IRS Form 990 is defined as the annual information return that tax-exempt organizations must file with the IRS to maintain their nonprofit status and demonstrate public accountability. Every finance professional managing a nonprofit needs to understand which version applies, what the form discloses, and what happens when filings go wrong. The stakes are real: three consecutive missed filings trigger automatic revocation of tax-exempt status under Section 6033(j), with no warning from the IRS. This guide covers form selection, key reporting sections, deadlines, and the strategic value of getting your 990 right.

What does Form 990 mean for your nonprofit?

Form 990 is not a tax return in the traditional sense. Tax-exempt organizations do not pay federal income tax, so the form serves a different purpose: it is a public accountability document that tells the IRS, donors, and regulators how the organization earns and spends its money. The IRS uses it to verify that the organization still qualifies for tax-exempt status. Donors and grantmakers use it to evaluate financial health and governance before writing checks.

The form covers financial data, program descriptions, governance policies, and executive compensation. That combination makes it one of the most revealing documents a nonprofit produces each year. Filing it accurately is not optional. Filing it well is a competitive advantage.

Which version of Form 990 applies to your organization?

The IRS requires nonprofits to file based on gross receipts and asset thresholds, not on organizational type alone. The four main versions are:

- Form 990-N (e-Postcard): For organizations with gross receipts of $50,000 or less. This is the simplest filing, requiring only basic identifying information submitted electronically.

- Form 990-EZ: For organizations with gross receipts between $50,000 and $199,999 and total assets under $500,000. It covers income, expenses, and basic governance questions.

- Full Form 990: Required when gross receipts reach $200,000 or more, or when total assets reach $500,000 or more. This version includes detailed financial statements, compensation disclosures, and multiple schedules.

- Form 990-PF: Required for all private foundations regardless of size. It includes additional calculations for minimum distribution requirements and excise taxes.

Choosing the wrong version is one of the most common filing errors. An organization that qualifies for 990-EZ but files 990-N has technically failed to meet its reporting obligation.

Pro Tip: If your organization is near a threshold, file the higher-level form. Crossing into a new tier mid-year without adjusting your filing creates inconsistencies that attract IRS attention.

All Form 990 versions must be filed electronically as of 2026. Paper filing was phased out after the Taxpayer First Act took effect in 2020. Every version, from the simple e-Postcard to the full 990-PF, requires submission through an IRS-authorized e-file provider.

What are the key sections of the full Form 990?

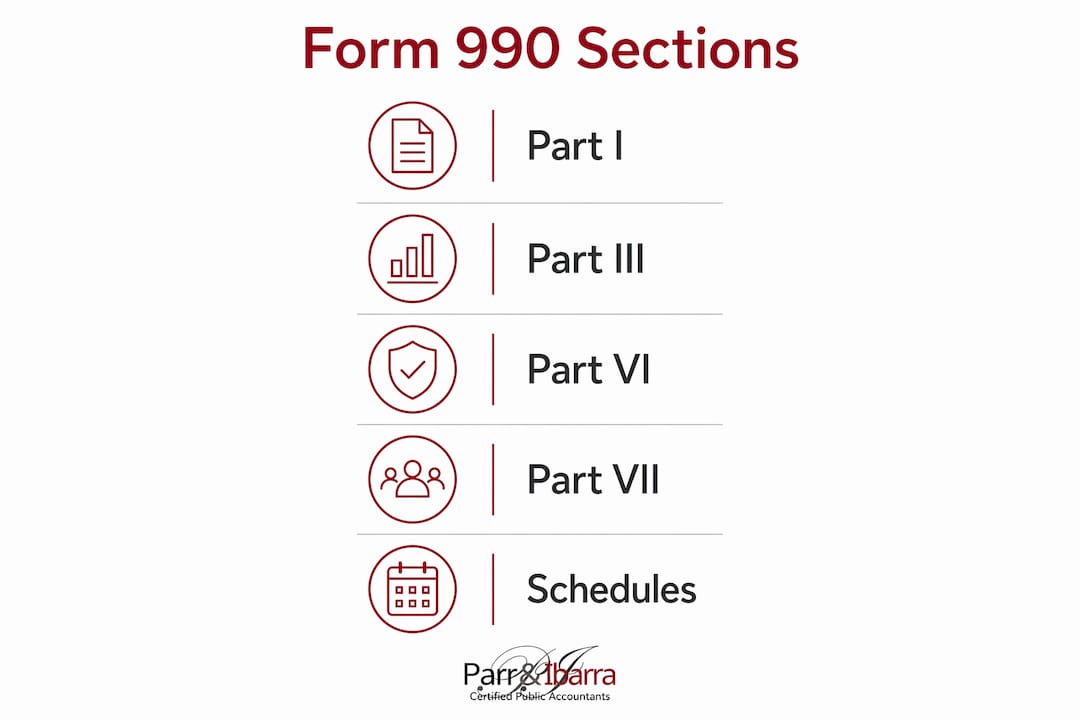

The full Form 990 contains eleven core parts plus schedules. Finance professionals responsible for preparation need to understand what each section communicates, not just what data it collects.

