IRS Tax Filing Guide, 2026: What Texas Business Owners and Dallas Entrepreneurs Need to Know

There’s a version of this conversation that happens every spring across Dallas. A business owner sits down with their accountant in March, hands over a folder of receipts, and somewhere in the middle of the meeting finds out they could have saved $20,000 if only they’d made a different call back in October. By March, that window is gone.

2026 is a year where that conversation could go very differently, because the tax code has changed in ways that genuinely favor business owners who plan ahead. Bonus depreciation is back at 100%. The SALT cap jumped from $10,000 to $40,000. The standard deduction for married filers is now $32,200. These aren’t minor inflation tweaks. They’re structural changes that require actual decisions, made before year-end.

This guide is written for Texas business owners, real estate investors, and high-income earners who want to understand what changed, why it matters for their specific situation, and what to do about it.

Tax Filing Is a Financial Strategy, Not a Paperwork Exercise

Most business owners think of tax filing as something that happens to them once a year. You gather your documents, hand them to someone, and hope the number at the end isn’t too painful. That mindset is expensive.

For anyone running a business, tax filing is inseparable from financial strategy. The entity you chose, how you compensate yourself, when you make purchases, how you classify expenses. All of it feeds into what you owe. And if no one is looking at those decisions through a tax lens throughout the year, you’re probably overpaying. A good starting point is simply evaluating whether your current tax situation is costing you more than it should.

For individuals, good filing means choosing the right status, capturing every deduction, and applying credits accurately. For businesses, it means understanding payroll obligations, calculating depreciation correctly, planning estimated payments, and making sure your records can actually support every line item on the return. The IRS has significantly improved its ability to find discrepancies. Digital payment tracking, third-party reporting, and algorithmic review tools mean that errors, accidental or otherwise, are easier to flag than they were five years ago. A clean, professionally prepared return isn’t just about compliance. It’s about not handing an auditor a reason to look closer.

Texas adds one more layer that catches people off guard. There’s no personal state income tax, which is a genuine advantage, but there is a franchise tax based on business revenue. Many small business owners assume their accountant is handling it. Make sure that assumption is confirmed, in writing, every year.

