We’ve been doing this long enough to know that most people don’t wake up excited about bookkeeping. It’s not supposed to be exciting. But here’s what we’ve learned working as a CPA in Keller Texas for years: the difference between people who have control over their finances and people who don’t usually comes down to their books.

Not their income level. Not their business model. Their bookkeeping.

We’re Parr & Ibarra, and we work with everyone from real estate investors managing multiple properties to restaurant owners tracking tip compliance to freelancers trying to figure out quarterly taxes for the first time. Some of our clients are individuals with complicated investment portfolios. Others run businesses with fifty employees. What they all have in common is they need their financial records to actually work for them.

So let’s talk about what professional bookkeeping actually means, why it matters more than you probably think, and when you should stop trying to do it yourself.

Bookkeeping Isn’t What Most People Think It Is

Here’s what we hear constantly: “I thought I just needed to keep my receipts and hand them to my accountant at tax time.”

That’s not bookkeeping. That’s a shoebox full of paper and a lot of hope.

Real bookkeeping means recording every financial transaction as it happens — every dollar that comes in, every dollar that goes out, every transfer between accounts, every credit card charge. Everything. And not just recording it, but categorizing it correctly so you can actually understand what the numbers mean.

Think of it like this. Bookkeeping is the daily work of tracking money. Accounting is looking at all that tracked money and figuring out what it tells you. Tax preparation is using both to legally minimize what you owe the IRS. They all depend on each other. You can’t have good tax planning if your books are a mess. You can’t make smart financial decisions if you don’t know where your money actually goes.

Working as a CPA in Texas, we see this constantly. People come to us with years of bank statements, unsorted receipts, and maybe a QuickBooks file they haven’t touched in eight months. They’re frustrated because they can’t get a loan, or they’re getting surprise tax bills, or they just have no idea if they’re actually profitable. And almost always, the problem started with bookkeeping.

Why Your Books Matter More Than You Realize

Nobody gets into business or builds wealth because they love bookkeeping. But here’s what good books actually give you.

You know what’s really happening with your money: Not what you think is happening. Not what you hope is happening. What’s actually happening. When someone asks “Can we afford this?” you have a real answer instead of a guess.

Your taxes get done faster and cheaper: We can prepare a tax return from clean books in a fraction of the time it takes when we’re sorting through chaos. That difference shows up in your bill. More importantly, clean books throughout the year mean you’re not missing deductions because we couldn’t find the documentation or figure out what a transaction was for.

You stay out of trouble: The IRS doesn’t care if you’re overwhelmed or busy. Miss critical filing deadlines, underreport income, or claim expenses you can’t prove? They’ll penalize you. Good bookkeeping keeps you compliant without thinking about it.

You can actually get financing when you need it: Banks want financial statements. Real ones, prepared from actual books, not something you threw together in Excel the night before your meeting. If you’re trying to buy property, expand your business, or get a business line of credit, your books matter.

You make better decisions: Should you hire someone? Can you afford that equipment? Is it time to raise prices? These aren’t guessing games when you have accurate financial data. We’ve watched clients avoid expensive mistakes and capitalize on opportunities they would have missed, all because they knew their numbers.

The Chart of Accounts (And Why It Actually Matters)

Your chart of accounts is basically your financial filing system. Every transaction gets put into a category, and those categories are your chart of accounts.

Now, most bookkeeping software comes with a default chart of accounts. QuickBooks has one. Xero has one. They’re generic templates designed to work for anybody, which means they don’t work particularly well for anybody specific.

A restaurant needs to track food costs differently than a consulting firm tracks their expenses. A real estate investor managing rental properties needs different categories than a freelance designer. What works for a retail store doesn’t work for a medical practice. And Texas has specific requirements that differ from what businesses in other states need.

Your business entity structure also shapes how your chart of accounts should be built. An S-corp needs different equity accounts than a sole proprietor. An LLC taxed as a partnership tracks owner draws differently than a C-corp tracks shareholder distributions. Getting this right from the start prevents major headaches at tax time, and it means the structure you chose when you formed your business actually shows up correctly in your financial records.

When we set up books for a new client at our Keller office, we’re thinking about their tax situation from day one. We’re building categories that make year-end tax prep easier. We’re making sure they can track what actually matters to their business or their financial situation. A good chart of accounts is customized. Period.

The problem with using the default setup is you end up with either too many categories (so everything’s spread out and you can’t see patterns) or too few (so everything gets dumped into “miscellaneous” and you have no idea what you’re actually spending money on). Neither one helps you.

