There is an uncomfortable pattern that plays out regularly among successful Texas business owners. They spend a decade or more building income and almost no time building wealth. Those two things are not the same, and the gap between them tends to become painfully clear somewhere around age 55.

Income is what your business generates today. Wealth is what sustains you when it no longer needs to. The people who confuse one for the other tend to reach their later years with strong revenue, modest savings, and a tax bill that eats into whatever reserves they did manage to accumulate.

The good news is that 2026 has created some of the most favorable conditions in recent memory for retirement planning and wealth accumulation. New tax provisions, higher contribution limits, reinstated depreciation rules, and updated estate exemptions have opened a window that disciplined Texas business owners and investors can use to meaningfully accelerate their financial position. If you have been putting this conversation off because it feels complicated or premature, that instinct is costing you money every year you wait.

What Retirement and Wealth Planning Actually Involves

Retirement and wealth planning is the structured process of building, protecting, and eventually distributing financial assets in a way that fits your long-term personal and business goals. It is not simply opening a 401(k) or buying index funds, though both can be components of a broader strategy.

For business owners and investors, the process is considerably more involved. It requires coordinating your business structure, compensation strategy, tax planning, investment allocation, estate planning, and insurance coverage into a unified plan that grows alongside your life. Understanding how a CPA and financial advisor work together in this process is a good starting point, particularly if you have historically kept those conversations in separate silos.

Done well, a wealth plan answers several critical questions at once. How much income will you need in retirement, and where will it come from? How do you extract value from your business in the most tax-efficient way possible? What happens to your estate if something goes wrong unexpectedly? How do you protect assets from creditors, litigation, or economic downturns? And how do you minimize the tax drag across every stage of accumulation?

A CPA who understands both tax law and financial strategy is not optional in this process. For business owners especially, having that advisor involved from the beginning determines how much of what you build you actually get to keep.

Why 2026 Changes the Retirement Planning Conversation

The 2026 tax environment has shifted in ways that create both opportunities and real risks for high earners and business owners. The federal tax law updates for 2026 touch nearly every aspect of personal and business tax planning, but a few changes are particularly relevant to retirement and wealth strategy.

The estate tax exemption is near $15 million per individual: For many Texas business owners, the combined value of their company, real estate, and investment accounts is approaching or exceeding this threshold. Proper estate planning now, before values grow further or the exemption changes, is critical. Understanding what business owners specifically need to know about estate planning in this environment is worth prioritizing before values climb any further.

The senior deduction adds $6,000 for taxpayers 65 and older: Business owners in or near that age bracket now have an additional deduction that can offset income from required minimum distributions or continued business earnings. Combined with the standard deduction of $32,200 for married filers in 2026, a qualifying senior couple can exclude $38,200 from income before a single itemized deduction is claimed.

Tax brackets have adjusted upward by approximately 2.7%: For high earners, this creates a small but real window to recognize income, accelerate deductions, or execute Roth conversions at slightly more favorable rates than in prior years.

Charitable deduction rules have been updated: For business owners who give generously, the 2026 provisions offer more flexibility around cash donations, donor-advised funds, and qualified charitable distributions from IRAs. If philanthropy is already part of your wealth strategy, this year has opened up some useful angles worth reviewing with your CPA.

Texas has no personal state income tax: This foundational advantage means every dollar you contribute to a retirement account, every deduction you claim, and every dollar of income you defer generates savings exclusively at the federal level. In states like California or New York, those same strategies produce combined federal and state savings of 40 to 50 cents on the dollar or more. In Texas, your take-home after federal planning remains higher to begin with, and that gap compounds significantly over time.

