Payroll is the systematic process businesses use to compensate employees accurately and comply with federal, state, and local tax laws. For small business owners and HR managers, getting it right means more than cutting checks. The IRS and the Department of Labor both impose strict recordkeeping, withholding, and reporting requirements that carry real penalties when missed. Payroll errors can trigger audits, financial losses, and damaged employee trust. Understanding the full scope of payroll processing, from gross wage calculation to tax remittance, is the first step toward running a business that stays compliant and keeps its people paid on time.

How to calculate payroll accurately

Calculating payroll starts with gross wages. For salaried employees, divide the annual salary by the number of pay periods. For hourly workers, multiply hours worked by the hourly rate, then add overtime at 1.5 times the regular rate for any hours beyond 40 in a workweek, as required by the Fair Labor Standards Act. Commissions, bonuses, and tips also count as gross wages and must be included before any deductions.

Once you have gross wages, federal withholdings come next. The IRS requires employers to withhold Social Security at 6.2% and Medicare at 1.45% from each employee’s paycheck. These rates apply to every W-2 employee, not independent contractors. That distinction matters enormously, because misclassifying workers as contractors when they function as employees exposes a business to back taxes, penalties, and interest.

State and local taxes follow federal withholdings. Texas has no state income tax, which simplifies things for Dallas-Fort Worth businesses, but other states require additional withholding tables and filing schedules. If your business operates across multiple states, each state’s rules apply independently.

Deductions come last. These fall into two categories: pre-tax deductions like health insurance premiums and 401(k) contributions, which reduce taxable income, and post-tax deductions like Roth contributions or wage garnishments. Garnishments require precise calculation to avoid legal liability that goes beyond IRS non-compliance. A single miscalculation on a court-ordered garnishment can result in the employer becoming personally liable for the unpaid amount.

The final figure after all withholdings and deductions is net pay. That is the amount deposited into the employee’s account or printed on their check.

Pro Tip: Set up a payroll calendar at the start of each year that maps every pay date, tax deposit deadline, and quarterly filing due date. The IRS requires most small businesses to deposit payroll taxes either monthly or semi-weekly, depending on their lookback period.

- Calculate gross wages (salary, hourly, overtime, commissions)

- Apply federal withholdings: Social Security (6.2%) and Medicare (1.45%)

- Apply state and local tax withholdings based on employee location

- Subtract pre-tax deductions (health insurance, 401k)

- Subtract post-tax deductions (Roth contributions, garnishments)

- Confirm net pay and schedule direct deposit or check issuance

What are the biggest payroll compliance challenges?

Compliance is where most small businesses get hurt. The rules governing payroll span federal law, state law, and sometimes local ordinances, and they change regularly. Missing a deposit deadline or applying the wrong withholding rate can result in penalties that compound quickly.

Payroll errors cause fines, financial losses, and loss of employee trust. That last consequence is often underestimated. An employee who receives a short paycheck or discovers a tax error on their W-2 loses confidence in the business. That erodes morale and increases turnover.

“Small payroll errors can cascade into audits, tax penalties, loss of trust, and disruption of critical business events. Payroll is a significant operational risk requiring cross-department collaboration among HR, finance, and tax.”

Common compliance failures include:

- Late new hire reporting: Federal law requires employers to report new hires to the state within 20 days of their start date. Missing this deadline can affect child support enforcement and trigger state fines.

- Incorrect withholding amounts: Using an outdated W-4 form or applying the wrong tax table results in under-withholding, which creates a tax liability for the employee and potential penalties for the employer.

- Misapplied deductions: Applying a pre-tax deduction to a benefit that does not qualify for pre-tax treatment creates a tax error that must be corrected on the employee’s W-2.

- Missed deposit deadlines: The IRS charges a failure-to-deposit penalty that starts at 2% and rises to 15% depending on how late the deposit is.

- Inadequate recordkeeping: The Fair Labor Standards Act requires employers to retain payroll records for at least three years. Missing records during an audit creates a presumption of non-compliance.

Understanding your payroll tax obligations before you hire your first employee is far less costly than correcting errors after the fact. Parr & Ibarra CPA works with Dallas-Fort Worth business owners specifically on these compliance gaps, because the cost of prevention is always lower than the cost of a penalty.

How do you choose the right payroll management software?

The right payroll management software depends entirely on how your business operates. A restaurant with 30 hourly employees needs time tracking and tip reporting. A professional services firm with salaried staff needs accounting integration and benefits administration. Software selection must match your operational needs, not just your headcount.