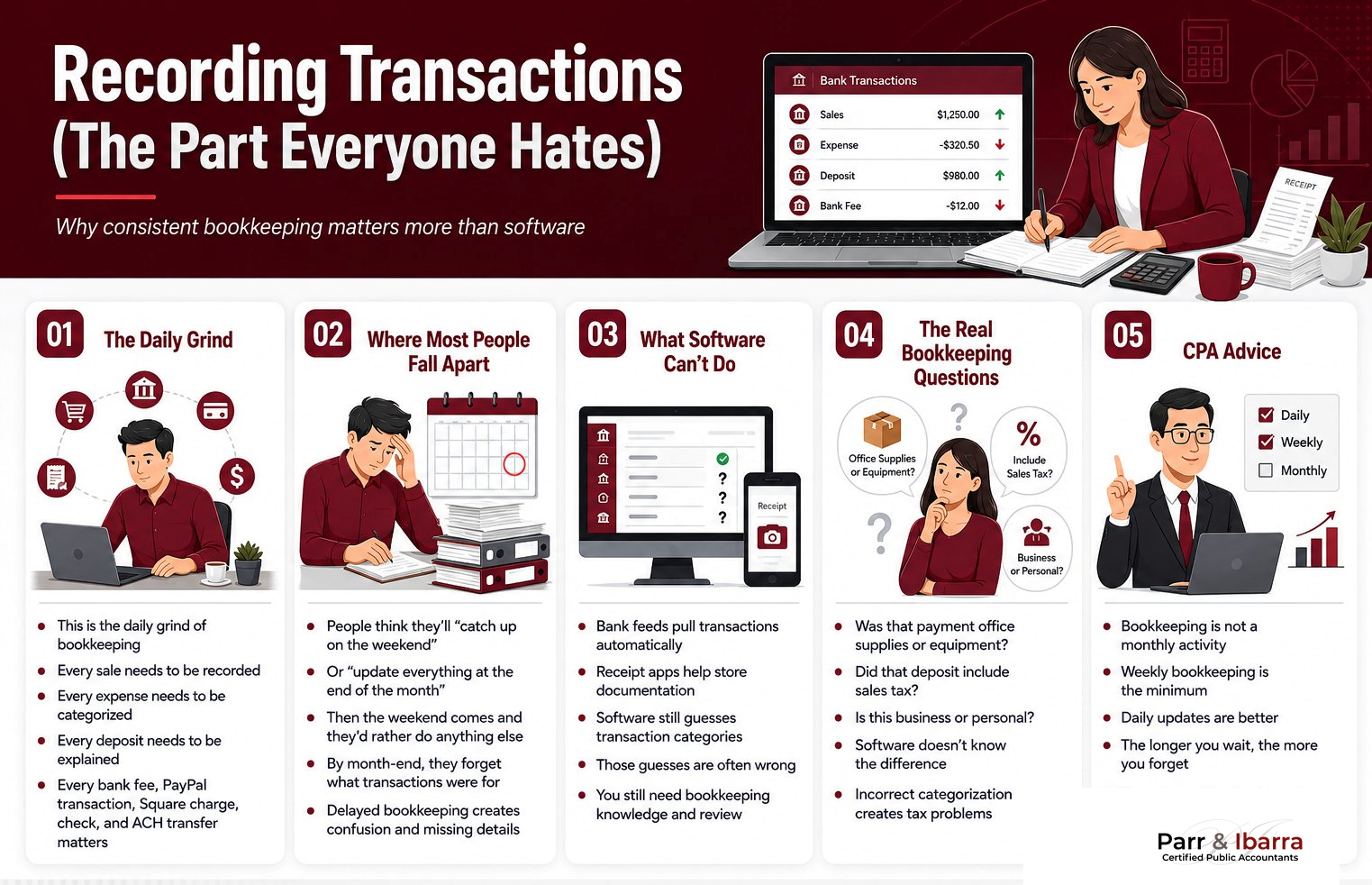

Recording Transactions (The Part Everyone Hates)

This is the daily grind of bookkeeping, and it’s exactly as tedious as it sounds.

Every sale needs to be recorded. Every expense needs to be categorized. Every deposit needs to be explained. Every bank fee, every PayPal transaction, every Square charge, every check, every ACH transfer. All of it.

Don’t overlook mileage, either. If you drive for business, consistently tracking your miles against IRS standard mileage rates throughout the year is significantly easier than reconstructing trips at tax time. Same goes for any self-employed deduction, understanding the IRS receipt requirements for business deductions before you make the expense is what keeps you protected if you’re ever questioned.