Core Retirement Planning Strategies for Texas Business Owners

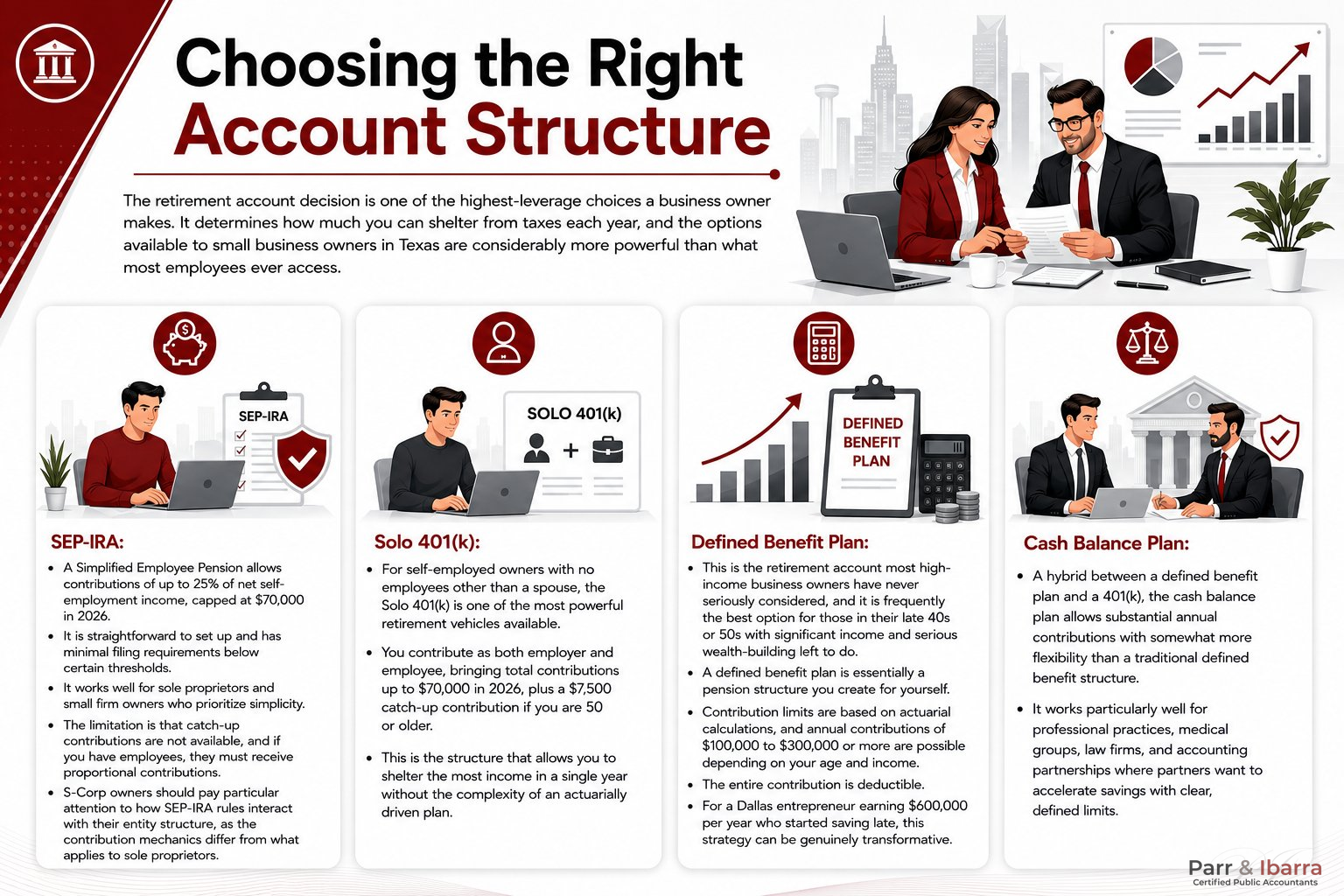

Choosing the Right Account Structure

The retirement account decision is one of the highest-leverage choices a business owner makes. It determines how much you can shelter from taxes each year, and the options available to small business owners in Texas are considerably more powerful than what most employees ever access.