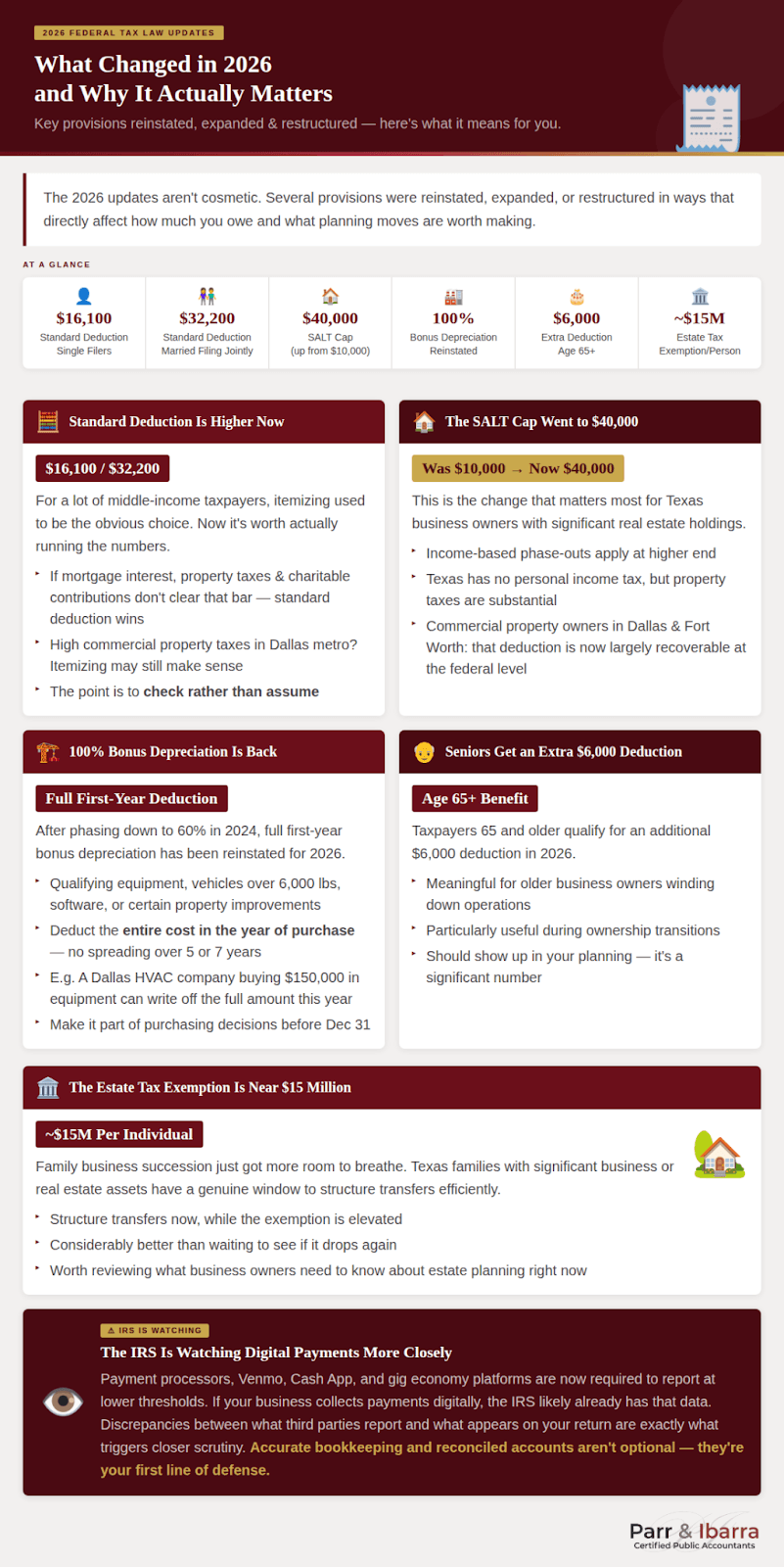

What Changed in 2026 and Why It Actually Matters

The 2026 updates aren’t cosmetic. Several provisions were reinstated, expanded, or restructured in ways that directly affect how much you owe and what planning moves are worth making. For a complete picture of how these changes interact with individual tax provisions, it’s worth reviewing the 2026 federal tax law updates before your next planning session.

Standard Deduction Is Higher Now

Single filers are at $16,100. Married couples filing jointly are at $32,200. For a lot of middle-income taxpayers, itemizing used to be the obvious choice. Now it’s worth actually running the numbers. If your mortgage interest, property taxes, and charitable contributions don’t clear that bar, the standard deduction wins. If they do, particularly if you have high commercial property taxes in the Dallas metro, itemizing still makes sense. The point is to check rather than assume.

The SALT Cap Went to $40,000

This is the change that matters most for Texas business owners with significant real estate holdings. The State and Local Tax deduction was stuck at $10,000 for years. It’s now $40,000, with income-based phase-outs at the higher end. Texas doesn’t have a personal income tax, but property taxes here are substantial, and commercial property owners in Dallas and Fort Worth know exactly how much that adds up to annually. That deduction is now largely recoverable at the federal level, which meaningfully changes the math for a lot of people.

100% Bonus Depreciation Is Back

This one is worth slowing down on. After phasing down to 60% in 2024, full first-year bonus depreciation has been reinstated for 2026. If your business buys qualifying equipment, vehicles over 6,000 pounds, software, or certain property improvements this year, you can deduct the entire cost in the year of purchase. No spreading it over five or seven years. A Dallas HVAC company buying $150,000 in new equipment can write off the full amount this year. That’s a strategy, not just a tax rule, and it needs to be part of your purchasing decisions before December 31.

Seniors Get an Extra $6,000 Deduction

Taxpayers 65 and older qualify for an additional $6,000 deduction in 2026. For older business owners winding down operations or transitioning ownership, this is a meaningful number that should show up in your planning.

