Introduction: Paying More in Taxes Than You Should?

Here is a number that most business owners never want to hear: the IRS estimates that Americans collectively overpay their taxes by tens of billions of dollars every year. Not because they’re dishonest. Because they’re uninformed. If you suspect you’re paying more in taxes than you should be, you are far from alone, and the gap between what you owe and what you actually pay is almost always a planning problem, not a math problem.

If you own a business in Dallas, invest in Texas real estate, or earn a high income in the Lone Star State, tax planning is not a once-a-year conversation with your accountant in April. It is a year-round financial discipline that can legally reduce what you owe, protect your assets, and compound your wealth over time.

The 2026 tax year brings meaningful changes. Expanded deductions, reinstated depreciation rules, updated brackets, and a transformed SALT landscape have shifted the calculus for both individuals and business entities. Knowing how to use these changes, rather than simply reacting to them, is the difference between a CPA who files your return and a tax strategist who builds your financial future.

At Parr & Ibarra CPA, we work with Dallas entrepreneurs, Texas business owners, and high-income professionals who refuse to leave money on the table. This guide explains exactly what changed in 2026, what strategies work, and how to position yourself before December 31 so tax season is never a surprise.

What Is Tax Planning?

Tax planning is the process of structuring your financial decisions throughout the year to minimize your tax liability within the bounds of U.S. law. It covers everything from choosing the right business entity to timing income and deductions, maximizing retirement contributions, and leveraging credits built into the tax code.

It is not tax evasion. It is not a gray area. It is exactly what Congress intends when it writes incentives, deductions, and credits into the Internal Revenue Code.

For a Dallas contractor who just signed a $2 million commercial deal, tax planning might mean accelerating depreciation on new equipment. For a Texas physician with passive rental income, it might mean a strategic Roth conversion. For a family-owned manufacturing company in Fort Worth, it might mean restructuring from a sole proprietorship into an S-Corp to reduce self-employment tax.

The strategy depends on your situation. The principle is universal: plan proactively, not reactively.

Why Tax Planning Matters More in 2026

The 2026 tax year is not business as usual. Several significant provisions have been updated or reinstated as part of the broader 2026 federal tax reform, and failing to account for them means either missing legitimate savings or walking into unexpected liabilities.

