A tax-efficient owner compensation strategy is defined as the deliberate structuring of how a business owner pays themselves, combining a reasonable W-2 salary with distributions, retirement contributions, and fringe benefits to reduce total tax liability. For S-Corp owners, this approach directly cuts payroll taxes, which apply only to salary and not to distributions. The IRS Section 199A qualified business income (QBI) deduction adds another layer of planning, since salary reduces the profit base eligible for that 20% deduction. Getting this balance right in 2026 requires understanding IRS reasonable compensation rules, Solo 401(k) limits, and the QBI phaseout thresholds that affect your specific situation.

What is a tax-efficient owner compensation strategy?

Owner compensation optimization starts with one foundational rule: the IRS requires S-Corp owner-employees to receive a reasonable W-2 salary before taking distributions. This is not optional. The IRS applies a nine-factor facts-and-circumstances test that examines your job role, hours worked, credentials, company performance, and what comparable employees earn in your market. Owners who pick a salary number purely to save taxes, without documentation to back it up, fail audits at a much higher rate than those who use external benchmarks.

Reasonable compensation is not a fixed percentage of profit. It is a defensible figure built from documented job descriptions, estimated hours, and credible market data. Three common methods exist for calculating it: the market method (what would you pay someone else to do your job), the cost method (what it would cost to replace your functions), and the income method (what portion of business income your personal effort generates). Each method produces a different number, and the right answer often blends all three.

Pro Tip: Document your compensation methodology in a written memo before your first paycheck of the year. Retroactive salary adjustments are a major audit red flag and significantly harder to defend.

The documentation standard matters as much as the number itself. A contemporaneous compensation memo describing your duties, hours, and the benchmarks you used gives you a clear paper trail. Annual reviews that adjust salary for business growth or role changes show the IRS that your process is systematic, not reactive.

- Use Bureau of Labor Statistics wage data or industry salary surveys as external benchmarks

- Record the specific job functions you perform, not just your title

- Note any credentials, licenses, or specialized skills that justify your pay rate

- Conduct a formal written review at least once per year

- Keep records of any compensation committee decisions or board approvals

How does the salary-to-distribution split affect your taxes?

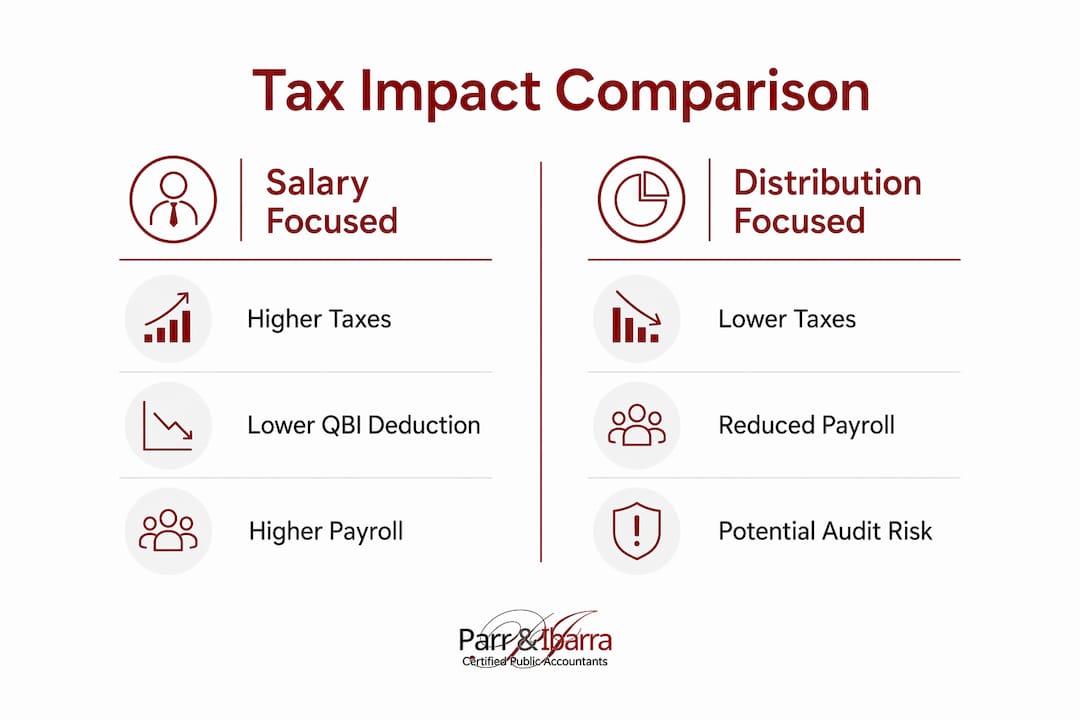

The core mechanic of owner compensation optimization in an S-Corp is straightforward. Payroll taxes (Social Security and Medicare) apply only to your W-2 salary. Distributions flow to you tax-free from a payroll tax perspective. On a $150,000 profit, splitting income between salary and distributions can save approximately $10,710 in self-employment taxes compared to treating all income as earned income.