The Estate Tax Exemption Is Near $15 Million

Family business succession just got more room to breathe. With the federal exemption at approximately $15 million per individual, Texas families with significant business or real estate assets have a genuine window to structure transfers efficiently. Understanding what business owners need to know about estate planning right now, while the exemption is elevated, is considerably better than waiting to see if it drops again.

The IRS Is Watching Digital Payments More Closely

Payment processors, platforms like Venmo and Cash App, and gig economy platforms are now required to report at lower thresholds than before. If your business collects payments digitally, the IRS likely already has that data. Discrepancies between what third parties report and what appears on your return are exactly what triggers closer scrutiny. Accurate bookkeeping and reconciled accounts aren’t optional at this point. They’re your first line of defense.

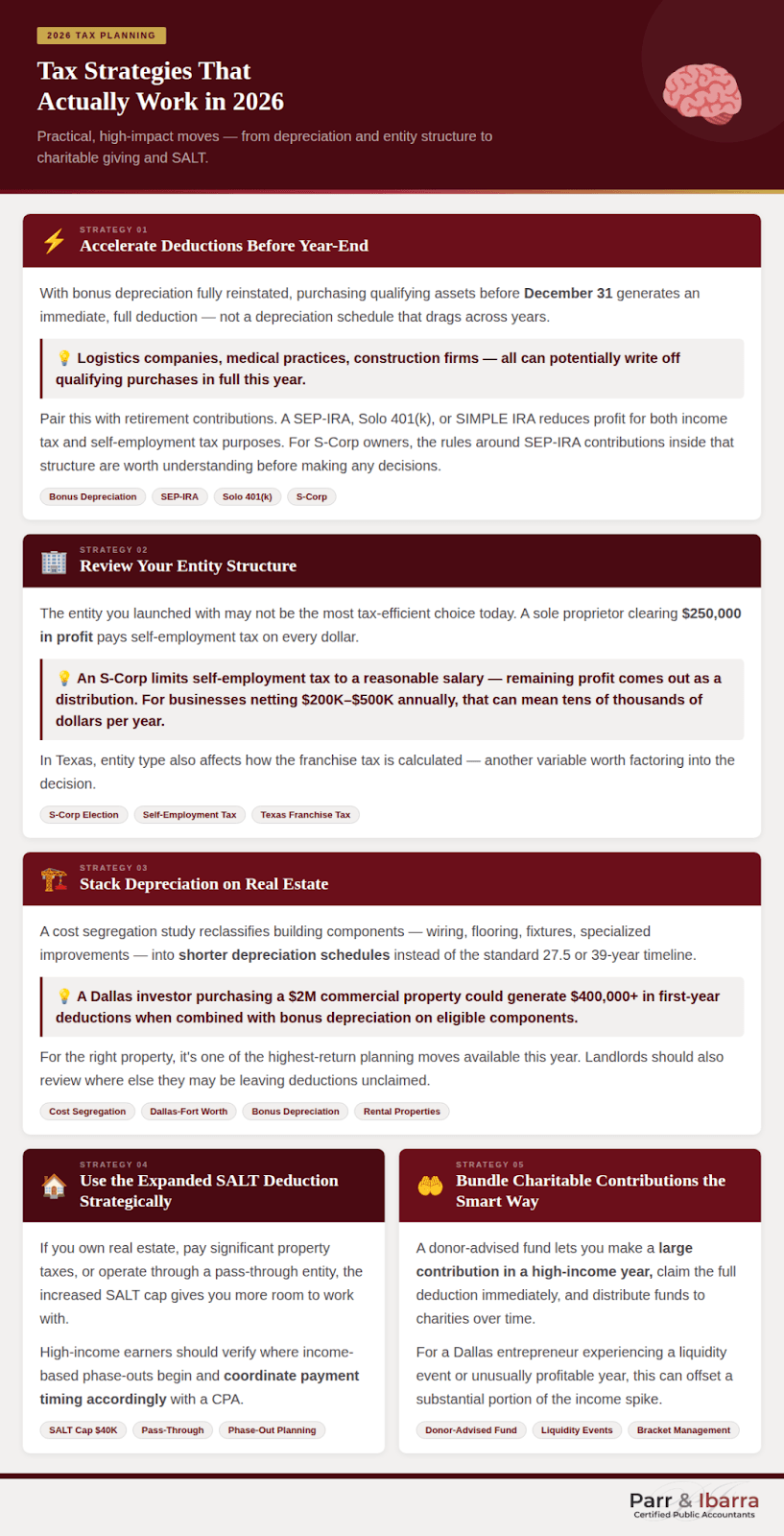

Tax Strategies That Actually Work in 2026

Accelerate Deductions Before Year-End

With bonus depreciation fully reinstated, purchasing qualifying assets before December 31 can generate an immediate, full deduction rather than a depreciation schedule that drags across years. A Dallas logistics company adding vehicles or warehouse equipment, a medical practice investing in new technology, a construction firm buying machinery. All of these businesses can potentially write off those purchases in full this year.

This strategy works even better when paired with retirement contributions. Contributing to a SEP-IRA, Solo 401(k), or SIMPLE IRA reduces profit for both income tax and self-employment tax purposes. A CPA-guided retirement plan ensures your contribution strategy is calibrated to your actual income, not just the annual maximum. For S-Corp owners specifically, the rules around SEP-IRA contributions inside that structure are worth understanding before you make any decisions.

Review Your Entity Structure

The entity you set up when you launched your business may not be the most tax-efficient choice today. A sole proprietor clearing $250,000 in profit is paying self-employment tax on every dollar. An S-Corp structure, properly implemented, limits self-employment tax to a reasonable salary, while the remaining profit comes out as a distribution. For businesses netting $200,000 to $500,000 annually, that distinction can mean tens of thousands of dollars per year.