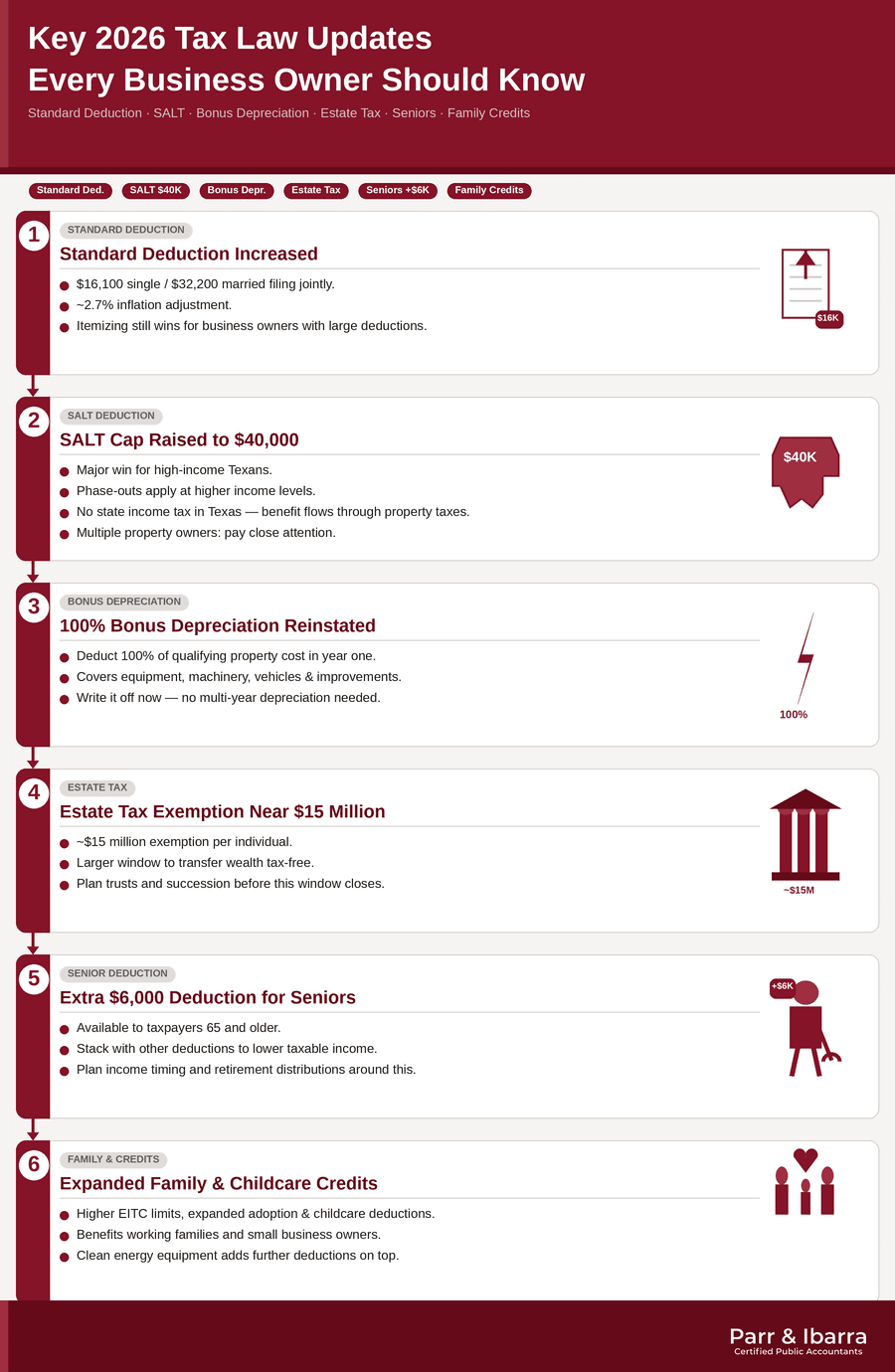

Key 2026 Tax Law Updates

Standard Deduction Increase: The standard deduction now sits at $16,100 for single filers and $32,200 for married couples filing jointly, reflecting a roughly 2.7% inflation adjustment. For many middle-income earners, this makes itemizing less compelling. But for business owners and investors with significant deductible expenses, itemizing still wins.

SALT Deduction Cap Raised to $40,000: This is one of the most impactful changes for high-income Texans. The State and Local Tax deduction has been raised to $40,000, though income-based phase-outs apply at higher income levels. Texas has no state income tax, so the SALT benefit here primarily flows through property taxes and any local taxes paid. Investors with multiple properties across Texas should pay close attention.

100% Bonus Depreciation Reinstated: This one is a major win for business owners. Full expense is back. In 2026, you can again deduct 100% of the cost of qualifying business property in the year it is placed in service. With 100% bonus depreciation back on the table, equipment, machinery, vehicles, and certain improvements can be written off immediately rather than depreciated over years. For a Dallas logistics company buying a fleet of vehicles, or a construction firm investing in heavy equipment, this is real, immediate tax relief.

Estate Tax Exemption Near $15 Million: Families with significant assets, real estate portfolios, or business interests have a larger window to plan wealth transfers without triggering estate tax. With the exemption at approximately $15 million, there is a great deal business owners need to know about estate planning before this window closes, including how proper structuring of trusts and business succession plans protects affluent Texas families.

Additional $6,000 Deduction for Seniors: Taxpayers who are 65 or older now qualify for an additional $6,000 deduction. For retired business owners or senior investors drawing down retirement accounts, this creates meaningful planning opportunities around income timing and distribution strategies.

Expanded Family and Childcare Credits: Higher EITC limits, expanded adoption credits, and improved childcare deductions benefit working families and small business owners who provide dependent care assistance programs to employees. Texas businesses should also review clean energy tax breaks still available in 2026, as qualifying investments in energy-efficient equipment and systems can layer additional deductions on top of other 2026 credits.

Complete Tax Planning Strategy Breakdown

1. Choose the Right Business Entity

The structure of your business is the foundation of your tax strategy. How your business entity structure affects what you owe in taxes is where every effective tax plan begins, and Texas business owners frequently leave significant money on the table by staying in the wrong entity type as their income grows.