Here’s where most people fall apart. They think they’ll “catch up on the weekend” or “update everything at the end of the month.” Then the weekend comes and they’d rather do literally anything else. By the time month-end rolls around, they can’t remember what half the transactions were for.

The software helps. Bank feeds pull transactions automatically. Receipt apps let you snap photos of documentation. But here’s what software can’t do: it can’t tell you how to categorize things. It guesses, and those guesses are wrong constantly.

Was that $500 payment office supplies or equipment? Did that deposit include sales tax? Is this a business expense or personal? Software doesn’t know. You have to know, or you have to have someone who knows.

As a CPA in Keller Texas, we tell clients the same thing: bookkeeping isn’t a monthly activity. It’s weekly at minimum. Daily is better. Because the longer you wait, the more you forget, and the more you’re guessing when you finally get around to it. And guessing in bookkeeping leads to problems at tax time.

Bank Reconciliation Is Non-Negotiable

Reconciling your accounts means making sure what’s in your bookkeeping system matches what’s actually in your bank account. You do this monthly. Every month. No exceptions.

Why? Because if they don’t match, something’s wrong. You’re missing transactions. You’ve got duplicates. There’s a timing issue you need to track down. Whatever it is, you need to find it and fix it.

We’ve taken over bookkeeping for clients who hadn’t reconciled in months. Sometimes years. They had no idea if their financial statements were even remotely accurate. Finding all the discrepancies takes hours of detailed work that wouldn’t be necessary if they’d just reconciled monthly from the beginning.

Every account gets reconciled. Your bank account. Your credit cards. PayPal. Stripe. Investment accounts if they’re part of your books. All of it. Because unreconciled accounts hide problems until they’re expensive to fix.

This is boring work. Nobody enjoys it. But it’s the difference between books you can trust and books that might be completely wrong.