SEP-IRA: A Simplified Employee Pension allows contributions of up to 25% of net self-employment income, capped at $70,000 in 2026. It is straightforward to set up and has minimal filing requirements below certain thresholds. It works well for sole proprietors and small firm owners who prioritize simplicity. The limitation is that catch-up contributions are not available, and if you have employees, they must receive proportional contributions. S-Corp owners should pay particular attention to how SEP-IRA rules interact with their entity structure, as the contribution mechanics differ from what applies to sole proprietors.

Solo 401(k): For self-employed owners with no employees other than a spouse, the Solo 401(k) is one of the most powerful retirement vehicles available. You contribute as both employer and employee, bringing total contributions up to $70,000 in 2026, plus a $7,500 catch-up contribution if you are 50 or older. This is the structure that allows you to shelter the most income in a single year without the complexity of an actuarially driven plan.

Defined Benefit Plan: This is the retirement account most high-income business owners have never seriously considered, and it is frequently the best option for those in their late 40s or 50s with significant income and serious wealth-building left to do. A defined benefit plan is essentially a pension structure you create for yourself. Contribution limits are based on actuarial calculations, and annual contributions of $100,000 to $300,000 or more are possible depending on your age and income. The entire contribution is deductible. For a Dallas entrepreneur earning $600,000 per year who started saving late, this strategy can be genuinely transformative.

Cash Balance Plan: A hybrid between a defined benefit plan and a 401(k), the cash balance plan allows substantial annual contributions with somewhat more flexibility than a traditional defined benefit structure. It works particularly well for professional practices, medical groups, law firms, and accounting partnerships where partners want to accelerate savings with clear, defined limits.

Roth Conversion Strategy

Roth conversions are one of the most discussed and least executed strategies in retirement planning. The concept is straightforward: you pay tax on pre-tax retirement funds today and move them to a Roth account where future growth and withdrawals are entirely tax-free. The question is always when to convert and how much.

In 2026, the answer depends on your current bracket, your projected retirement income, and your estate planning goals. For a Dallas entrepreneur who plans to sell a business in the next five years, the years before that exit event are often ideal for moderate conversions. Once the sale closes, income spikes and conversion costs rise sharply. Converting in lower-income years fills up lower brackets at today’s rates rather than paying higher rates later, when required minimum distributions can push income into territory you didn’t anticipate.

For owners approaching age 73, when RMDs begin, the math often favors converting enough each year to prevent RMDs from triggering higher brackets or Medicare premium surcharges. There are multiple strategies to reduce the tax impact of RMDs after age 73, and Roth conversions are often the most effective starting point.

Business Exit and Succession Planning

For most Texas business owners, the largest single asset on their personal balance sheet is the business itself. Yet fewer than 20% have a formal exit strategy. That gap is one of the most costly oversights in the entire wealth planning process.

A business exit strategy has to answer several questions at once. Do you plan to sell to a third party, transfer to a family member, or transition to a management team? What is the business worth today, and what would increase that valuation? What is the most tax-efficient structure for the sale, whether an asset sale, stock sale, installment agreement, or charitable remainder trust?

Each of these decisions carries significant tax implications. Understanding which exit strategy fits your business before you’re in active negotiations is the difference between a transaction you planned and one you simply reacted to. An outright sale at the top capital gains rate produces a very different outcome than a structured installment sale or a transfer to an intentionally defective grantor trust. Without planning, a Texas business owner who sells for $3 million may net $2.1 million. With the right structure in place years before the sale, the same transaction might yield $2.6 million or more.

Real Estate as a Wealth-Building Vehicle

Texas business owners and investors have a structural advantage in real estate wealth building that most people in high-tax states don’t fully appreciate. Rental income in Texas is subject only to federal tax. Combined with depreciation deductions, mortgage interest, and cost segregation strategies, a well-managed real estate portfolio can generate significant income at a very low effective tax rate.