A sole proprietor or single-member LLC earning $200,000 annually pays self-employment tax (15.3%) on every dollar of net income. Beyond the tax cost, it is worth understanding how poor financial practices can put your LLC liability shield at risk, because structural mistakes compound both legal exposure and tax liability over time. An S-Corporation earning the same amount pays that tax only on a reasonable salary component. The rest flows through as a distribution, free of self-employment tax. The tax benefits of structuring as an S-Corporation extend well beyond payroll savings, particularly for business owners with significant pass-through income. On $200,000 of net income, the difference can easily exceed $15,000 per year.

C-Corporations have a flat 21% federal rate. For businesses retaining earnings rather than distributing them, this can create significant tax advantages, particularly when paired with strategic fringe benefit plans.

For family-owned businesses evaluating more sophisticated ownership structures, using a family limited partnership in your overall financial strategy can offer layered tax efficiency alongside estate planning benefits that a simple LLC or S-Corp cannot match.

If you started your business as a sole proprietor or a basic LLC and your net income has grown past $80,000, a conversation about entity restructuring belongs on your agenda this year.

2. Maximize Retirement Contributions

Retirement accounts are one of the cleanest, most legal, and most underused tax reduction tools available. For 2026, contribution limits continue to climb.

A SEP-IRA allows self-employed individuals and small business owners to contribute up to 25% of net self-employment income, with a dollar-cap that has crossed $70,000 for high earners. What S-Corporations specifically need to know about SEP-IRA contributions matters because the structure of your entity directly affects how contributions are calculated, what limits apply, and which retirement vehicles remain available to you and your employees. A Solo 401(k) offers even more flexibility, including a Roth option and loan provisions.

For Dallas entrepreneurs running profitable businesses, stacking retirement contributions, health insurance deductions, and HSA contributions can reduce taxable income by $80,000 to $100,000 or more in a single year. That is not hypothetical. That is a strategy we implement with clients regularly. Working with a CPA to maximize retirement planning and tax savings is not just about hitting contribution deadlines. It is about coordinating the right account types with the right entity structure at the right moment in your income cycle.

3. Deploy Bonus Depreciation Strategically

With 100% bonus depreciation reinstated in 2026, the window to accelerate deductions is open. Qualifying property includes most tangible personal property with a recovery period of 20 years or less. Leveraging bonus depreciation alongside cost segregation in the post-reform tax environment requires understanding not just what qualifies, but when and how to time the placement of assets in service to capture the full deduction.

A Dallas-based restaurant group investing in kitchen equipment can write off the entire purchase in year one. A Texas physician buying medical devices for a private practice can do the same. A real estate investor installing HVAC systems, flooring, or lighting improvements may qualify through cost segregation, and understanding the cost segregation process from start to finish is the first step toward knowing whether a study is worth commissioning on your specific property.

The key is timing. Property must be placed in service during 2026 to qualify. If you are planning a capital investment, moving it into this tax year rather than waiting until January could produce a six-figure deduction.

4. Leverage the Texas Tax Advantage

Texas has no personal state income tax. That is a structural advantage that out-of-state business owners and high earners who relocate here frequently underestimate. For business owners and professionals weighing a move, understanding the key tax considerations when relocating to the DFW area surfaces planning opportunities that begin well before you file your first Texas return.

A California-based entrepreneur earning $500,000 annually pays up to 13.3% in state income tax. The same income earned in Texas, zero. For high-income professionals moving to Dallas, or California businesses establishing Texas operations, the annual savings can exceed $50,000 to $60,000.

The Texas Franchise Tax, however, is a separate matter. Texas imposes a margin tax on most business entities with revenues above a certain threshold. The calculation can be based on total revenue, compensation paid, or cost of goods sold, and choosing the wrong method can cost thousands. Understanding the Texas state unemployment tax and your broader Texas payroll tax obligations is an essential step for any business owner operating in the state. This is an area where having a CPA familiar with Texas tax law is not optional, it is essential.

5. Optimize Timing of Income and Deductions

One of the simplest and most effective planning strategies is controlling when income is recognized and when deductions are claimed.

If your income is expected to be unusually high this year, you may want to accelerate deductible expenses. Pay January business expenses in December. Make charitable contributions before year-end. Fund retirement accounts now rather than waiting until April. Staying on top of essential tax deadlines every Texas business owner needs to track is the practical foundation that makes year-end timing strategies actually executable.

Conversely, if you expect a lower-income year in 2027 due to a business transition or planned sabbatical, it may make sense to defer income into that year, pushing Roth conversions or real estate sales to a lower-bracket window. For investment portfolios, strategic tax-loss harvesting can offset realized gains and reduce your effective tax rate without altering your long-term investment position, making it one of the cleaner timing tools available.