The QBI deduction adds a competing pressure. The Section 199A deduction allows up to 20% of qualified business income, but your W-2 salary does not count as QBI. Every dollar you pay yourself in salary reduces the profit pool eligible for that deduction. This means a higher salary saves payroll taxes but shrinks your QBI deduction. A lower salary preserves more QBI but increases audit risk and reduces retirement plan contribution capacity.

The QBI phaseout begins at $197,300 for single filers and $394,600 for joint filers in 2026 for specified service trades and businesses. Above those thresholds, the deduction phases out entirely. Owners in that income range need to model the exact salary level that maximizes combined tax savings across payroll taxes and the QBI deduction.

| Scenario | Salary | Distributions | Payroll Tax Savings | QBI Deduction Impact |

|---|---|---|---|---|

| All salary | $150,000 | $0 | None | None |

| Balanced split | $80,000 | $70,000 | ~$10,710 saved | Moderate QBI preserved |

| Salary too low | $30,000 | $120,000 | Higher short-term savings | Audit risk, reduced retirement cap |

Finding the sweet spot requires running actual numbers for your business. The right salary is the one that satisfies the IRS reasonable compensation standard while leaving enough profit in distributions to reduce payroll taxes and preserve QBI. That number is different for every owner, every year.

How do retirement plans and fringe benefits multiply tax savings?

Retirement plan contributions are one of the most powerful tools in any business owner tax strategy. The 2026 Solo 401(k) allows employee contributions up to $24,000, plus an employer contribution of up to 25% of net profit, for a combined maximum of $72,000. Defined benefit plans go further, allowing deductible contributions over $200,000 for older owners in high-income years.

Your salary level directly controls how much you can contribute to these plans. A salary that is too low caps your employer contribution calculation and limits total retirement funding. This is the hidden cost of chasing the lowest possible salary. Owners who set salary artificially low to save payroll taxes often reduce retirement plan funding and lose more in long-term wealth than they saved in short-term taxes.

Pro Tip: Model your retirement contribution ceiling before finalizing your salary. A $10,000 increase in salary might cost $1,530 in payroll taxes but unlock $15,000 in additional deductible retirement contributions.

Fringe benefits add another layer of tax-free compensation. The IRS allows several benefits that are deductible to the business and tax-free to you as the owner-employee:

- Health Savings Accounts (HSAs): deductible contributions up to $4,400 for individuals or $8,750 for families in 2026

- Educational assistance: businesses can pay up to $5,250 per year toward an employee’s education, completely tax-free

- Group health insurance premiums paid by the business reduce taxable income directly

- Accountable plan reimbursements for home office, mileage, and business expenses shift personal costs to the business

These benefits do not show up on your W-2 as taxable income, which means they reduce your adjusted gross income without reducing your QBI base. For a detailed look at how these fit into small business tax planning, the interaction between fringe benefits and overall compensation design is worth reviewing carefully.

What audit risks come with owner compensation, and how do you defend against them?

The IRS targets S-Corp owners who pay themselves unusually low salaries. The agency has won multiple court cases against owners who took minimal W-2 wages while pulling large distributions. The pattern is well-documented, and it remains one of the most common triggers for S-Corp audits.

The most common mistakes that invite scrutiny include:

- Salary set as a round number with no supporting documentation

- Irregular payroll cadence (paying yourself quarterly or annually instead of biweekly)

- Salary that drops significantly in a profitable year without explanation

- No written job description or compensation memo on file

- Retroactive salary adjustments made after the tax year closes

Compensation planning requires balancing tax efficiency with retirement and household financial goals. The lowest tax approach is often suboptimal in the long run, and the IRS knows exactly what it looks like.

Audit defense starts before the first paycheck. A written compensation memo, external benchmark data, and a consistent payroll schedule are the three pillars of a defensible position. Parr & Ibarra CPA prepares formal reasonable compensation reports for clients that document the methodology, the market data, and the rationale, giving owners a clear record to present if the IRS ever asks questions. Owners who work with tax professionals to build this documentation upfront face significantly less risk than those who reconstruct records after the fact.

How do you implement an owner compensation plan step by step?

A structured process removes guesswork and creates a defensible record from day one.

Assess your business profitability and role. Calculate net profit before owner compensation. List every function you perform in the business, from operations to sales to finance. Complexity and hours worked both affect what the IRS considers reasonable.

Research market compensation. Pull salary data from Bureau of Labor Statistics occupational surveys, industry associations, or compensation databases for your specific role and geography. Document the sources you used and the date you pulled the data.

Set salary before your first paycheck. Write a compensation memo that records your job duties, hours, credentials, and the market data you reviewed. Sign and date it. This document is your first line of defense in any audit.

