Estimated quarterly taxes are periodic payments made directly to the IRS on income that no employer withholds taxes from, including self-employment earnings, freelance income, dividends, and rental income. The IRS calls this the pay-as-you-go system, and it applies to millions of freelancers, small business owners, landlords, and investors across the country. Missing these payments, or paying too little, triggers underpayment penalties even if you get a refund when you file. Form 1040-ES and the Electronic Federal Tax Payment System (EFTPS) are the two primary tools the IRS provides to manage these obligations.

What are estimated quarterly taxes and who must pay them?

Estimated quarterly taxes are advance tax payments covering income the IRS has not already collected through payroll withholding. The IRS divides the year into four payment periods, each with a specific due date. You owe estimated taxes if you expect to owe at least $1,000 in federal tax after subtracting withholding and credits.

The following income types most commonly trigger estimated tax obligations:

- Self-employment income from freelancing, consulting, or running a sole proprietorship

- Business income from partnerships, S corporations, or LLCs taxed as pass-through entities

- Investment income including dividends, capital gains, and interest

- Rental income from residential or commercial properties

- Alimony received under pre-2019 divorce agreements (still taxable under prior law)

Employees who also earn side income often fall into this category too. If your W-2 withholding does not cover the tax on your side business, you owe estimated payments on the gap.

Pro Tip: If you recently left a salaried job to go full-time freelance, your first quarterly payment is due the april 15 deadline, not at year-end. Missing that first installment starts the penalty clock immediately.

The IRS safe harbor rules offer a clear way to avoid penalties. You meet safe harbor if you pay at least 90% of your current year tax or 100% of your prior year tax, whichever is smaller. High earners with adjusted gross income above $150,000 must pay 110% of their prior year tax to qualify. These thresholds make prior-year tax a reliable planning floor, especially when your current-year income is hard to predict.

How to calculate your estimated quarterly tax payments

Accurate calculation starts with Form 1040-ES, which includes a worksheet for projecting your adjusted gross income, deductions, credits, and total tax for the year. The IRS recommends using your prior year tax return as a starting point. From there, you adjust for any expected income changes.

Two calculation methods work for most taxpayers:

- Prior year method. Take your total tax from last year’s Form 1040. Divide by four. Pay that amount each quarter. This method qualifies for safe harbor and requires almost no guesswork.

- Current year estimate method. Project your actual income, deductions, and credits for the current year. Use the Form 1040-ES worksheet to calculate the tax owed. Divide the result into four installments. This method is more accurate but requires more work and carries more risk if your income shifts.

Most self-employed individuals and small business owners start with the prior year method for safety, then switch to current year estimates once they have a clearer picture of their income.

Projecting income accurately is the hardest part. A freelance graphic designer who earned $80,000 last year but lands a major contract in march should revise estimates upward for the june 15 payment. A landlord who sells a rental property mid-year needs to account for the capital gain in that quarter’s estimate.

Pro Tip: Set a calendar reminder two weeks before each due date to review your year-to-date income. A quick comparison against your prior-year baseline takes 20 minutes and can save you hundreds in penalties.

You can re-calculate estimates mid-year using the Form 1040-ES worksheet whenever your income changes significantly. Waiting until april to reconcile everything is the most common and costly mistake. The IRS assesses penalties by installment, not annually, so a shortfall in the first quarter costs you even if you overpay in the fourth.

Common calculation pitfalls include forgetting self-employment tax (15.3% on net earnings up to the Social Security wage base), ignoring state estimated tax requirements, and failing to account for deductible business expenses that reduce taxable income. Tracking self-employed deductions throughout the year directly lowers your estimated tax bill.