This kind of timing strategy sounds simple. Executing it correctly, within IRS rules, across multiple income streams and entity types, is where a knowledgeable CPA earns their fee many times over. If you need more runway, knowing how to file a business tax extension properly preserves your planning options without triggering the penalties that catch many business owners off guard.

6. Qualified Business Income Deduction (QBI)

Pass-through businesses, including S-Corps, partnerships, and sole proprietors, may qualify for a 20% deduction on qualified business income. This is one of the most powerful deductions available to small and mid-sized Texas businesses, and it is consistently underused. Top tax strategies for high-income professionals identify QBI optimization as one of the highest-value moves available to pass-through business owners, precisely because the stakes are high and the planning window is narrow.

For a business owner earning $300,000 in pass-through income, that is a $60,000 deduction before a single expense is counted.

Income limits apply, and certain service businesses phase out of the deduction at higher income levels. But with proper planning, including structuring wages within your S-Corp, splitting business activities, or restructuring service delivery, many high-income owners can retain access to this deduction. For founders and early-stage business owners in particular, essential tax strategies for founders lay out exactly how entity structure, compensation design, and QBI planning work together from day one.

Advanced Strategies for High-Value Clients

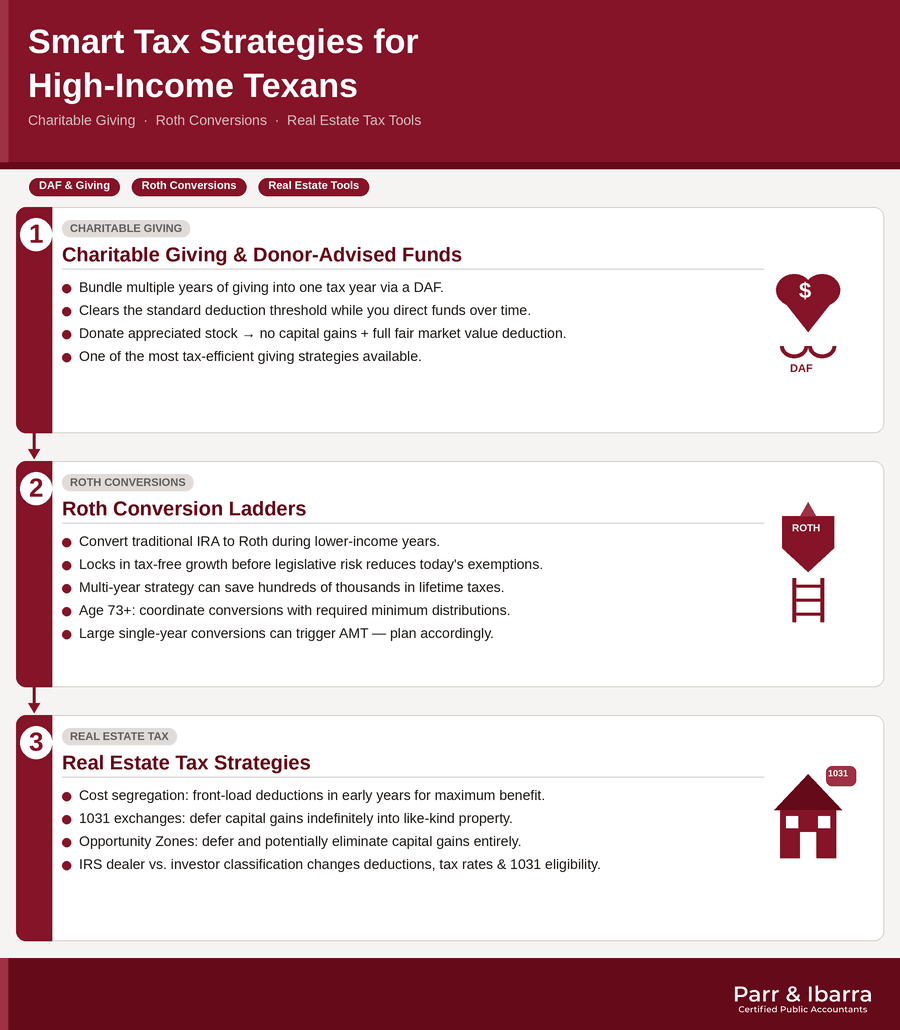

Charitable Giving and Donor-Advised Funds

For high-income Texans who give generously, maximizing charitable impact through RSUs and Donor-Advised Funds allows bundling multiple years of contributions into a single tax year, clearing the standard deduction threshold while still directing funds to chosen charities over time. Combined with the 2026 updates to charitable contribution rules and itemized deduction thresholds, this strategy can produce meaningful itemized deductions for clients who would otherwise default to the standard deduction.