Part I: Summary provides a snapshot of the organization’s mission, governance structure, revenue, expenses, and net assets. Reviewers often start here before reading anything else.

Part III: Program Service Accomplishments is where the organization describes its charitable activities in narrative form. Vague or incomplete descriptions in this section are a common weakness. Specifying the number of people served, outcomes achieved, and dollars spent per program builds credibility with donors and grantmakers far more effectively than general language.

Part VI: Governance, Management, and Disclosure asks about board composition, meeting frequency, and written policies. The IRS tracks governance disclosures in Part VI as markers of organizational health. The absence of a conflict-of-interest policy or a whistleblower policy can trigger a closer review.

Part VII: Compensation requires disclosure of officer, director, and key employee compensation above specific thresholds. This section is frequently scrutinized by journalists and watchdog organizations.

Part IX: Statement of Functional Expenses breaks costs into program services, management, and fundraising. The allocation across these three categories signals how efficiently the organization uses its resources.

Common schedules include:

- Schedule A: Documents the public support test that determines whether a public charity maintains its status.

- Schedule B: Lists significant donors, though donor names are redacted from the public version.

- Schedule G: Reports fundraising events and activities, including gross receipts and direct expenses.

Pro Tip: Treat Part III as a marketing document, not a compliance checkbox. Grantmakers read program descriptions to decide whether your work aligns with their funding priorities.

How and when do you file Form 990?

The standard filing deadline is the 15th day of the fifth month after the organization’s fiscal year ends. For a calendar-year organization, that is may 15. Missing this date has real consequences.

The filing process follows these steps:

- Gather financial records for the full fiscal year, including bank statements, payroll records, and grant documentation.

- Reconcile financial statements to confirm that revenue and expense figures match your audited or reviewed financials.

- Complete all required schedules based on the organization’s activities, revenue sources, and governance structure.

- Conduct board review before submission. Many states require board approval of the Form 990 before filing.

- Submit electronically through an IRS-authorized e-file provider. Electronic filing is mandatory across all 990 versions.

- Retain a copy of the filed return and all supporting documentation for at least three years.

Organizations that need more time can request an automatic six-month extension using Form 8868. The extension applies to the filing deadline, not to any tax payment obligations.

Missing three consecutive years of required filings results in automatic revocation of tax-exempt status under Section 6033(j). Reinstatement requires reapplying for exemption, which is a lengthy and costly process. Late filing also triggers penalties calculated per day, with higher rates for larger organizations.

Pro Tip: Set a calendar reminder 90 days before your filing deadline. That window gives your CPA or finance team enough time to gather records, resolve discrepancies, and complete board review without rushing.

Why Form 990 is a public document that shapes your reputation

Most nonprofit leaders underestimate how quickly and widely their Form 990 circulates after filing. The return is publicly accessible through the IRS Tax Exempt Organization Search, ProPublica Nonprofit Explorer, and similar platforms within months of submission. Donors, journalists, regulators, and peer organizations all search these databases routinely.

“Form 990 preparation should be viewed as a branding opportunity to build donor trust and future funding, not just a compliance form. Every narrative description, governance disclosure, and expense allocation tells a story about how your organization operates.”

The practical implications are significant. A grantmaker reviewing your application will pull your most recent 990 before scheduling a meeting. A major donor considering a six-figure gift will check your executive compensation disclosures and program expense ratios. A journalist investigating nonprofit finances will start with ProPublica.

Common pitfalls that damage credibility include:

- Reporting fundraising expenses near zero despite running active solicitation campaigns.

- Showing unusually high administrative costs relative to program spending.

- Leaving governance policy questions blank or answering “no” without explanation.

- Providing vague program descriptions that do not quantify outcomes.

Treating the 990 as a transparency tool rather than a burden changes how finance teams approach preparation. Every section is an opportunity to demonstrate that the organization operates with integrity and delivers measurable results.

Common mistakes and best practices in Form 990 preparation

Preparation errors fall into two categories: technical mistakes that create compliance risk, and narrative weaknesses that undermine credibility. Both are avoidable.

