Capital gains tax is a federal tax on the profit you earn when you sell or dispose of an asset for more than you originally paid for it. The IRS applies this tax to a wide range of assets, including stocks, bonds, mutual funds, real estate, and collectibles. Understanding how capital gains tax works is not optional for investors. It directly affects your net return on every asset you sell.

The tax applies only when a gain is realized, meaning you actually sell the asset. An investment that doubles in value while you hold it generates no tax liability. The moment you sell, the clock starts on what you owe. That timing distinction gives investors real control over their tax outcomes.

What is capital gains tax and how is it calculated?

Capital gains are calculated by subtracting your adjusted basis from the amount you realize on the sale. The formula is straightforward: Amount Realized (sale price minus selling expenses) minus Adjusted Basis equals Capital Gain.

The adjusted basis is typically what you paid for the asset, plus any improvements or additions, minus any depreciation you claimed. For example, if you bought stock for $10,000 and sold it for $15,000 after paying $200 in commissions, your capital gain is $4,800. Getting this number right matters because brokerage-reported basis does not always reflect your true adjusted basis, which can lead to overpaying or underreporting.

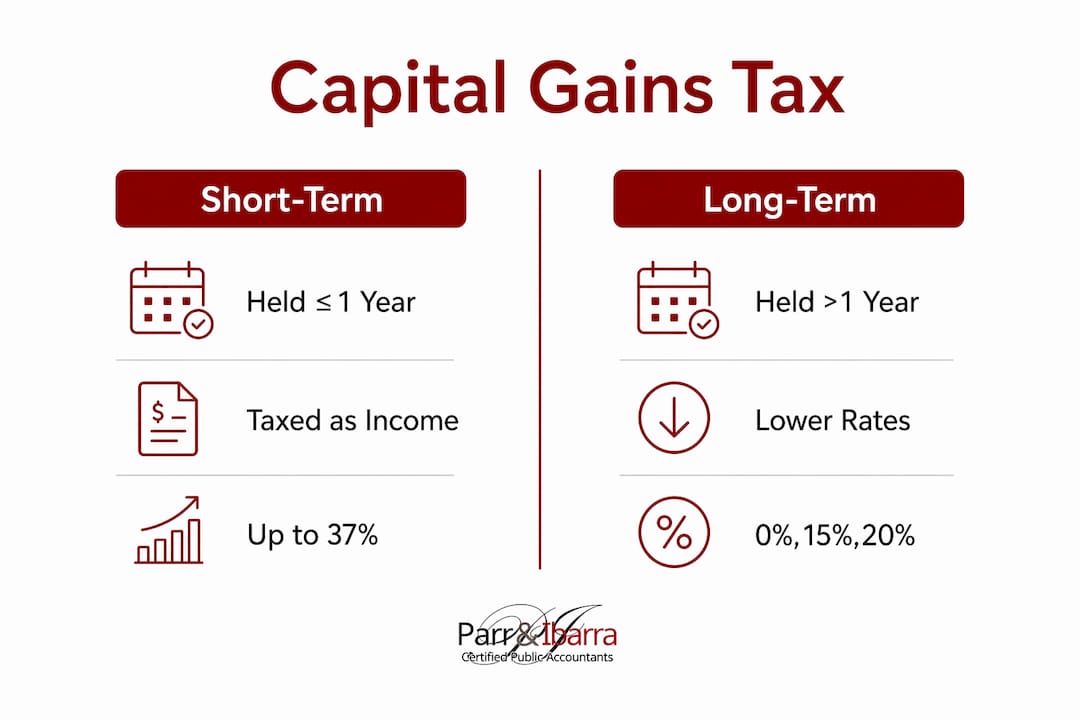

Short-term vs. long-term capital gains

The holding period determines which tax rate applies. The dividing line is exactly one year.

- Short-term gains: Assets held one year or less. Taxed at ordinary income rates, up to 37%.

- Long-term gains: Assets held more than one year. Taxed at preferential rates of 0%, 15%, or 20%.

- Holding period start date: The day after you acquire the asset, through and including the date you sell it.

- Mixed portfolios: Each position is evaluated individually, so you can have both short-term and long-term gains in the same tax year.

The difference between short-term and long-term treatment can be dramatic. Selling a stock after 11 months versus 13 months could mean paying 37 cents on the dollar versus 15 cents, on the same profit.

Pro Tip: If you are close to the one-year mark on a profitable position, wait until you cross it before selling. That single decision can cut your tax rate nearly in half.

What are the current capital gains tax rates?

Short-term capital gains are taxed as ordinary income, using the same brackets as your wages. The top federal rate is 37%. Long-term capital gains rates are lower and depend on your total taxable income and filing status.

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $47,025 | $47,026–$518,900 | Over $518,900 |

| Married Filing Jointly | Up to $94,050 | $94,051–$583,750 | Over $583,750 |

| Head of Household | Up to $63,000 | $63,001–$551,350 | Over $551,350 |

Note: Income thresholds reflect recent IRS guidance and are subject to annual inflation adjustments.

These brackets stack on top of your other income. If your wages push your total taxable income into a higher bracket, your capital gains rate rises with it. Capital gains tax brackets are not isolated from the rest of your return. That is why integrated income planning matters.

The Net Investment Income Tax (NIIT)

High earners face an additional layer. The NIIT adds 3.8% on top of federal capital gains tax for individuals with Modified Adjusted Gross Income (MAGI) above $200,000 (single filers) or $250,000 (married filing jointly). That means a high-income investor in the top bracket could pay an effective federal rate of 23.8% on long-term gains. Managing your MAGI through deductions, retirement contributions, or income timing can keep you below that threshold and save thousands.

What triggers capital gains tax and how do you report it?