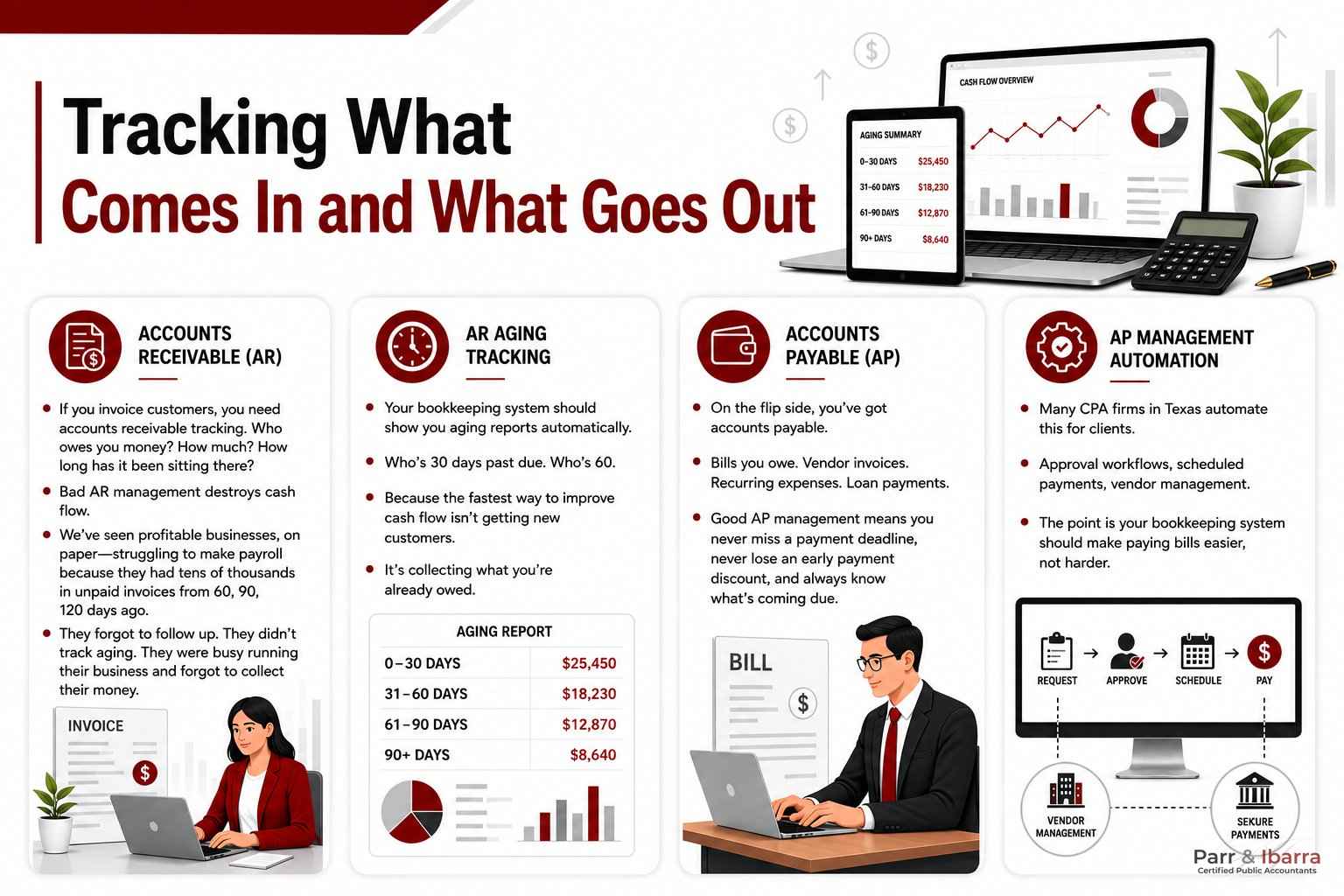

Tracking What Comes In and What Goes Out

If you invoice customers, you need accounts receivable tracking. Who owes you money? How much? How long has it been sitting there?

Bad AR management destroys cash flow. We’ve seen profitable businesses, on paper—struggling to make payroll because they had tens of thousands in unpaid invoices from 60, 90, 120 days ago. They forgot to follow up. They didn’t track aging. They were busy running their business and forgot to collect their money.

Your bookkeeping system should show you aging reports automatically. Who’s 30 days past due. Who’s 60. Because the fastest way to improve cash flow isn’t getting new customers. It’s collecting what you’re already owed.

On the flip side, you’ve got accounts payable. Bills you owe. Vendor invoices. Recurring expenses. Loan payments. Good AP management means you never miss a payment deadline, never lose an early payment discount, and always know what’s coming due.

Many CPA firms in Texas automate this for clients. Approval workflows, scheduled payments, vendor management. The point is your bookkeeping system should make paying bills easier, not harder.

Payroll Bookkeeping: What Business Owners Need to Know

If you have employees or work with contractors, payroll is one of the most compliance-heavy components of your bookkeeping, and one of the most commonly mishandled. Get it wrong, and the consequences aren’t just accounting errors. They’re IRS penalties and back taxes.

It starts with worker classification. The decision between hiring employees versus 1099 contractors has dramatically different tax implications for your business, and the IRS scrutinizes misclassification closely. Once that determination is made, you need a clear picture of the different types of payroll taxes your business is responsible for, federal income tax withholding, FICA (Social Security and Medicare), FUTA, and in Texas, SUTA.

From there, one of the most common questions we get from business owners new to payroll is how to calculate the correct withholding amounts for each employee. Getting this wrong in either direction creates problems. Under-withhold and your employees face unexpected tax bills at year-end. Over-withhold and you’ve introduced a compliance headache that’s hard to unwind.

Things get more nuanced when you have mixed working relationships. If the same individual performs different types of work for your business at different points — sometimes as an employee, sometimes as a contractor — knowing when to issue both a W-2 and a 1099 to the same person becomes a real question. The answer matters, and getting it wrong can trigger unwanted IRS attention.

The bottom line: payroll bookkeeping is an area where errors compound fast and the regulatory exposure is real. For most business owners, professional oversight isn’t optional , it’s worth it.

Cash vs. Accrual (And Why You Need to Pick the Right One)

There are two ways to do bookkeeping, and picking the wrong one causes problems.

Cash basis is simpler. You record money when it hits your account. You record expenses when money leaves. It’s intuitive, and most smaller operations can use it. The IRS allows it if you don’t carry inventory and your receipts are under $30 million.

The accrual basis is more complex. You record income when you earn it, regardless of when payment arrives. You record expenses when you incur them, regardless of when you pay. It’s more accurate for understanding your real financial position, especially if you have significant timing differences between when you bill and when you get paid.

Which one should you use? Depends on your situation. The IRS requires accrual if you have inventory or you’re big enough. But even if you’re allowed to use cash basis, sometimes accrual gives you better information for managing your finances.

Working as a CPA in Texas, we help people think through the tax implications and practical considerations. There’s not one right answer for everyone. It depends on what you’re trying to accomplish and what your situation looks like.