A full comparison of business entity structures and their tax implications is worth going through before you assume your current setup is still optimal. In Texas, the entity type also affects how the franchise tax is calculated, which adds another variable to the decision.

Stack Depreciation on Real Estate

Texas real estate investors, particularly those active in the Dallas-Fort Worth market, have access to depreciation strategies that most owners don’t fully use. A cost segregation study reclassifies components of a building, things like wiring, flooring, fixtures, and specialized improvements, into shorter depreciation schedules instead of the standard 27.5 or 39-year timeline. Understanding how cost segregation works before commissioning a study helps you know whether it pencils out for your specific property.

Combined with bonus depreciation on eligible components, a Dallas investor purchasing a $2 million commercial property could generate $400,000 or more in first-year deductions. The real-world financial impact of these studies is well-documented, and for the right property, it’s one of the highest-return planning moves available this year. Landlords and rental property owners not yet familiar with this approach should also review the tax guide for landlords and real estate investors to understand where else they may be leaving deductions unclaimed.

Use the Expanded SALT Deduction Strategically

If you own real estate, pay significant local property taxes, or operate through a pass-through entity, the increased SALT cap gives you more room to work with. High-income earners should verify where the income-based phase-outs begin and coordinate the timing of payments accordingly with a CPA. This is also an area where strategies built for high-income professionals often surface planning moves that aren’t obvious without looking at the full picture.

Bundle Charitable Contributions the Smart Way

Most people make charitable contributions the same way every year. A check here, a donation there. It works, but it isn’t optimal. The 2026 updates to charitable deduction rules create real opportunities to be more strategic. A donor-advised fund lets you make a large contribution in a high-income year, claim the full deduction immediately, and distribute funds to your chosen charities over time. For a Dallas entrepreneur experiencing a liquidity event or an unusually profitable year, using RSUs and donor-advised funds together can offset a substantial portion of the income spike that would otherwise push you into a higher bracket.