When and how to pay estimated quarterly taxes

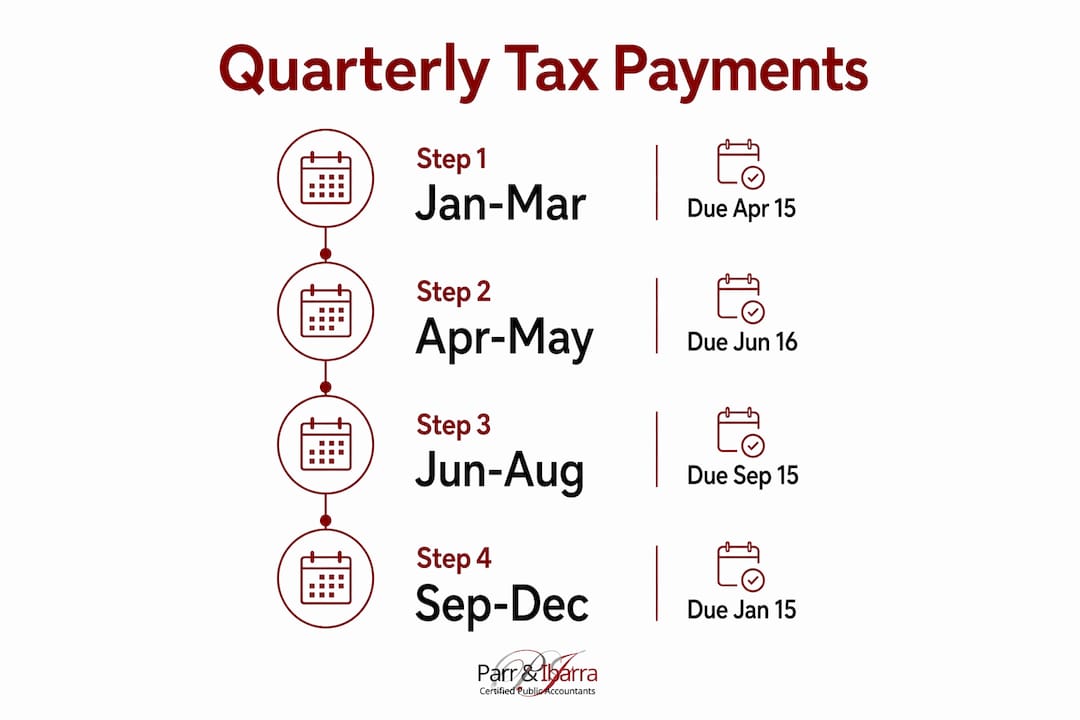

The four IRS quarterly due dates are not evenly spaced. That detail catches many first-time payers off guard.

| Payment Period | Due Date |

|---|---|

| January 1 – march 31 | april 15 |

| april 1 – may 31 | june 16 |

| june 1 – august 31 | september 15 |

| september 1 – december 31 | january 15 (following year) |

The second period covers only two months, while the fourth covers four. This uneven structure means the june payment often arrives before many business owners expect it. Mark these essential tax deadlines well in advance.

Payment methods include:

- EFTPS (Electronic Federal Tax Payment System). Free, secure, and available 24/7 online or by phone. You can schedule payments up to a year in advance, which removes the risk of forgetting a due date.

- IRS Direct Pay. Free bank transfer directly from your checking or savings account at IRS.gov.

- Mailing a check with Form 1040-ES voucher. The traditional paper method. Allow at least five business days for delivery.

- Credit or debit card. Available through IRS-authorized payment processors, though processing fees apply.

The IRS allows weekly, bi-weekly, or monthly payments as long as the total for each quarter is paid by the due date. A restaurant owner with strong weekend revenue might pay a small amount every Monday rather than scrambling for a large lump sum in april. That flexibility is underused and genuinely valuable.

What are IRS safe harbor rules and how do they prevent penalties?

Safe harbor rules define the minimum payment amounts that protect you from underpayment penalties, regardless of what you ultimately owe. The IRS assesses underpayment penalties by installment, not at year-end. That means paying the full annual amount in december does not erase a shortfall from april.

| Safe Harbor Rule | Requirement | Best For |

|---|---|---|

| 90% current year rule | Pay 90% of this year’s total tax | Taxpayers whose income is predictable |

| 100% prior year rule | Pay 100% of last year’s total tax | Taxpayers with variable or growing income |

| 110% prior year rule | Pay 110% of last year’s total tax | Taxpayers with AGI above $150,000 |

The 100% and 110% prior year rules are the most practical for small business owners. They let you base payments on a known number rather than a projection. The IRS safe harbor rules function as a penalty floor, not a tax ceiling. You may still owe more at filing, but you will not owe a penalty.

A common misconception is that filing your return and paying the balance due in april eliminates any penalty exposure. It does not. The penalty clock starts from each installment’s due date. A freelancer who underpaid in april and june will owe penalties on those two installments even if they pay everything owed by the following april 15.

Proactively meeting safe harbor thresholds before each due date is the most reliable penalty avoidance strategy available to self-employed individuals and small business owners.

How do you manage estimated taxes with uneven income?

Uneven income is the norm for freelancers, seasonal businesses, and commission-based earners. The IRS provides a specific tool for this situation: the annualized income installment method, calculated on IRS Form 2210, Schedule AI.

The annualized method works by calculating your actual income for each period of the year, annualizing it, and computing the tax owed on that annualized figure. This prevents overpaying in slow quarters and underpaying in busy ones. A landscaping company that earns 80% of its revenue between april and september benefits directly from this approach.