Software Matters (But It’s Not Magic)

You need bookkeeping software. Spreadsheets don’t cut it once you’re past extremely simple finances. The question is which one.

QuickBooks Online is still the market leader. We use it constantly with clients because it’s what most people in Texas use. It handles invoicing, expense tracking, bank feeds, payroll integration, and financial reports. It’s powerful enough to grow with you.

The downside? It can get pricey when you start adding features. And because it’s so powerful, you can mess things up if you don’t know what you’re doing. We’re QuickBooks ProAdvisors, which means we can set it up correctly from the start and fix things when they break.

Xero is a solid alternative. There are legitimate reasons to choose Xero over traditional accounting software — its clean interface, strong bank feed integration, and multi-currency handling stand out for businesses with more complex needs. It works especially well for detailed project tracking. The catch is fewer accountants know it well, so finding qualified help can be harder.

FreshBooks works well for service businesses that invoice a lot. Wave is free and surprisingly capable for basic bookkeeping. But both are designed for simpler situations, and as you grow or add complexity, you’ll probably outgrow them. Businesses at that stage should look into how to evaluate ERP software for greater accounting efficiency — when standard small-business platforms stop keeping pace with your operations, an ERP can consolidate everything.

Here’s what matters more than which software you pick: you need someone who knows how to use it properly. Software doesn’t replace judgment. It doesn’t know how to categorize things for Texas franchise tax. It doesn’t catch errors it’s not programmed to find. Software is a tool. You still need expertise.

Texas-Specific Stuff You Need to Track

Operating in Texas means dealing with state requirements that your bookkeeping needs to handle.

Sales tax is the big one for businesses. Texas has a 6.25% state rate, plus local rates that vary. Some parts of DFW have combined rates over 8%. Your books need to track sales tax separately from revenue. They need to handle different rates if you’re in multiple locations. And they need to make filing with the Texas Comptroller straightforward.

We’ve seen businesses get into real trouble by using sales tax money for operating expenses. That money doesn’t belong to you. It belongs to the state. Spend it and you’re creating a liability you can’t pay.

Then there’s Texas franchise tax. We don’t have corporate income tax, but we do have the margin tax. It applies to most businesses operating here. Your bookkeeping affects the calculation because the state looks at your revenue, cost of goods sold, and compensation.

Good bookkeeping throughout the year makes franchise tax reporting easy. Poor bookkeeping means scrambling at the deadline trying to reconstruct numbers. Many businesses qualify for the small business exception if they’re under $2.47 million in annual revenue. But you still need accurate books to prove it.

If you have employees, Texas employers are also responsible for payroll-related obligations at both the federal and state level. Understanding your federal unemployment tax (FUTA) obligations and the Texas state unemployment tax (SUTA) requirements are both part of keeping your books compliant — and your liability in check — as an employer in this state.