Capital gains tax is triggered when you sell or otherwise dispose of an asset. Unrealized gains are not taxed until you actually realize them through a sale or disposition. Several events count as realization beyond a straightforward sale.

Common triggers include:

- Selling stocks, bonds, or real estate at a profit.

- Receiving capital gain distributions from mutual funds, even if you reinvest them automatically.

- Exchanging one asset for another, such as trading cryptocurrency for a different coin.

- Gifting appreciated property in certain circumstances, where the recipient inherits your basis.

Once a triggering event occurs, you report it on your federal return for that tax year. Form 8949 and Schedule D are the primary forms used to report capital gains and losses. Form 8949 lists each individual transaction. Schedule D summarizes the totals and feeds into your Form 1040. Missing a mutual fund distribution is one of the most common errors investors make, since those distributions appear on your 1099-DIV and are taxable even if you never touched the cash.

Pro Tip: Check your essential tax deadlines early in the year. Capital gains from the prior year must be reported by the April filing deadline, and estimated taxes on large gains may be due quarterly.

What exceptions and special rules affect capital gains tax?

Several rules reduce or eliminate capital gains tax liability in specific situations. Knowing them can save you a significant amount.

Primary residence exclusion

Eligible homeowners can exclude up to $250,000 of capital gain on the sale of a primary residence, or $500,000 for married couples filing jointly. To qualify, you must have owned and lived in the home for at least two of the five years before the sale. This exclusion does not apply to investment properties or vacation homes. For real estate tax strategies beyond the primary residence, the rules get more complex quickly.

Other special rate assets

Not all assets qualify for standard long-term rates. Collectibles such as art, coins, and comic books are taxed at a maximum federal rate of 28%. Real estate investors who claimed depreciation deductions face a separate “unrecaptured Section 1250 gain” taxed at up to 25%. These higher rates catch many investors off guard, especially those who have held collectibles for years assuming they would benefit from the standard 20% cap.

Capital loss rules

- Capital losses offset capital gains dollar for dollar in the same tax year.

- If losses exceed gains, up to $3,000 can be deducted against ordinary income.

- Losses beyond $3,000 carry forward indefinitely to future tax years.

- This carryforward is a powerful long-term tax management tool for active investors.

Pro Tip: Tax-loss harvesting, selling losing positions before year-end to offset gains, works best when you plan it in October or November rather than scrambling in late December.

Key Takeaways

Capital gains tax is a timing-driven tax where holding period, income level, and asset type together determine how much you owe on every profitable sale.

| Point | Details |

|---|---|

| Calculation starts with basis | Subtract your adjusted basis and selling expenses from sale proceeds to find your taxable gain. |

| Holding period is the key rate driver | Assets held more than one year qualify for 0%, 15%, or 20% rates instead of up to 37%. |

| NIIT adds 3.8% for high earners | Single filers above $200,000 MAGI and joint filers above $250,000 MAGI owe this surtax. |

| Primary residence exclusion is significant | Qualifying homeowners exclude up to $500,000 of gain from a primary home sale. |

| Losses carry forward indefinitely | Capital losses above the $3,000 annual deduction limit roll forward to reduce future gains. |

Why timing your sales is the most underused tax tool

Most investors focus on what to buy. The bigger tax decision is when to sell. I have seen clients pay tens of thousands more than necessary simply because they sold a position 30 days too early, missing the long-term threshold entirely. That is not a tax code problem. It is a planning problem.

The other mistake I see constantly is ignoring the adjusted basis. Investors assume their brokerage statement has the right number. It often does not, especially for positions held across multiple accounts, inherited assets, or stocks with reinvested dividends. Your actual basis can be higher than reported, which means you may be overpaying tax on gains that do not legally exist.

The NIIT is the third area where planning pays off. Investors who understand how MAGI works can time income events, accelerate deductions, or use retirement contributions to stay below the $200,000 or $250,000 threshold. A single year of proactive planning around MAGI can save more than years of passive investing. Capital gains planning is not a year-end task. It belongs in every quarterly financial review.

— Adan

Capital gains tax planning with Parr & Ibarra CPA

Capital gains tax decisions rarely happen in isolation. A stock sale, a real estate transaction, or a business exit all carry tax consequences that ripple through your entire return. Getting the numbers right requires more than a tax form.

Parr & Ibarra CPA works with individuals and investors across the Dallas-Fort Worth area to build proactive tax strategies around capital gains, NIIT exposure, and asset timing. Whether you are selling investment property, managing a portfolio, or planning around a major liquidity event, the team at Parr & Ibarra CPA provides hands-on guidance year-round. Start with the IRS Tax Filing Guide 2026 for a clear overview of current filing requirements and capital gains reporting. For complex transactions, professional CPA services are available to help you plan before you sell, not after.

FAQ

What is capital gains tax in simple terms?

Capital gains tax is the federal tax on profit from selling an asset for more than you paid. It applies to stocks, real estate, and other investments when the gain is realized through a sale.

How is capital gains tax calculated?

Subtract your adjusted basis and any selling expenses from your sale price. The result is your taxable capital gain, reported on Form 8949 and Schedule D.

What is the difference between short-term and long-term capital gains?

Short-term gains apply to assets held one year or less and are taxed at ordinary income rates up to 37%. Long-term gains on assets held more than one year are taxed at 0%, 15%, or 20%.

Do I owe capital gains tax when I sell my home?

Qualifying homeowners can exclude up to $250,000 of gain ($500,000 married filing jointly) if they owned and lived in the home for at least two of the five years before the sale.

What triggers capital gains tax on investments?

Selling a stock or bond, receiving mutual fund capital gain distributions, or exchanging one asset for another all trigger capital gains tax in the year the transaction occurs.