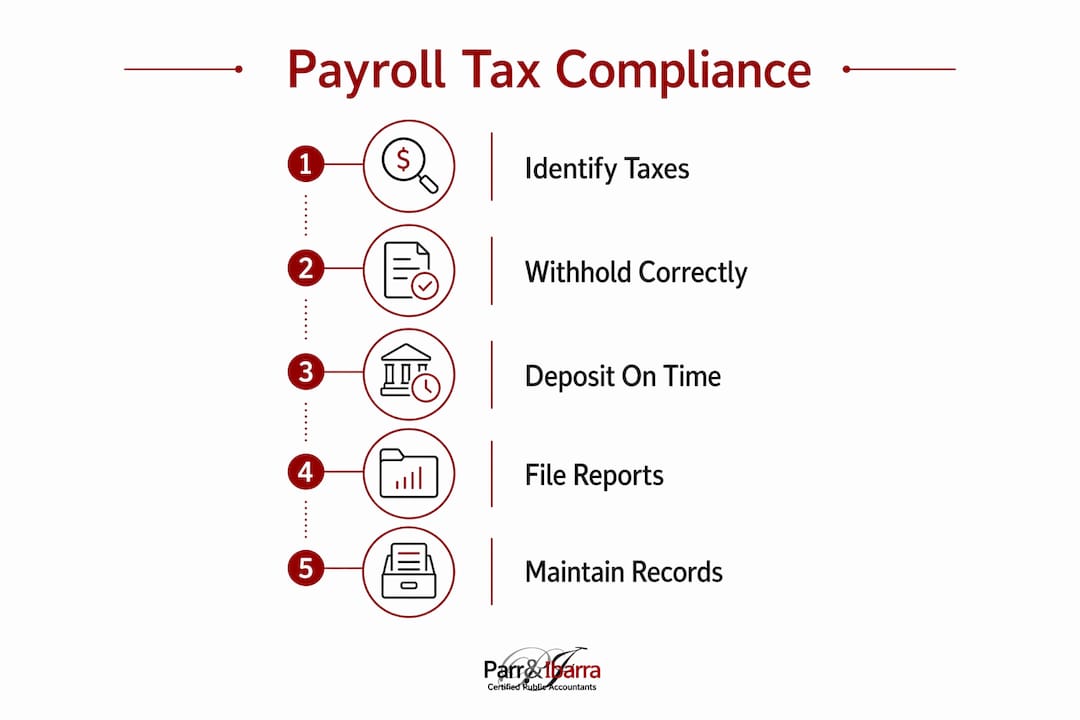

Here is the standard payroll tax processing sequence every small business owner should follow:

- Collect Form W-4 from each new employee before their first paycheck.

- Calculate withholding using the IRS Publication 15-T tables for federal income tax.

- Calculate FICA by applying 6.2% Social Security and 1.45% Medicare to both the employee and employer sides.

- Check for the Additional Medicare Tax threshold if any employee’s wages approach $200,000 in the calendar year.

- Deposit taxes via EFTPS according to your assigned monthly or semiweekly schedule.

- File Form 941 quarterly, which reconciles total wages, withheld taxes, and deposits. Form 941 is due on January 31, April 30, July 31, and October 31.

- File Form 940 annually by January 31 to report and pay any remaining FUTA liability.

- Distribute W-2s to employees and file copies with the Social Security Administration by January 31 of the following year.

Pro Tip: Set calendar reminders 10 days before each Form 941 due date and each EFTPS deposit deadline. A missed deposit costs you a percentage of the unpaid tax, and the penalty increases the longer the balance sits unpaid.

Check the essential tax deadlines calendar from Parr & Ibarra CPA to map every payroll filing date for the year in one place.

What are the most common payroll tax compliance pitfalls?

Payroll tax compliance failures rarely come from ignorance of the rates. They come from process breakdowns and wrong assumptions. These are the five mistakes that trigger the most IRS notices and penalties:

- Misclassifying workers as independent contractors. Worker misclassification is the top cause of payroll tax errors and audits. If the IRS reclassifies a contractor as an employee, you owe back taxes, penalties, and interest on every paycheck you issued without withholding.

- Using withheld taxes as operating cash. Withheld employee taxes are trust fund money. They belong to the IRS, not your business. Segregating withheld taxes into a dedicated account immediately after each payroll run prevents the temptation to use those funds for expenses.

- Ignoring remote employee work locations. Withholding is based on where the employee works, not where your office is located. A Dallas-based business with a remote employee in Colorado owes Colorado state income tax withholding. Failing to update employee locations creates multi-state compliance gaps.

- Assuming your payroll provider handles everything. The IRS holds you, the employer, legally responsible for payroll tax compliance even when you outsource to a payroll service. If your provider makes an error, you pay the penalty.

- Missing deposit deadlines. Penalties for late deposits include fines, interest, and potential legal action. The penalty rate starts at 2% for deposits one to five days late and climbs to 15% for amounts still unpaid more than 10 days after the IRS issues a notice.