Appreciated stock contributions to a DAF eliminate capital gains tax on the donated shares while providing a fair market value deduction. It is one of the most tax-efficient giving strategies available.

Roth Conversion Ladders

The estate tax exemption at approximately $15 million is generous today. But legislative risk exists. Locking in tax-free growth now through Roth conversion strategies, including backdoor Roth options for high earners blocked from direct contributions, especially in lower-income years, creates a permanent asset that avoids both income tax and, with proper estate planning, estate tax exposure.

For Texas investors sitting on large traditional IRA balances, a multi-year Roth conversion strategy executed during moderate-income years can save hundreds of thousands in lifetime taxes. For those approaching or past age 73, reducing the tax burden of required minimum distributions is a natural complement to the Roth ladder approach, since strategic distributions and conversions interact closely. High-conversion-year strategies can also brush up against the alternative minimum tax, and understanding how to use AMT credit carryforwards is worth reviewing before executing a large conversion in any single year.

Real Estate Tax Strategies

Texas remains one of the strongest real estate markets in the country, and Dallas continues to attract commercial and residential investment. With that comes a rich set of tax tools.

The real-world financial impact of cost segregation studies demonstrates how investors front-load deductions in early years when the tax benefit is highest. Seven proven strategies to reduce capital gains tax on real estate, including 1031 exchanges that allow investors to defer capital gains taxes indefinitely by rolling proceeds from one investment property into another, represent core planning tools every Texas property investor should understand. Opportunity Zone investments in targeted Texas communities can defer and potentially eliminate capital gains taxes entirely, and how the new legislation reshaped Qualified Opportunity Zones clarifies exactly what changed and who can benefit in 2026.

One nuance that directly affects strategy selection is how the IRS classifies real estate dealers versus investors, because that classification changes which deductions apply, how gains are taxed, and whether 1031 exchange treatment is even available to you.

These are sophisticated strategies. They require careful execution and coordination between your CPA, attorney, and financial advisor. But the savings justify the complexity.

Looking to optimize your property investments? Explore our in-depth guide on Real Estate Tax Strategies to uncover powerful ways to reduce liabilities and maximize returns.