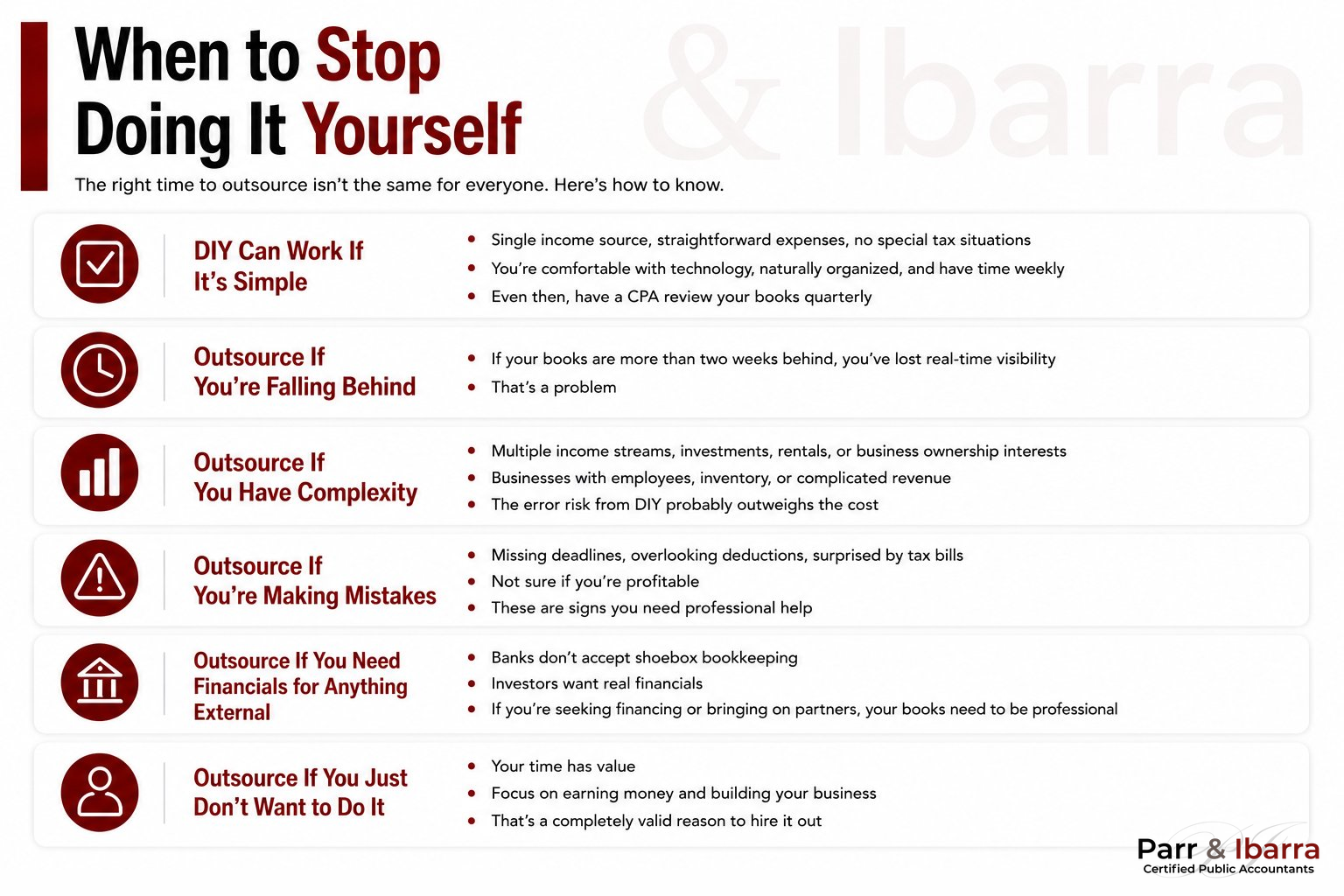

When to Stop Doing It Yourself

This is the question we get asked most often. “Should I handle this myself or hire someone?”

Honest answer: it depends on your situation.

DIY can work if your finances are genuinely simple. Single income source, straightforward expenses, no special tax situations. You’re comfortable with technology. You’re naturally organized. You have time to stay on top of it, we’re talking weekly, not letting months pile up. Even then, we’d recommend having a CPA review your books quarterly to catch mistakes before they compound.

But you should probably outsource if you’re falling behind. If your books are more than two weeks behind right now, you’ve already lost real-time visibility. That’s a problem.

Outsource if you have complexity. Multiple income streams, investment portfolios, rental properties, business ownership interests. Operating a business with employees, inventory, or complicated revenue. Any of that and the error risk from DIY probably outweighs the cost of doing it right. If you’re scaling quickly, it may also be worth exploring why CFO-level services become essential for growing businesses, having someone who not only maintains your books but actively uses them to drive financial strategy can change how your business operates.

Outsource if you’re making mistakes. Missing deadlines, overlooking deductions, surprised by your tax bill, not sure if you’re profitable. These are signs you need professional help.

Outsource if you need financial statements for anything external. Banks don’t accept shoebox bookkeeping. Investors want real financials. If you’re trying to get financing or bring on partners, your books need to be professional.

And honestly? Outsource if you just don’t want to do it. Your time has value. If you’d rather focus on actually earning money or building your business than managing books, that’s a completely valid reason to hire it out. Managing your finances through virtual accounting gives you the expertise of a full back-office team without the overhead of hiring in-house staff, and it scales as your business grows.

At Parr & Ibarra, we handle full bookkeeping for clients who need everything from daily transaction recording to monthly financial reporting. We become their back-office accounting department without the overhead of hiring staff. We handle the details so they can focus on what they’re actually good at.

Financial Statements That Actually Mean Something

Good bookkeeping produces financial statements you can use. Not compliance paperwork. Actual tools for making decisions.

Your profit and loss statement shows revenue minus expenses for a specific period. Monthly, quarterly, annually. This is where most people start. Am I profitable? Where’s the money going? What are the trends?

A good P&L breaks expenses into categories that make sense for your situation. Not generic categories from the software defaults. Categories that help you actually understand your finances and make decisions.