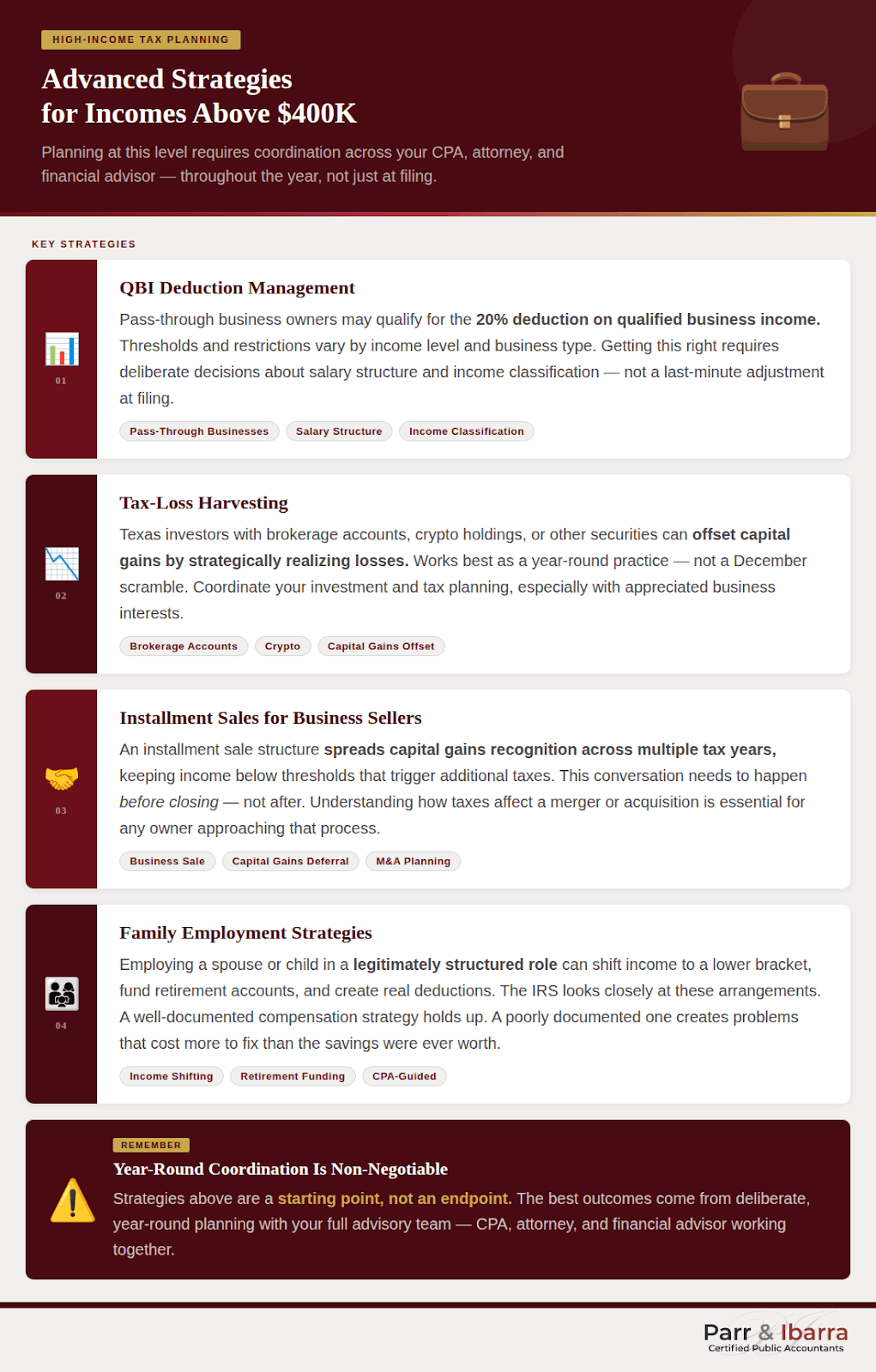

Advanced Strategies for Incomes Above $400K

Once your gross income clears $400,000, or your business generates significant passive income, the strategies above are a starting point rather than an endpoint. Planning at this level requires coordination across your CPA, attorney, and financial advisor throughout the year, not just at filing.

QBI Deduction Management. Pass-through business owners may still qualify for the 20% deduction on qualified business income. The thresholds and restrictions vary by income level and business type. Getting this right requires deliberate decisions about salary structure and income classification, not a last-minute adjustment when the return is being prepared.