Determine your distribution amount. After salary is set, calculate remaining profit available for distributions. Run the QBI deduction math to confirm you are not leaving money on the table by over-paying salary.

Max out retirement contributions. Use your salary level to calculate the maximum Solo 401(k) or defined benefit plan contribution. Fund it fully before year-end. This is where S-Corp retirement planning pays off most directly.

Layer in fringe benefits. Set up an HSA, review educational assistance options, and confirm your accountable plan covers legitimate business expenses. Each benefit reduces taxable income without touching your QBI base.

Review quarterly and adjust at year-end. If business income changes significantly, revisit your salary. A mid-year adjustment is defensible if documented. A retroactive adjustment after the books close is not.

Pro Tip: Treat your compensation review as a formal meeting. Put it on the calendar, write up the outcome, and keep the notes with your tax records. The IRS responds well to evidence of a systematic process.

Key Takeaways

A tax-efficient owner compensation strategy requires setting a documented, IRS-defensible salary, then layering distributions, retirement contributions, and fringe benefits to minimize total tax liability and build long-term wealth.

| Point | Details |

|---|---|

| Reasonable salary is non-negotiable | The IRS requires a defensible W-2 salary backed by market data and written documentation. |

| Salary-distribution balance drives savings | Splitting profit between salary and distributions can save over $10,000 in payroll taxes on a $150,000 profit. |

| Retirement contributions amplify the strategy | Solo 401(k) limits reach $72,000 in 2026; salary level directly controls how much you can contribute. |

| Fringe benefits reduce taxable income tax-free | HSAs, educational assistance, and accountable plans cut taxes without reducing your QBI deduction base. |

| Documentation is your audit defense | A compensation memo written before the first paycheck is the single most effective audit protection tool. |

Why I think most owners get this backwards

Most business owners I work with come in focused on one question: “What is the lowest salary I can pay myself?” That is the wrong starting point. The right question is: “What salary produces the best total outcome across payroll taxes, QBI deduction, retirement contributions, and audit risk?”

I have seen owners save $8,000 in payroll taxes by setting a low salary, then lose $20,000 in retirement contribution capacity and face a $15,000 IRS assessment two years later. The math does not work when you only look at one variable. Compensation design is a system, not a single lever.

The owners who come out ahead treat their salary as a planning anchor. They set it with documentation, fund their retirement plan to the ceiling, use every legal fringe benefit available, and then take distributions on top. They also review the number every year because business income changes, and a salary that was reasonable at $200,000 in profit may not be reasonable at $400,000.

The household financial planning dimension matters too. A salary that is too low can hurt your mortgage application, reduce your Social Security benefit at retirement, and create cash flow instability if distributions are not disciplined. Compensation is not just a tax decision. It is a personal finance decision that happens to have tax consequences.

Work with a CPA who will model the full picture, not just the payroll tax savings. The difference between a good compensation plan and a great one is usually found in the retirement contribution math and the fringe benefit stack, not in how low you can push your salary.

— Adan

How Parr & Ibarra CPA helps you structure owner pay

Parr & Ibarra CPA works directly with Dallas-Fort Worth business owners to build compensation plans that hold up to IRS scrutiny and produce real tax savings year after year.

The team at Parr & Ibarra CPA prepares formal reasonable compensation reports, models the salary-to-distribution split for your specific income level, and integrates retirement plan contributions and fringe benefits into a single plan. Every engagement includes audit defense documentation so you are never caught without a paper trail. If you want a personalized tax planning review that covers your compensation structure, retirement goals, and 2026 tax position, Parr & Ibarra CPA is ready to build that plan with you. Reach out to the team at aibarra.cpa to get started.

FAQ

What is a reasonable salary for an S-Corp owner?

A reasonable salary is a defensible W-2 wage based on your job duties, hours worked, credentials, and market data for comparable roles. The IRS uses a nine-factor test and rejects salaries chosen purely to minimize payroll taxes.

How does owner salary affect the QBI deduction?

Your W-2 salary reduces the profit eligible for the Section 199A QBI deduction, which allows up to 20% of qualified business income. Setting salary too high shrinks the deduction; setting it too low invites IRS scrutiny and caps retirement contributions.

What are the Solo 401(k) contribution limits for 2026?

The 2026 Solo 401(k) allows employee contributions up to $24,000 plus an employer contribution of up to 25% of net profit, for a combined maximum of $72,000. Your W-2 salary level directly determines the employer contribution ceiling.

How do I protect myself from an IRS audit on owner compensation?

Write a compensation memo before your first paycheck, use external market data to support your salary, run payroll on a consistent schedule, and conduct a formal written review each year. Parr & Ibarra CPA prepares formal reasonable compensation reports that document your methodology and serve as audit-ready evidence.

Can fringe benefits reduce my taxable income as an owner?

Yes. HSA contributions up to $8,750 for families, educational assistance up to $5,250 per year, and accountable plan reimbursements are all deductible to the business and tax-free to you as the owner-employee.