For investors who qualify as real estate professionals under IRS rules, rental losses can offset ordinary income without the passive activity limitations that apply to most investors. This is a significant distinction that requires careful documentation of hours and participation. If you are a Dallas entrepreneur spending substantial time managing a rental portfolio, understanding how IRS classification affects your taxes as a real estate investor could change your entire tax picture. A thorough tax guide for landlords and real estate investors covers the practical implications of that designation in detail.

Advanced Wealth Planning Strategies

The Backdoor Roth IRA

High earners who exceed the Roth IRA income limits ($165,000 for single filers, $246,000 for married filers in 2026) can still access Roth treatment through a two-step process. You make a non-deductible contribution to a traditional IRA, then convert it to a Roth immediately. The backdoor Roth IRA has survived multiple IRS reviews and remains a viable option for high-income professionals and business owners who want tax-free growth going forward.

The complication arises if you have existing pre-tax IRA balances, which triggers the pro-rata rule and can result in unexpected taxable income. Your CPA needs to evaluate this before you execute the conversion, not after.

Qualified Opportunity Zone Investments

Texas has a meaningful number of designated Opportunity Zones, particularly in the Dallas, Houston, and San Antonio markets. Investors who roll capital gains into Qualified Opportunity Zone Funds within 180 days of the triggering event can defer the original gain, and eliminate tax entirely on appreciation generated within the fund after a 10-year hold. The 2026 updates to Qualified Opportunity Zone rules have introduced changes worth reviewing with a CPA before committing capital. For a Texas business owner who just sold a property or liquidated a large position, this strategy allows the full gain to keep compounding inside an investment rather than paying tax immediately on a smaller base.

Grantor Retained Annuity Trusts

With the estate tax exemption near $15 million, some Texas business owners may feel insulated from estate tax exposure. But business values grow, real estate appreciates, and the exemption is not permanent. A Grantor Retained Annuity Trust allows you to transfer future appreciation of a business or asset out of your estate with minimal gift tax implications. If the asset grows faster than the IRS hurdle rate, the excess passes to heirs free of estate tax. This strategy works best for business owners who believe their company or portfolio will appreciate significantly in the coming years and who want to begin transferring wealth while valuations are still manageable. Using a family limited partnership alongside trust structures can add another layer of planning flexibility for families with complex asset situations.

Charitable Remainder Trusts and Donor-Advised Funds

For business owners with philanthropic intentions, the 2026 updates to charitable contribution rules make this a good time to revisit how you give. A Charitable Remainder Trust allows you to donate a highly appreciated asset, receive an income stream for life, avoid capital gains on the sale inside the trust, and take a partial charitable deduction in the year of contribution. The remainder passes to your chosen charity at death.

A Donor-Advised Fund is simpler and increasingly common among high-income earners. You contribute cash or appreciated assets, take the full deduction in the year of contribution, and then direct grants to charities over time. Pairing RSUs or appreciated stock with a donor-advised fund is particularly powerful in high-income years, like a business sale year, where you want to maximize deductions immediately but distribute the giving gradually.

The Mistakes That Quietly Erode Wealth Over Time

Treating the business as the retirement plan: This is the most common and most damaging mistake among Texas business owners. The logic makes sense on the surface: “My business is worth $4 million. That is my retirement.” The problem is that business value is illiquid, unpredictable, and tied to conditions you cannot always control. A buyer may not appear when you want to exit. A key departure or economic shift can compress the valuation significantly. Qualified retirement accounts, real estate, and taxable investment accounts need to be built alongside the business, not instead of it.

Ignoring RMDs until they arrive: Required minimum distributions begin at age 73 under current rules. Understanding exactly how RMDs work before they start is the only way to plan around them effectively. For owners who have accumulated $1 million or more in pre-tax retirement accounts, RMDs can add $60,000 to $100,000 or more per year in taxable income at a time when passive income and continued business activity may already be pushing brackets upward. The resulting Medicare surcharges and bracket creep are entirely avoidable with proactive planning in the years before distributions are required.