Tax-Loss Harvesting. Texas investors with brokerage accounts, crypto holdings, or other securities can offset capital gains by strategically realizing losses. Strategic tax-loss harvesting works best as a year-round practice, not a December scramble. With capital gains rates potentially applying to appreciated business interests as well, coordinating your investment and tax planning is worth the effort.

Installment Sales for Business Sellers. If you’re considering selling your business, an installment sale structure can spread capital gains recognition across multiple tax years and keep income below thresholds that trigger additional taxes. This is a conversation that needs to happen before closing, not after. Understanding how taxes affect a merger or acquisition is essential reading for any owner actively in or approaching that process.

Family Employment Strategies. Employing a spouse or child in a legitimately structured role within your Texas business can shift income to a lower bracket, fund retirement accounts, and create real deductions. The IRS looks closely at these arrangements. A well-documented compensation strategy built with CPA guidance holds up under scrutiny. A poorly documented one creates problems that cost more to resolve than the savings were ever worth.

The Mistakes That Cost Texas Business Owners Real Money

Missing quarterly estimated tax deadlines: Business owners who don’t pay estimated taxes throughout the year face underpayment penalties in addition to the final bill. The IRS charges interest on late or insufficient payments, and that cost compounds. Knowing exactly how and when to make IRS tax payments keeps you ahead of those penalties rather than paying them after the fact.

Misclassifying employees as contractors: Calling someone a 1099 contractor doesn’t make it so. The IRS and Texas Workforce Commission both take worker classification seriously, and the tax implications of employees versus independent contractors are significant enough that any business relying heavily on contract labor should have those arrangements reviewed by a professional. Back payroll taxes, penalties, and audit exposure are all on the table when this goes wrong.

Failing to track vehicle and home office expenses: If you use your vehicle for business and work from home, those expenses are deductible, but only if you’ve documented them properly. The IRS expects a contemporaneous mileage log and documented business use for any home office deduction. Reconstructing this at tax time rarely works out well. Understanding IRS mileage rate rules and keeping a simple log throughout the year protects deductions you’re legitimately entitled to. The same applies to receipts for self-employed expenses. The IRS requirements for substantiating those deductions are specific, and “I have an estimate” doesn’t hold up under review.

Waiting until April to plan: Tax planning that happens in March for the prior year is compliance, not strategy. Real savings come from decisions made during the year: when to buy equipment, how to time income, which deductions to accelerate. By April 15, most of those windows are permanently closed.

Overlooking the Texas franchise tax: Texas doesn’t have a state income tax, but the franchise tax applies to most businesses above $2.47 million in revenue, and many below that threshold still have a filing obligation. Assuming your accountant is handling it isn’t enough. Confirm it explicitly, every year.

How This Plays Out for Real Texas Business Owners (illustrative)

The Dallas restaurant group owner runs two locations with $1.8 million in combined revenue needed to address both federal income tax and Texas franchise tax exposure. A cost segregation study on the leasehold improvements in the newer location, combined with bonus depreciation and a restructure from LLC to S-Corp, reduced his combined tax bill by over $60,000 in a single year. None of those moves were aggressive. They were just planned.

The Fort Worth real estate investor with seven residential rentals had been using standard depreciation schedules across the board. A cost segregation analysis and a review of his rental activity classification revealed that he qualified for real estate professional status, unlocking deductions that had been suspended for years. Understanding the difference between real estate dealer and investor classification is one of those distinctions that can fundamentally change your tax picture, and it’s one that gets missed constantly. With 100% bonus depreciation now available on reclassified components, the full benefit of a cost segregation study for real estate investors hit at exactly the right time.

The Dallas tech founder who had taken on a co-founder and outside investors needed help managing phantom income from equity distributions, planning around exit scenarios, and structuring compensation to minimize self-employment taxes while maintaining retirement contributions. Tax strategies built specifically for founders cover a lot of this ground, but the specifics always depend on the stage of the business and the personal tax picture sitting alongside it.

When to Hire a CPA (The Honest Answer)

Before you think you need one.