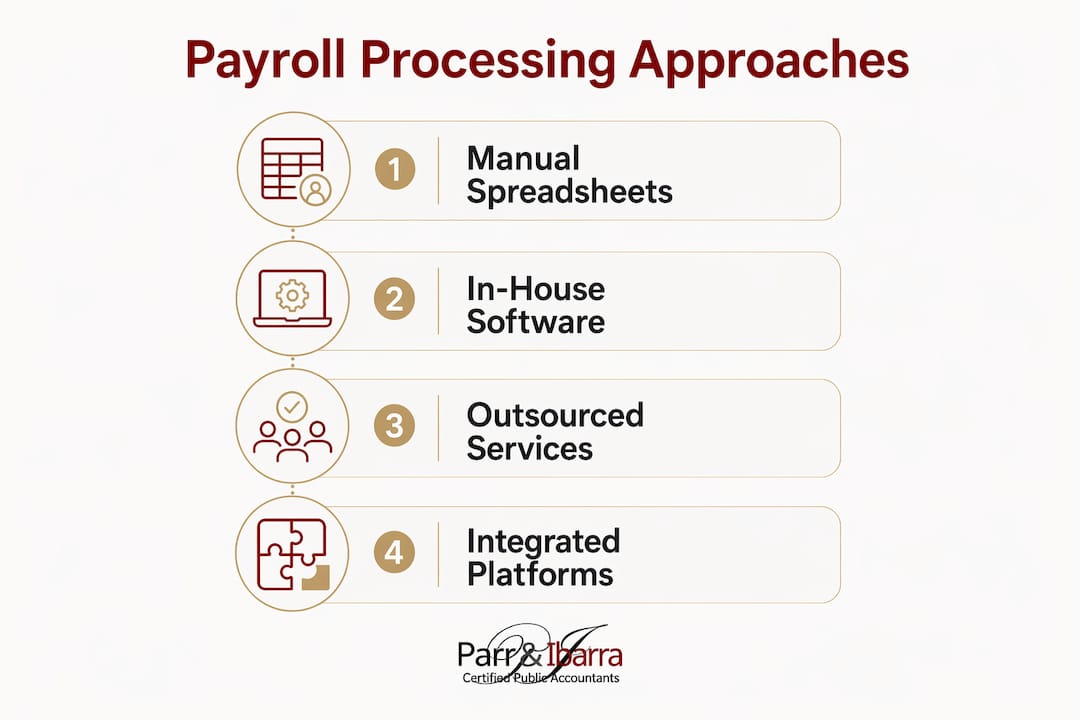

The four main approaches to payroll processing are manual spreadsheets, in-house software, outsourced services, and integrated cloud platforms. Manual spreadsheets carry the highest risk. Manual payroll is error-prone and lacks real-time compliance updates, which means a tax rate change or new state rule can go unnoticed until a penalty arrives.

| Approach | Best for | Key limitation |

|---|---|---|

| Manual spreadsheets | Solo operators with one or two employees | No compliance updates, high error risk |

| Entry-level payroll software | Small teams under 25 employees | Limited integration with accounting systems |

| Full-service outsourced payroll | Businesses without in-house HR expertise | Less control, higher cost at scale |

| Integrated cloud platform | Growing businesses with complex needs | Requires setup time and staff training |

Entry-level payroll software for small businesses starts at roughly $49 per month plus $2–$6 per employee. That pricing is accessible for most small businesses and far cheaper than the cost of a single IRS penalty. Cloud-based platforms also push compliance updates automatically, so your tax tables stay current without manual intervention.

Key features to evaluate when selecting a platform include tax filing automation, direct deposit, employee self-service portals, time and attendance tracking, and integration with accounting software like QuickBooks or Xero. Platforms that connect payroll directly to your general ledger eliminate double-entry errors and give your bookkeeper or CPA a clean audit trail.

Automated payroll software reduces processing time from several hours per pay period to under one hour. That time savings compounds across 26 biweekly pay periods per year, freeing HR managers to focus on higher-value work.

Pro Tip: Before committing to any platform, ask the vendor how it handles multi-state payroll and whether it files state tax returns on your behalf. Many entry-level tools handle federal filings but leave state compliance to you.

Best practices for payroll management in small businesses

Strong payroll management requires consistent habits, not just good software. The businesses that avoid audits and penalties are the ones that treat payroll as a recurring operational discipline, not a monthly scramble.

- Document your payroll policy in writing. Define pay periods, overtime rules, bonus eligibility, and deduction schedules. A written policy protects the business in disputes and gives HR a clear reference point.

- Verify employee information before every pay run. Confirm that W-4 elections, direct deposit accounts, and benefit enrollment details are current. An outdated W-4 from a life event like marriage or a new dependent is one of the most common sources of withholding errors.