Common Tax Planning Mistakes to Avoid

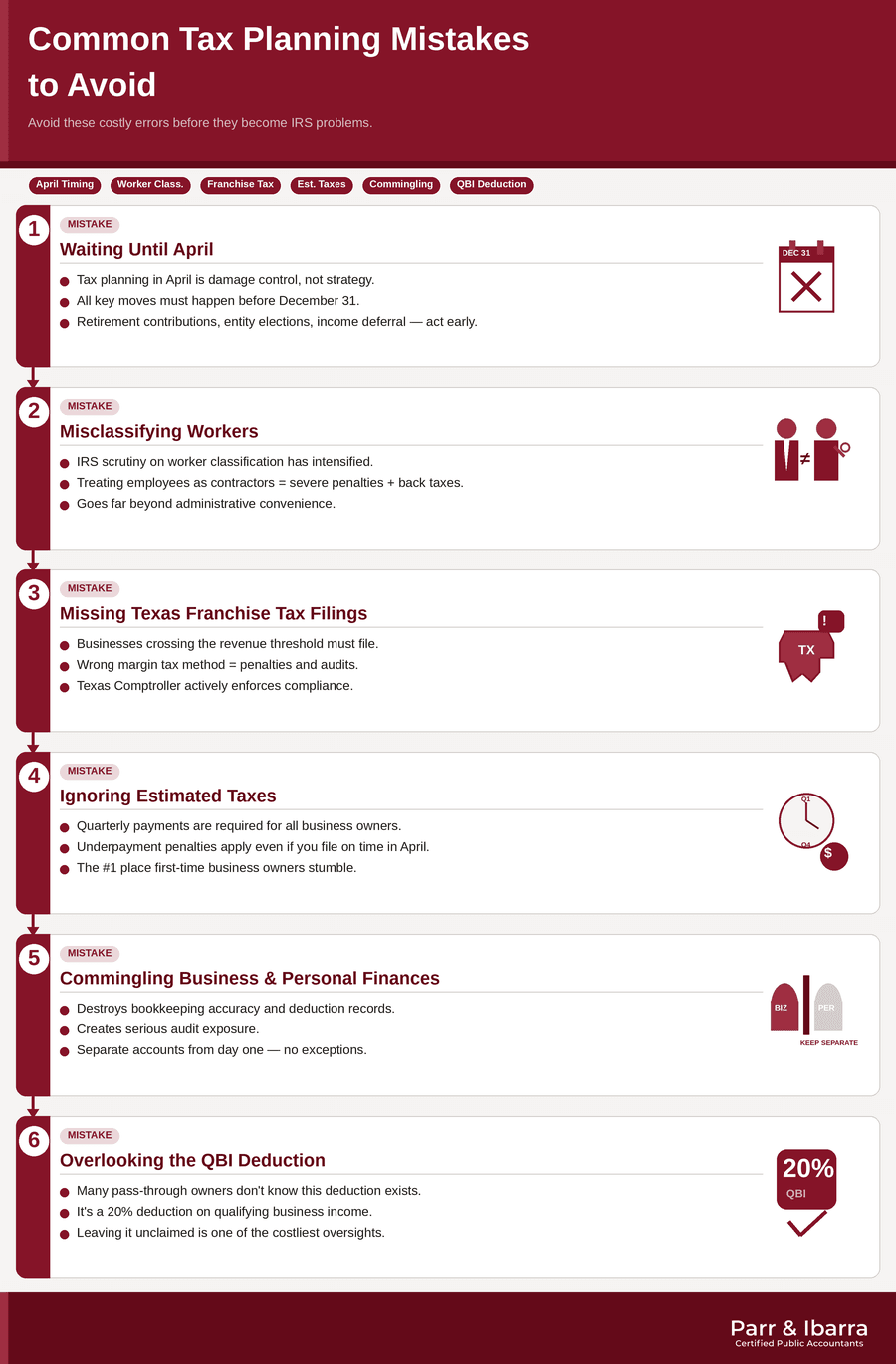

Waiting Until April: Tax planning done in April is damage control, not strategy. The best moves, retirement contributions, entity elections, depreciation timing, income deferral, all require action before December 31.

Misclassifying Workers: The IRS has intensified scrutiny of worker classification. The full tax implications of hiring employees versus 1099 contractors go far beyond administrative convenience. Treating employees as independent contractors to avoid payroll taxes is a common mistake with severe penalties and back-tax exposure.

Missing Texas Franchise Tax Filings: Texas businesses that cross the revenue threshold and fail to file, or choose the wrong margin tax calculation method, face penalties and potential audits from the Texas Comptroller.

Ignoring Estimated Taxes: Business owners and self-employed professionals who do not pay quarterly estimated taxes face underpayment penalties regardless of whether they file on time in April. Knowing how to make federal tax payments correctly and on schedule is foundational compliance, but it is consistently where first-time business owners stumble.

Commingling Business and Personal Finances: This is one of the most expensive habits a small business owner can have. It destroys bookkeeping accuracy, makes deductions difficult to substantiate, and creates audit exposure. Building sound bookkeeping habits from the start and understanding exactly what business records to keep and for how long are the two practices that keep your deductions clean and your books audit-ready.

Overlooking the QBI Deduction: Many pass-through business owners still do not know this deduction exists or assume they do not qualify. Leaving a 20% deduction unclaimed is a costly oversight. If you are uncertain whether your business qualifies, understanding how the IRS audits pass-through returns and what documentation matters gives you a clearer picture of how to substantiate your position before it is ever questioned.

When Should You Hire a CPA for Tax Planning?

The honest answer is: earlier than most people do.

If you are still filing a Schedule C as a sole proprietor with net income above $75,000, you have likely already outgrown DIY tax software. If you own a business with employees, hold investment properties, have equity compensation or stock options, or are planning to sell a business, the complexity of your situation demands professional guidance.

With IRS audit risks increasing in the current staffing environment, the case for having a qualified CPA in your corner before a problem arises has never been stronger. The ROI on professional tax planning is not measured in the cost of the engagement. It is measured in the taxes you do not pay, the penalties you never incur, and the strategies you would never have known to ask about.