Your balance sheet shows assets, liabilities, and equity at a specific point in time. It’s your financial snapshot, what you own, what you owe, what’s left over. Lenders look at balance sheets to evaluate creditworthiness. Investors use them to assess financial health. You should use them to understand your liquidity and debt position.

The cash flow statement is underrated but critical. It shows where cash came from and where it went. You can be profitable on paper and still run out of cash. Happens all the time. Strong sales with slow collections, inventory building up, equipment purchases, all can drain cash while you’re showing profit. Understanding cash flow is often what separates businesses that survive rough periods from businesses that close. It’s that important.

When your business reaches a certain size, or when lenders, investors, or regulators start requesting formally verified financials, you’ll need to understand what those look like compared to your standard internal statements. The difference between audit and assurance is a good place to start, and from there, choosing between an audit, a review, and a compilation depends on who’s asking for the statements, what they need them for, and how much external validation is required. If you’re approaching a formal audit for the first time, our guide to preparing for a financial statement audit walks through what to expect and how to get ready.

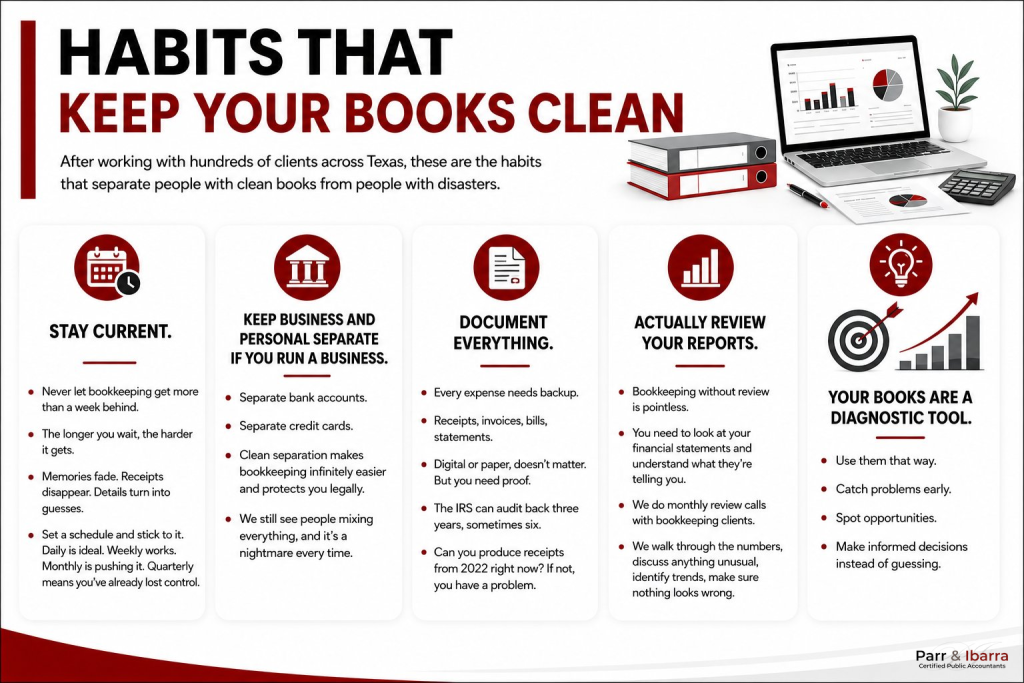

Habits That Keep Your Books Clean

After working with hundreds of clients across Texas, these are the habits that separate people with clean books from people with disasters.

Stay current: Never let bookkeeping get more than a week behind. The longer you wait, the harder it gets. Memories fade. Receipts disappear. Details turn into guesses. Set a schedule and stick to it. Daily is ideal. Weekly works. Monthly is pushing it. Quarterly means you’ve already lost control.

Keep business and personal separate: If you run a business. Separate bank accounts. Separate credit cards. Clean separation makes bookkeeping infinitely easier, and it protects you legally. Commingling funds is one of the fastest ways to put your LLC liability protection at risk if your business is ever challenged in court. We still see people mixing everything, and it creates problems every time.

Document everything: Every expense needs backup. Receipts, invoices, bills, statements. Digital or paper, doesn’t matter. But you need proof. Most business owners don’t have a clear picture of what records they actually need to keep — and that gap tends to show up at the worst possible time. The IRS can audit back three years, sometimes six. Can you produce receipts from 2022 right now? If not, you have a problem.