Holding appreciated assets without a plan: A Dallas investor who bought commercial property in 2015 and has seen it appreciate by $1.5 million has a large embedded gain. Holding without a plan doesn’t make that gain disappear. It just delays the decision until circumstances force it, often at the worst possible time from a tax perspective. There are specific strategies to reduce capital gains tax on real estate that work best when implemented before a sale is imminent, not after a buyer has already signed a letter of intent.

Starting succession planning too late: Business succession planning that begins at 60 is a decade too late for most owners. Preparing a business for sale, identifying and training a successor, or transferring ownership to family members is a multi-year process. Owners who maximize their exit values are the ones who built transferable businesses, with documented systems, key-person independence, and clean financial records, long before they expected to sell. Understanding how taxes affect a merger or acquisition early in the process changes how you structure things, not just how you report them.

Overlooking how the wealthy actually build and protect wealth: Most high-income earners focus on earning more and invest relatively little effort in understanding how debt, leverage, and structure are used by wealthy individuals to reduce taxes and build wealth. These are not exotic strategies reserved for the ultra-rich. They are approaches that work at the $500,000 to $5 million level and are consistently underused by business owners who haven’t had that conversation with the right advisor.

How This Plays Out in Practice (illustrative)

The Dallas medical practice owner in her late 40s operates her practice as an S-Corp and earns $650,000 per year in W-2 income from the business. She had been contributing to a SEP-IRA but had not maximized her retirement savings. After a full review, her CPA recommended converting to a defined benefit plan combined with a 401(k). Total annual contributions jumped from $66,000 under the SEP to over $220,000 between the two plans. Her taxable income dropped from $650,000 to roughly $430,000, removing a significant portion of her income from the 37% bracket entirely. Over 10 years, the tax savings on contributions alone exceed $700,000 before accounting for the compounding effect inside the tax-sheltered accounts.

The Fort Worth real estate investor with eight residential rentals and a combined market value of $4.2 million had been using standard depreciation schedules across all properties. After qualifying as a real estate professional under IRS rules, a cost segregation study on three recently acquired properties captured approximately $380,000 in accelerated depreciation. A cost segregation study structured correctly for a real estate investor unlocked deductions that offset $180,000 in W-2 income from a prior position, and a Roth conversion of $120,000 was executed in the same year at a near-zero effective rate on that portion. The investor also began moving appreciated properties into a 1031 exchange structure to defer embedded gains while repositioning into more productive commercial assets.

The DFW tech entrepreneur, 38 years old, had built a software company valued at approximately $8 million with minimal personal retirement savings alongside it. A succession planning conversation revealed he hoped to sell in six to eight years. The plan focused on three parallel tracks: maximizing a Solo 401(k) annually, creating a GRAT to transfer future business appreciation above the IRS hurdle rate to his children, and making two real estate acquisitions in Dallas Opportunity Zones. By the time of the business sale, those three tracks will have materially reduced both his income tax and estate tax exposure on accumulated wealth. Tax strategies built specifically for founders at this stage of a company tend to look very different from generic retirement advice, and the specifics matter considerably.

When to Engage a CPA for Retirement and Wealth Planning

If you are earning more than $250,000 per year and don’t have a structured retirement contribution strategy in place, you are already behind. Not dangerously behind, but behind in a way worth correcting as soon as possible.

The clearest signals that it is time to bring in professional guidance: you are approaching a major income event such as a business sale, a real estate disposition, or a significant equity grant. You are within 10 years of your intended retirement date. You haven’t reviewed your retirement account structure in the past two years. Or you have never had a formal estate plan reviewed by a CPA alongside your attorney. Top tax strategies for high-income professionals can give you a sense of the planning landscape, but the real value comes from applying those strategies to your specific income, entity, and timeline.

The value of professional guidance here is not just compliance. It is the difference between a retirement funded by what is left after taxes and one funded by what was protected before taxes ever applied. That distinction, compounded over 20 or 30 years, often represents hundreds of thousands of dollars or more.