The clearest signals: you’re starting or buying a business, your income crossed $150,000, you acquired real estate, you received something from the IRS, you’re preparing for a sale, or you inherited assets. Each of those events carries specific tax implications that, handled without guidance, can cost multiples of what a CPA engagement would have.

For Dallas entrepreneurs and Texas business owners, the more useful question is often not “do I need a CPA?” but “am I actually getting what I should be from the one I have?” Tax preparation and tax planning are not the same thing. If your CPA only calls you in March, you’re getting the former. With IRS audit risks shifting in ways that affect businesses at every revenue level, the value of year-round professional support has gone up, not down. If you’ve never been through one, understanding how an IRS audit actually works is worth your time even if you never face one.

A CPA relationship built around proactive communication, quarterly check-ins, and year-round strategy is what separates businesses that manage their tax burden from those that are managed by it.

About Parr & Ibarra CPA

Parr & Ibarra CPA works with business owners, investors, and high-income professionals across Dallas, Fort Worth, and Texas. The firm was built for clients who need more than a return prepared once a year. Every engagement includes forward-looking planning, entity structure guidance, bookkeeping and financial reporting support, and CFO-level advisory for businesses that need strategic financial guidance without the overhead of a full-time hire.

The team stays current on every meaningful IRS update, including the full scope of the 2026 changes, so clients don’t have to become tax law experts themselves. That’s the job of a trusted CPA partner, and it’s a job worth taking seriously.

If you’re a Dallas or Texas business owner who hasn’t reviewed your tax strategy recently, schedule a consultation. There’s a good chance there’s money on the table.

Frequently Asked Questions

What are the biggest tax law changes in 2026?

The reinstatement of 100% bonus depreciation, the SALT deduction cap rising to $40,000, an expanded standard deduction ($32,200 for married filers), a higher estate tax exemption near $15 million, and a new $6,000 deduction for senior taxpayers. Together, these create meaningful planning opportunities for business owners who act before year-end rather than after.

How can I legally reduce my taxes in 2026?

Maximize retirement contributions, use bonus depreciation on qualifying asset purchases, review your entity structure for S-Corp efficiency, leverage the expanded SALT deduction, and consider donor-advised funds if you’re having a high-income year. Work with a CPA throughout the year. That last part is where most of the value actually lives.

Do Texas businesses benefit from the 2026 updates?

Yes, in several specific ways. Bonus depreciation benefits any Texas business investing in equipment this year. The raised SALT cap helps property-heavy businesses recover more of what they pay in local taxes. And because Texas has no state income tax, every dollar saved at the federal level goes directly to your bottom line. The franchise tax still applies and requires its own planning, but the overall picture for Texas businesses is favorable.

Is bonus depreciation really back at 100% in 2026?

Yes. Congress reinstated full first-year bonus depreciation after it had phased down to 60% in 2024. New and used equipment, vehicles, software, and certain qualified improvement properties all qualify. The building structure itself doesn’t, which is exactly why cost segregation studies are so valuable for real estate investors. They identify the components that do qualify and accelerate those deductions immediately.

What is the Texas franchise tax and who owes it?

It’s a state-level tax based on a business’s taxable margin, generally derived from gross revenue with limited deductions. Most businesses with annual Texas revenue above $2.47 million owe it, though rates and calculation methods vary. Unlike the federal income tax, it applies regardless of profitability, which makes it a consistent planning consideration for Texas companies of every type.

When should I hire a CPA instead of using tax software?

Once you own a business, hold rental properties, have significant investment income, earn above $150,000, or receive anything from the IRS, the complexity and financial stakes justify professional involvement. Tax software handles simple returns adequately. For business owners, the value of a CPA isn’t the return itself. It’s the planning that happens all year long before the return is ever prepared.

How does the IRS’s push toward digital compliance affect my business?

The IRS now receives data from more third-party sources than ever. Payment platforms, gig economy apps, and financial institutions all report at lower thresholds than before. Discrepancies between what those sources report and what shows up on your return create audit risk. Accurate bookkeeping and properly reconciled accounts are the most straightforward protection. A CPA-reviewed return gives you confidence that your filing matches what the IRS already knows about you.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.