Retirement plans tax savings occur through three distinct mechanisms: immediate tax deductions, tax-deferred growth, or tax-free withdrawals, depending on which account you use. For anyone approaching retirement in 2026, the difference between a well-structured plan and a poorly timed one can mean tens of thousands of dollars in unnecessary taxes. The IRS has updated contribution limits for 401(k)s, IRAs, Solo 401(k)s, and SIMPLE plans this year, giving you more room to reduce your taxable income than ever before. Understanding how each account type works, and when to draw from each, is the foundation of a sound retirement tax strategy.

How retirement plans impact your taxable income

The tax treatment of your retirement account determines when you pay taxes, not whether you pay them. That distinction shapes every decision you make from now through retirement.

Traditional 401(k)s and IRAs reduce your taxable income in the year you contribute. Every dollar you put in comes out of your gross income before the IRS calculates what you owe. The trade-off is that distributions are taxed as ordinary income at federal rates ranging from 10% to 37% in 2026. That means a retiree pulling $80,000 per year from a traditional IRA could owe taxes at the 22% bracket on a significant portion of those withdrawals.

Roth IRAs and Roth 401(k)s flip the equation. You contribute after-tax dollars today, so there is no immediate deduction. The payoff comes later. Qualified Roth withdrawals are tax-free after a five-year holding period and once you reach age 59½. For someone who expects to be in a higher tax bracket in retirement, Roth accounts are the stronger long-term tool.

Taxable brokerage accounts offer no upfront deduction and no tax-free growth. However, investments held longer than one year qualify for long-term capital gains rates of 0%, 15%, or 20%, which are significantly lower than ordinary income rates for most retirees. These accounts play a supporting role in a tax-efficient income strategy.

The choice between pre-tax and Roth contributions depends heavily on your expected tax bracket in retirement. If you are in a high bracket now and expect a lower one later, pre-tax contributions win. If the reverse is true, Roth wins.

Pro Tip: If you are unsure which bracket you will land in during retirement, split your contributions between a traditional and Roth account. This hedges your tax exposure across both scenarios.

What are the 2026 contribution limits for retirement plans?

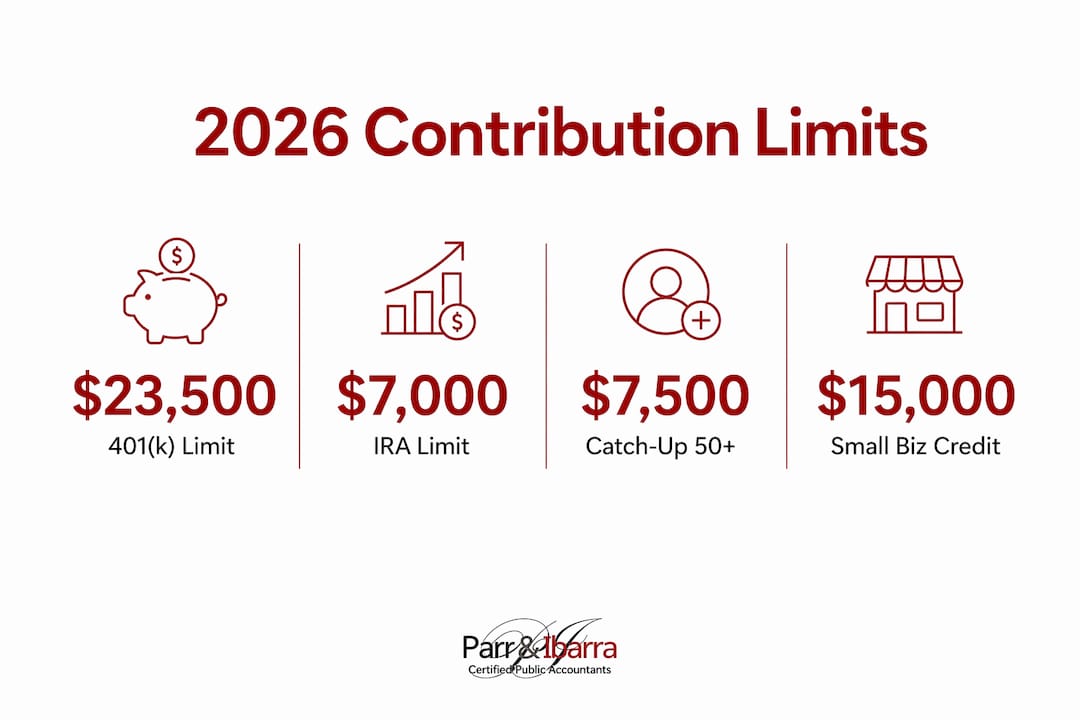

The IRS raised contribution limits for 2026, and using every dollar available to you is one of the most direct ways to cut your tax bill.

For a standard 401(k), the elective deferral limit is $23,500, with an additional $7,500 catch-up contribution allowed if you are age 50 or older. That brings your total to $31,000 per year in pre-tax or Roth contributions. For self-employed individuals using a Solo 401(k), the combined employer and employee contribution limit reaches $69,000, or $76,500 for those 50 and older. A $50,000 contribution in the 32% tax bracket saves $16,000 in federal income tax in that year alone, before accounting for state taxes.