Hiring a CPA in the middle of an IRS audit is not tax planning. Hiring one in January is a strategy. Hiring one in November, when there is still time to act, is the sweet spot.

Why Choose Parr & Ibarra CPA?

We are a full-service CPA firm serving Texas businesses, Dallas entrepreneurs, and high-income professionals who need more than a tax preparer. They need a strategic partner.

The firm brings deep expertise in federal and Texas tax law, business structuring, and proactive financial planning. Whether you are launching a startup in Uptown Dallas, managing a real estate portfolio across DFW, scaling a service business, or planning a business exit, our team brings the knowledge to move the needle. CFO-level financial guidance is increasingly essential for growing Texas businesses, and that depth of advisory thinking is built into how we support every client relationship, not just the ones at the largest scale.

Services include comprehensive tax planning and preparation, bookkeeping and financial reporting, business advisory, CFO services for growing companies, and IRS audit representation and protection. Every client relationship begins with understanding your goals, not just your last tax return.

Clients choose Parr & Ibarra CPA because they want someone who knows the Texas business environment, understands the Dallas market, and treats their financial future with the seriousness it deserves.

Conclusion: Your Tax Strategy Starts Now

Tax planning is not a luxury for large corporations. It is a practical discipline that pays measurable returns for every business owner, investor, and professional willing to be intentional about it.

In 2026, the tools are better than they have been in years. Full bonus depreciation is back. SALT limits are higher. Estate exemptions are generous. Retirement contribution limits keep climbing. The question is whether you have a plan to use them.

Parr & Ibarra CPA works with clients throughout Dallas, across Texas, and nationwide to build tax strategies that reduce liability, ensure compliance, and support long-term financial growth.

Ready to stop overpaying? Schedule a consultation with us today and find out exactly how much you could be saving.

Frequently Asked Questions

What are the biggest tax law changes for 2026?

The most impactful 2026 changes include the reinstatement of 100% bonus depreciation, the SALT deduction cap raised to $40,000, standard deduction increases ($16,100 single / $32,200 married), an additional $6,000 deduction for taxpayers 65 and older, an estate tax exemption near $15 million, and expanded family tax credits. Business owners and investors with a proactive CPA can benefit substantially from all of these updates.

How can I legally reduce my taxes in 2026?

The most effective legal strategies include maximizing retirement contributions, deploying bonus depreciation on equipment and property, restructuring your business entity to minimize self-employment tax, using Donor-Advised Funds for charitable giving, executing 1031 exchanges on real estate sales, and claiming the Qualified Business Income deduction. A tailored plan built around your specific income profile is the most reliable approach.

Do Texas businesses get any special tax advantages?

Yes. Texas has no state personal income tax, which is one of the most significant structural advantages for high-income earners and business owners. However, Texas does impose a franchise tax (margin tax) on most business entities above a revenue threshold. The right margin tax calculation method can make a meaningful difference. Working with a CPA familiar with Texas tax law is important for maximizing your Texas-specific advantages.

Is 100% bonus depreciation still available in 2026?

Yes. Full first-year bonus depreciation has been reinstated for 2026, allowing businesses to immediately deduct 100% of qualifying property costs in the year the property is placed in service. This applies to most tangible personal property with a recovery period of 20 years or less. It is a significant opportunity for businesses making capital investments this year.

When should I hire a CPA for tax planning?

Ideally, before the end of the third quarter, so there is still time to make elections, restructure compensation, fund retirement accounts, and time income or deductions before year-end. If your income has grown significantly, if you own a business, or if you are dealing with investment income, real estate, or equity compensation, professional tax planning will almost certainly pay for itself multiple times over.

How does the raised SALT deduction cap affect Texas taxpayers?

Since Texas has no state income tax, the SALT benefit for most Texas taxpayers flows primarily through property tax deductions. The increase to $40,000 (subject to income-based phase-outs) is most valuable to Texans with multiple properties or significant property tax bills, which is common in the Dallas-Fort Worth market given local property values.

What is the Qualified Business Income (QBI) deduction and do I qualify?

The QBI deduction allows qualifying pass-through business owners (S-Corps, partnerships, sole proprietors) to deduct up to 20% of their qualified business income. Income thresholds and phase-outs apply, particularly for certain service businesses. With proper planning around W-2 wages and entity structure, many business owners who assume they do not qualify can structure their affairs to take full or partial advantage of this powerful deduction.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.