About Parr & Ibarra CPA

Parr & Ibarra CPA is a Dallas-based firm that combines deep tax expertise with the kind of strategic, long-range planning that high-income professionals and business owners actually need. The practice works with Dallas entrepreneurs across industries, commercial real estate investors throughout the DFW metro, medical and legal professionals, and family-owned businesses navigating succession and growth.

On retirement and wealth planning, the firm brings together core tax planning expertise with coordinated guidance on retirement account selection, business exit strategy, estate planning integration, and charitable giving structure. Every engagement is built around forward-looking strategy, not just preparation.

If you are looking for a CPA in Dallas Texas who treats your retirement plan as seriously as your tax return, schedule a consultation today. Visit Us to connect with an advisor who understands your market, your tax situation, and where you are trying to go.

Frequently Asked Questions

What 2026 tax changes matter most for retirement planning?

Several updates are directly relevant. The estate tax exemption has risen to approximately $15 million, affecting succession and gifting strategy. The additional $6,000 deduction for taxpayers 65 and older creates meaningful income reduction for seniors still earning active or passive income. Roth IRA income thresholds have increased, the standard deduction has risen to $32,200 for married filers, and charitable deduction rules now offer more flexibility for donor-advised funds and qualified charitable distributions. All of these interact with retirement account strategy in ways that are worth reviewing with a CPA.

How can Texas business owners legally reduce taxes through retirement planning?

The most direct methods involve maximizing contributions to qualified retirement accounts, which are fully deductible. Defined benefit and cash balance plans allow the largest annual contributions, sometimes exceeding $200,000 for high-income owners. Beyond contributions, Roth conversion strategies, strategic timing of income recognition, real estate depreciation, and charitable vehicles all reduce tax exposure across both the accumulation and distribution phases of retirement.

Do Texas businesses benefit from the absence of state income tax in retirement planning?

Significantly. Because Texas imposes no state income tax, every retirement account contribution generates savings at the federal rate only. In high-tax states, a $100,000 deduction might save $45,000 or more combined. In Texas, the federal savings are substantial on their own, and the absence of state taxation on retirement distributions means your income in retirement stretches further. This structural advantage makes consistent, maximized retirement contributions especially powerful for Texas-based earners.

Is it too late to start retirement planning at 50?

No. In many ways, starting focused planning at 50 with significant income is one of the highest-return financial decisions you can make. Catch-up contribution limits allow investors 50 and older to contribute an additional $7,500 to a 401(k). Defined benefit plans are particularly valuable for older high-income owners because actuarial calculations based on age allow much larger annual contributions than younger participants. The key is acting quickly rather than assuming the runway is too short to matter.

What is the right retirement account for a self-employed business owner in Texas?

It depends on income level, age, number of employees, and how aggressively you want to reduce taxable income. A Solo 401(k) is usually the best starting point for solo operators. A SEP-IRA is simpler but more limited. For high earners wanting maximum deductions, a defined benefit or cash balance plan can dwarf the contribution limits of any IRA or 401(k). The difference between the right choice and the wrong one can be $100,000 or more in annual deductions, which makes a CPA review worth the time before you commit to a structure.

When does a Roth conversion make sense?

The best time to convert is when your current year income is lower than expected, whether due to a business downturn, a gap between income events, or a year when large deductions are reducing your effective rate. Conversions also make sense in years before RMDs begin, when proactive conversion reduces the pre-tax balance and therefore the size of future required distributions. A CPA can model your projected income over the next 10 to 20 years and identify the optimal amounts and timing.

How do I protect retirement assets from creditors or lawsuits in Texas?

Texas has some of the strongest asset protection laws in the country. State law provides broad protection for IRAs and most qualified retirement plan assets from creditors in a bankruptcy proceeding. Combined with the right business entity structure, proper insurance coverage, and certain trust structures, a Texas business owner can build meaningful protection around both business and personal assets. This is an area where your CPA and your attorney should be coordinating together, not working independently.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.