Actually review your reports: Bookkeeping without review is pointless. You need to look at your financial statements and understand what they’re telling you. We do monthly review calls with bookkeeping clients. We walk through the numbers, discuss anything unusual, identify trends, and make sure nothing looks wrong.

Your books are a diagnostic tool. Use them that way. Catch problems early. Spot opportunities. Make informed decisions instead of guessing.

Common Questions We Actually Get Asked

How much does professional bookkeeping cost?

Depends on volume and complexity. Simple situations might be a few hundred monthly. Complex operations with heavy transaction volume could be several thousand. But compare that to tax penalties, missed deductions, and financial mistakes. Good bookkeeping usually pays for itself.

Can I switch accounting methods mid-year?

Technically yes, but it creates complications. Generally better to switch at year-end. That said, if your current bookkeeping is a complete disaster, sometimes immediate cleanup and switching is better than continuing down the wrong path. Talk to a CPA before making changes.

How long should I keep records?

The IRS recommends at least three years for tax returns and supporting documents. Seven years is safer for income documentation. Some records — business formation documents, property records, loan documents, should be kept permanently. Our breakdown of what specific records businesses need to retain covers the schedules in more detail. For payroll specifically, payroll record retention requirements follow their own timeline and are worth understanding on their own terms.

What if I need more time to file?

It happens. A business tax extension gives you more time to file your return, but it does not extend the time to pay. If you owe, payment is still due by the original deadline. Getting that wrong is a costly mistake.

What’s the difference between a bookkeeper and a CPA?

Bookkeepers record transactions and maintain records. CPAs are licensed accountants who can also provide tax planning, audit services, financial analysis, and strategic advice. If you’re weighing your options, it also helps to understand how a CPA differs from a tax strategist, the distinction matters when you’re deciding what level of expertise your situation actually calls for. At Parr & Ibarra, we offer both bookkeeping and higher-level CPA services, using bookkeeping data as the foundation for tax strategy and financial planning.

How do I catch up if I’m behind?

Block time, gather documents, work through each month systematically. Start with bank reconciliation to find missing transactions. Categorize everything properly. Don’t skip months trying to catch up faster. Or hire someone to do cleanup. We do bookkeeping reconstruction regularly. It’s tedious but necessary.

Why This Actually Matters

Professional bookkeeping isn’t about compliance forms or satisfying the IRS. It’s about having clarity and control over your financial life.

When your books are accurate and current, you know your real position. You make decisions based on facts instead of guesses. You catch problems while they’re still small. You maximize tax benefits because everything’s documented properly, which also means you’re positioned to take full advantage of strategies like depreciation, amortization, and expensing elections that most business owners miss simply because their books aren’t organized enough to support them. And you sleep better knowing your financial house is in order.

Working as a CPA in Keller Texas, we’ve built our practice around providing bookkeeping that goes beyond transaction recording. We deliver financial insight, support strategic planning, and ensure compliance with all the regulatory requirements. But mainly, we give people confidence in their numbers.

Whether you’re an individual with complicated investment portfolios, a business growing through multiple locations, or anywhere in between, professional bookkeeping makes a measurable difference.

We work with clients across Texas who need more than data entry. They need financial visibility. Tax optimization. Strategic guidance. That’s what working with an actual CPA firm gets you compared to just using software or hiring a basic bookkeeper.

Your financial records tell your story. The question is whether that story is accurate, complete, and useful for making the decisions that determine your success. That’s what professional bookkeeping is really about.

Get Professional Help That Actually Helps

At Parr & Ibarra, we handle bookkeeping for individuals with complex finances and businesses of all sizes across the Dallas-Fort Worth area. We’re not a bookkeeping mill processing transactions. We’re CPAs who use accurate books as the foundation for tax planning, financial strategy, and business growth.

Our approach is hands-on and forward-looking. We don’t just record transactions — we help you understand what the numbers mean and use that information to make better decisions. Whether it’s reducing taxes, improving cash flow, or planning for growth, we work alongside our clients as partners.

We specialize in industries like real estate, where bookkeeping complexity is higher and tax deduction strategies for real estate professionals require careful documentation throughout the year, not just at tax time. We also work extensively with healthcare practices, where CPA services for healthcare providers often means navigating industry-specific compliance requirements alongside the standard bookkeeping and tax work. And we work with everyone from freelancers figuring out quarterly taxes to established businesses managing multi-location expansion.

If you’re in Keller, Grapevine, Hurst, Addison, or anywhere in the DFW area and you need bookkeeping that actually works, let’s talk. We’ll review your current situation, identify what needs fixing, and build a system that gives you the clarity you need.