The most frequent technical errors include filing the wrong form version, reporting inconsistent figures across the return and attached schedules, and omitting required schedules entirely. Inconsistencies between Part IX functional expenses and the organization’s audited financial statements are a particular red flag.

Governance disclosures in Part VI are frequently incomplete. Organizations that lack written conflict-of-interest policies, whistleblower protections, or document retention policies should address those gaps before filing, not after.

Fundraising expenses reported near zero despite active solicitation activity often trigger IRS scrutiny. The IRS expects reasonable allocation across program, management, and fundraising categories. Misallocating costs to appear more program-focused than the organization actually is creates both compliance and reputational risk.

Engaging a CPA for full Form 990 preparation is the right call for organizations with complex revenue streams, related-party transactions, or key employee compensation near IRS thresholds. Professional guidance reduces the risk of errors that invite scrutiny and protects board members from personal liability exposure. You can also review the right form for your entity with a qualified advisor before filing season begins.

Pro Tip: Keep board meeting minutes, conflict-of-interest disclosures, and financial reconciliations in a dedicated 990 preparation file throughout the year. Assembling documentation at filing time is slower and more error-prone than maintaining it continuously.

Key Takeaways

IRS Form 990 is the primary compliance and transparency tool for tax-exempt organizations, and filing it accurately protects both nonprofit status and donor trust.

| Point | Details |

|---|---|

| Form version selection | Choose 990-N, 990-EZ, full 990, or 990-PF based on gross receipts and total asset thresholds. |

| Mandatory e-filing | All Form 990 versions require electronic submission through an IRS-authorized provider as of 2026. |

| Three-year revocation rule | Missing three consecutive filings triggers automatic loss of tax-exempt status under Section 6033(j). |

| Public accessibility | Returns appear on IRS and ProPublica databases within months, visible to donors, media, and regulators. |

| Governance disclosures matter | Absent conflict-of-interest or whistleblower policies in Part VI can prompt IRS review and reduce grantmaker confidence. |

What I’ve learned from years of 990 filings

The organizations that treat Form 990 as a once-a-year scramble are the ones that end up with compliance problems and credibility gaps. I have seen well-run nonprofits lose major grants because their 990 showed administrative cost ratios that looked bad out of context, with no narrative explanation to clarify the numbers. The form gave an incomplete picture, and the organization paid for it.

The detail that surprises most finance professionals is how closely grantmakers read Part III. They are not just checking boxes. They are comparing your program descriptions against your expense allocations to see whether the numbers tell the same story as the words. When they do not align, it raises questions that are hard to answer after the fact.

My strongest recommendation is to integrate 990 preparation into your annual financial calendar, not treat it as a separate project. Organizations that reconcile their functional expense allocations quarterly, maintain governance documentation year-round, and review compensation disclosures with their board in advance file more accurate returns and face fewer follow-up questions. The 2026 IRS filing requirements have not made this easier, which is exactly why professional support pays for itself.

— Adan

Nonprofit tax compliance support from Parr & Ibarra CPA

Filing Form 990 accurately requires more than downloading the right form. It requires reconciled financials, documented governance policies, and a clear understanding of which schedules apply to your organization’s activities.

Parr & Ibarra CPA works with nonprofit organizations and business owners across the Dallas-Fort Worth area to prepare accurate, complete 990 filings and build year-round compliance workflows. The team of over 20 professionals, including multiple CPAs, brings the depth of a large firm with the attention of a local practice. Whether you need help selecting the right form version, reviewing compensation disclosures, or building a filing calendar, the team is ready to help. Start with the nonprofit tax planning guide to see how proactive planning reduces compliance risk and supports long-term financial health.

FAQ

What is IRS Form 990?

Form 990 is the annual information return that tax-exempt organizations file with the IRS to report financial data, program activities, and governance practices. It is a public document used by donors, regulators, and grantmakers to evaluate nonprofit transparency.

Who is required to file Form 990?

Most tax-exempt organizations under Section 501© must file a Form 990 series return each year, with the specific version determined by gross receipts and total assets. Churches and certain government entities are among the limited exceptions.

What happens if a nonprofit misses its Form 990 deadline?

Late filings trigger per-day penalties, and missing three consecutive years results in automatic revocation of tax-exempt status under Section 6033(j). Reinstatement requires a new exemption application.

Can Form 990 be filed on paper in 2026?

No. All Form 990 versions require electronic filing through an IRS-authorized e-file provider. Paper filing was eliminated after the Taxpayer First Act took effect in 2020.

Does the public have access to my organization’s Form 990?

Yes. Filed returns are searchable through the IRS Tax Exempt Organization Search and platforms like ProPublica Nonprofit Explorer, typically within months of submission.