Pro Tip: Open a separate bank account specifically for payroll taxes. Transfer the full employer and employee tax amounts on every pay date. This single habit eliminates the most common cash flow crisis in small business payroll.

How do payroll taxes affect your total labor costs?

Most small business owners budget for gross wages and forget the employer tax layer on top. Employer payroll taxes add 8%–15% on top of base salary costs due to FICA and unemployment taxes. That overhead is real money that must appear in your financial projections.

Here is what that looks like for a sample employee earning $60,000 per year:

| Employer Tax Component | Rate | Annual Cost |

|---|---|---|

| Social Security (employer share) | 6.2% | $3,720 |

| Medicare (employer share) | 1.45% | $870 |

| FUTA (effective rate) | 0.6% on $7,000 | $42 |

| SUTA (example at 2.7%) | 2.7% on state wage base | ~$540 |

| Total employer tax cost | ~$5,172 |

That $5,172 is on top of the $60,000 salary, bringing the true cost of that employee closer to $65,172 before benefits, equipment, or training. Payroll taxes are integral to labor cost management, and underestimating them is one of the most common budgeting errors in small business.

The good news is that employer-paid payroll taxes are deductible as business expenses on your federal return. The employer share of FICA, FUTA, and SUTA all reduce your taxable income. The employee withheld portions are not deductible by you. Only the amounts you pay as the employer qualify. Proper bookkeeping practices that separate employer tax costs from employee withholdings make this deduction straightforward at year end.

Key Takeaways

Payroll tax compliance requires knowing your tax types, depositing on schedule, filing Form 941 quarterly, and keeping employer tax funds separate from operating cash.

| Point | Details |

|---|---|

| Four core tax types | Federal withholding, FICA, FUTA, and SUTA each have distinct rates, payers, and wage bases. |

| Deposit schedule matters | The IRS assigns monthly or semiweekly schedules based on your lookback period liability. |

| Employer cost overhead | Employer payroll taxes add 8%–15% on top of gross wages, a critical budgeting factor. |

| Outsourcing does not transfer liability | You remain legally responsible for payroll tax accuracy even when using a payroll service. |

| Deductibility rule | Employer-paid FICA, FUTA, and SUTA are deductible; employee withheld taxes are not. |

Why payroll taxes deserve more than a checkbox

I have worked with dozens of small business owners in the Dallas-Fort Worth area who treat payroll taxes as a back-office chore. That mindset is expensive. The businesses that run into IRS trouble are almost never the ones who did not know the rates. They are the ones who knew the rules but let process slip during a busy quarter.

The single most effective habit I have seen is fund segregation. Owners who move payroll tax amounts into a separate account on every pay date never face the cash flow crisis of a large quarterly deposit they cannot cover. It sounds simple because it is. Simple disciplines prevent the most painful problems.

Remote work has added a real layer of complexity that many owners have not caught up with yet. If your team is spread across multiple states, your withholding obligations are spread across those states too. Payroll software like Gusto or ADP can track work locations automatically, but you still need to verify the setup is correct. Software does not replace your responsibility to understand the rules.

My advice is to review your payroll setup with a CPA at least once a year, not just at tax time. Rules change, wage bases adjust, and your workforce composition shifts. A one-hour review catches the gaps before the IRS does.

— Adan

Let Parr & Ibarra CPA handle your payroll tax compliance

Running payroll correctly takes more than software. It takes someone who knows the rules and watches the deadlines for you.

Parr & Ibarra CPA works with small business owners across the Dallas-Fort Worth area to manage payroll tax deposits, quarterly Form 941 filings, and year-end W-2 preparation. The team of over 20 professionals, including multiple CPAs, gives you the coverage of a large firm with the attention of a local partner. Start with the IRS tax filing guide to understand your federal obligations, then schedule a consultation with Parr & Ibarra CPA to build a payroll compliance plan that fits your business.

FAQ

What are payroll taxes, exactly?

Payroll taxes are mandatory contributions withheld from employee wages and paid by employers to fund Social Security, Medicare, federal unemployment insurance, and state programs. Both the employee and employer share responsibility for FICA taxes, while FUTA and SUTA are paid entirely by the employer.

How do I know if I am a monthly or semiweekly depositor?

The IRS assigns your deposit schedule based on your total payroll tax liability during a prior 12-month lookback period. Businesses with more than $50,000 in liability during that period are semiweekly depositors; all others, including new employers, default to monthly.

Can I be penalized if my payroll service makes a mistake?

Yes. The IRS holds employers legally responsible for payroll tax compliance regardless of whether a third-party payroll provider processes the payments. Errors made by your payroll service are still your liability.

Which payroll taxes can I deduct on my business return?

The employer share of FICA, FUTA, and SUTA are all deductible as business expenses. Employee withheld taxes are not deductible by the employer because those funds belong to the employee and are simply passed through to the IRS.

What happens if I miss a payroll tax deposit deadline?

Penalties start at 2% for deposits that are one to five days late and increase to 15% for balances unpaid more than 10 days after the IRS issues a notice. Interest accrues on top of penalties, making late deposits significantly more costly the longer they go unresolved.