- Reconcile payroll to your general ledger each period. Every payroll run should match the corresponding journal entries in your accounting system. Discrepancies caught early take minutes to fix. Discrepancies found during an audit take weeks.

- Maintain a complete audit trail. Store payroll registers, tax deposit confirmations, and employee change logs for at least four years. The IRS can audit employment tax returns up to three years after filing, and longer if fraud is suspected.

- Coordinate with HR and finance before making changes. A new benefit plan, a compensation adjustment, or an acquisition all affect payroll. Changes made in isolation create errors. Parr & Ibarra CPA recommends a pre-change review that includes HR, finance, and your CPA before any structural payroll modification takes effect.

Reviewing your estimated quarterly tax schedule alongside your payroll calendar also prevents cash flow surprises. Many small business owners separate these two tasks and then face a large tax payment they did not plan for.

Key Takeaways

Accurate payroll requires correct wage calculation, timely tax deposits, and consistent compliance practices across every pay period.

| Point | Details |

|---|---|

| Calculate gross to net correctly | Start with gross wages, apply federal and state withholdings, then subtract pre-tax and post-tax deductions. |

| Federal withholding rates are fixed | Social Security is 6.2% and Medicare is 1.45% for every W-2 employee, with no exceptions. |

| Compliance errors compound fast | Late deposits, misclassified workers, and missed filings trigger penalties that escalate quickly. |

| Software selection must fit your operations | Match platform features to your business type: time tracking for hourly teams, accounting integration for salaried firms. |

| Automation cuts processing time significantly | Cloud-based payroll platforms reduce per-period processing from several hours to under one hour. |

What I’ve learned from watching small businesses handle payroll

After working with dozens of small business owners in the Dallas-Fort Worth area, the pattern I see most often is this: payroll gets treated as a back-office task until something goes wrong. Then it becomes a crisis.

The businesses that struggle most are the ones that grew quickly and never updated their payroll processes to match. They started with a spreadsheet when they had three employees and kept using it when they had fifteen. By that point, the risk exposure is significant. Multi-state employees, garnishments, benefit plan changes, and new hire reporting requirements all pile up faster than a spreadsheet can handle.

What I tell every client is that payroll is not just about paying people. It is a compliance function that touches the IRS, the Department of Labor, state tax agencies, and your employees’ personal finances simultaneously. A mistake in any one of those areas creates a ripple effect. I have seen a single misclassified contractor trigger a full employment tax audit that consumed months of management time and tens of thousands of dollars in professional fees.

The move to cloud-based payroll platforms is not optional for growing businesses. It is the minimum viable standard for staying compliant without a dedicated payroll specialist on staff. The accounting automation benefits extend well beyond payroll itself, touching reconciliation, reporting, and audit readiness. The businesses I work with that have made this transition spend less time on payroll administration and more time on the decisions that actually grow their companies.

— Adan

How Parr & Ibarra CPA helps small businesses stay payroll-compliant

Running payroll correctly requires more than software. It requires someone who understands how payroll intersects with your tax strategy, your benefit elections, and your year-end filings.

Parr & Ibarra CPA works with small business owners and HR managers across the Dallas-Fort Worth area to build payroll processes that hold up under scrutiny. The team of over 20 professionals, including multiple CPAs, reviews withholding accuracy, coordinates payroll with quarterly tax planning, and flags compliance risks before they become penalties. Whether you need help setting up a new payroll system or cleaning up errors from a prior period, the firm offers hands-on support tailored to your business size and structure. Start with the firm’s tax planning best practices to see how payroll fits into a broader financial strategy, or review the 2026 tax planning strategies for updates specific to this year.

FAQ

What is payroll and why does it matter for small businesses?

Payroll is the process of calculating employee wages, withholding taxes, and distributing net pay on a defined schedule. For small businesses, it also determines compliance with IRS, Department of Labor, and state tax agency requirements.

How do I calculate federal payroll taxes?

Withhold Social Security at 6.2% and Medicare at 1.45% from each employee’s gross wages, then match those amounts as the employer. These rates apply to all W-2 employees and are set by the IRS.

What are the most common payroll compliance mistakes?

The most common errors include late tax deposits, incorrect worker classification, outdated W-4 withholding elections, and misapplied deductions like garnishments. Each carries its own penalty structure from the IRS or state agencies.

How long do I need to keep payroll records?

The IRS requires employers to retain employment tax records for at least four years after the tax is due or paid. State requirements vary, so check your state’s rules in addition to the federal standard.