Practical strategies for managing variable income include:

- Re-estimate every quarter. Use the Form 1040-ES worksheet after each quarter closes to update your projection based on actual year-to-date income.

- Pay more frequently. Weekly or monthly payments tied to actual cash flow prevent large lump-sum payments from straining your finances.

- Build a tax reserve. Set aside a fixed percentage of every payment you receive into a dedicated savings account. Many CPAs recommend 25%–30% for self-employed individuals, though the right percentage depends on your deductions and filing status.

- Adjust after major income events. A large project payment, a property sale, or a new client contract should trigger an immediate estimate revision, not a year-end surprise.

Flexible payment timing is a genuinely underused IRS provision. Most taxpayers assume they must pay one lump sum per quarter. Spreading payments across the quarter smooths cash flow without any penalty risk, as long as the quarterly total is met by the due date.

Key Takeaways

Estimated quarterly taxes require proactive planning by each installment due date. Waiting until april to reconcile shortfalls does not prevent penalties assessed on earlier installments.

| Point | Details |

|---|---|

| Who must pay | Anyone expecting to owe $1,000 or more after withholding and credits must make estimated payments. |

| Safe harbor threshold | Pay 100% of prior year tax (110% if AGI exceeds $150,000) to avoid underpayment penalties. |

| Calculation starting point | Use Form 1040-ES with prior year return data, then adjust mid-year as income changes. |

| Payment flexibility | The IRS allows weekly or monthly payments as long as quarterly totals are met by each due date. |

| Penalty timing | Penalties accrue from each installment’s due date, not from the annual filing deadline. |

What I have learned from watching business owners get this wrong

Working with small business owners and freelancers across the Dallas-Fort Worth area, I have seen the same pattern repeat itself. Someone has a great year, earns significantly more than expected, and then faces a painful surprise in april: not just a large tax bill, but an underpayment penalty on top of it. The penalty feels arbitrary because they paid their taxes. They just paid them too late.

The most damaging misconception I encounter is that estimated taxes are optional until filing. They are not. The IRS penalty clock starts from each installment due date. A strong fourth quarter does not cancel out a missed first quarter payment.

The second mistake is treating estimated taxes as a once-a-year calculation. Income changes. A new contract, a slow month, a property sale, all of these shift your tax liability. Reviewing your estimate every quarter takes less time than most people think, and it prevents the compounding problem of carrying an underpayment forward through multiple periods.

The EFTPS system makes this easier than it has ever been. You can schedule payments in advance for the entire year in a single session. That removes the human error of forgetting a june deadline during a busy season.

My honest recommendation: use the prior year safe harbor as your baseline, review your actual income each quarter, and adjust upward when you have a strong period. That approach will not produce a perfect estimate, but it will keep you out of penalty territory while you build a more accurate picture of your annual tax liability.

— Adan

Tax planning support from Parr & Ibarra CPA

Estimated tax planning is one of the areas where working with a CPA pays for itself most clearly. A missed installment or an inaccurate estimate can cost more than the professional fee to get it right.

Parr & Ibarra CPA works with individuals and small business owners across the Dallas-Fort Worth area to build proactive tax plans that account for estimated payments, safe harbor thresholds, and mid-year income changes. The team of over 20 professionals, including multiple CPAs, handles everything from quarterly tax planning to year-round bookkeeping and payroll support. The IRS Tax Filing Guide 2026 on the Parr & Ibarra CPA website is a practical starting point for understanding your filing and payment obligations this year. For personalized guidance, contact Parr & Ibarra CPA directly to schedule a consultation.

FAQ

Who is required to pay estimated quarterly taxes?

Any individual who expects to owe at least $1,000 in federal tax after withholding and credits must make estimated tax payments. This includes freelancers, self-employed individuals, landlords, and investors with significant unwithheld income.

What happens if you miss an estimated tax payment?

The IRS assesses an underpayment penalty starting from the installment due date, not from your annual filing date. Paying the full balance in April does not eliminate penalties already accrued on earlier missed installments.

What is the safest way to calculate estimated taxes?

The prior year safe harbor method is the most reliable approach. Pay 100% of your prior year tax in four equal installments (110% if your adjusted gross income exceeded $150,000) to avoid penalties regardless of what you ultimately owe.

Can you pay estimated taxes more than once per quarter?

Yes. The IRS permits weekly, bi-weekly, or monthly payments as long as the total for each quarter is paid by the quarterly due date. This flexibility helps taxpayers with variable income manage cash flow without penalty risk.

What is Form 1040-ES used for?

Form 1040-ES is the IRS worksheet used to calculate your estimated tax payments. It projects your adjusted gross income, deductions, and credits for the year and can be used to revise estimates mid-year when your income changes.