IRA contributions remain at $7,000 for 2026, with a $1,000 catch-up for those 50 and older. Traditional IRA contributions may be fully deductible depending on your income and whether you have a workplace plan.

For small business owners, SEP-IRAs allow contributions up to 25% of net self-employment income, and SIMPLE IRAs allow employee deferrals up to $16,000 in 2026. Both plans carry lower administrative costs than a 401(k) and still deliver meaningful tax deductions.

Under SECURE 2.0, small businesses with 50 or fewer employees can claim tax credits for retirement plan startup costs up to $15,000 over three years, plus an additional credit of up to $1,000 per employee per year for five years for employer contributions. These credits directly reduce your business tax bill, not just your taxable income.

| Plan Type | 2026 Employee Limit | Catch-Up (50+) | Employer Contributions |

|---|---|---|---|

| 401(k) | $23,500 | $7,500 | Up to plan limits |

| Solo 401(k) | $23,500 | $7,500 | Up to $69,000 combined |

| Traditional IRA | $7,000 | $1,000 | None |

| SEP-IRA | N/A | None | Up to 25% of net income |

| SIMPLE IRA | $16,000 | $3,500 | Required match or nonelective |

Pro Tip: If you run a small business and have not set up a retirement plan yet, the SECURE 2.0 tax credits make 2026 the most cost-effective year to start. Visit the SEP-IRA guide for S Corporations to see which structure fits your business.

How should you sequence withdrawals to minimize retirement taxes?

Retirement tax planning centers on managing brackets and withdrawal order, not on picking a single best account. The sequence in which you draw income determines how much of it the IRS takes.

The standard tax-efficient withdrawal order works like this:

- Taxable brokerage accounts first (in early retirement, before required minimum distributions kick in). Long-term gains taxed at 0% if your income stays below $47,025 for single filers in 2026.

- Traditional IRA and 401(k) withdrawals in controlled amounts to fill lower tax brackets without pushing into higher ones.

- Roth accounts last, since they carry no required minimum distributions and grow tax-free indefinitely.

“The goal is not to avoid taxes entirely. The goal is to pay them at the lowest possible rate, in the year that costs you the least.” This means filling the 12% bracket with traditional IRA withdrawals before touching Roth funds, rather than drawing everything from one source.

Social Security taxation adds another layer of complexity. Up to 85% of your Social Security benefit becomes taxable once your provisional income (adjusted gross income plus half your Social Security benefit plus tax-exempt interest) exceeds $34,000 for single filers or $44,000 for married couples. Keeping traditional IRA withdrawals low in early retirement can preserve more of your Social Security benefit from taxation.

Coordinating Roth, taxable, and traditional accounts into a layered income strategy lets you satisfy spending needs while staying in the lowest possible bracket each year. This is not a set-it-and-forget-it plan. It requires annual review as your income, tax laws, and account balances shift.

What pitfalls should you avoid with retirement tax strategies?

The most expensive retirement tax mistakes are not obvious. They hide inside strategies that look smart on the surface.

The pro-rata rule in backdoor Roth conversions. High earners who exceed the Roth IRA income limits often use a backdoor Roth conversion. The problem arises when you hold pre-tax IRA assets. The IRS aggregates all traditional IRA balances when calculating the taxable portion of a conversion, which can trigger a large unexpected tax bill. Rolling pre-tax IRA funds into your employer’s 401(k) before converting solves this.

Ignoring the Net Investment Income Tax (NIIT). High net worth individuals with modified adjusted gross income above $200,000 (single) or $250,000 (married) owe an additional 3.8% tax on investment income. Coordinating withdrawals to stay below these thresholds is a real strategy, not a theoretical one.

Missing contribution deadlines. Traditional IRA contributions for 2026 can be made up until the tax filing deadline in april 2027. SEP-IRA contributions can be made even later, up to the extended filing deadline. Missing these windows means leaving a deduction on the table.

Treating an HSA as a short-term spending account. A Health Savings Account used as a long-term investment vehicle is one of the most tax-efficient tools available. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, you can withdraw for any purpose and pay only ordinary income tax, making it function like a traditional IRA.

Pro Tip: If you have multiple IRA accounts scattered across different institutions, consolidate them before attempting a Roth conversion. Fewer accounts mean cleaner math and fewer pro-rata surprises. The 2026 IRS tax guide from Parr & Ibarra CPA covers the filing rules you need to know.

Key takeaways

The most effective retirement tax strategy combines pre-tax deductions, Roth growth, and a disciplined withdrawal sequence to keep your lifetime tax bill as low as possible.

| Point | Details |

|---|---|

| Use every contribution dollar | Max out 401(k) and IRA limits in 2026 to reduce taxable income immediately. |

| Match account type to tax bracket | Pre-tax accounts favor high earners now; Roth accounts favor those expecting higher future taxes. |

| Sequence withdrawals strategically | Draw from taxable accounts first, then traditional accounts, then Roth to stay in lower brackets. |

| Watch Social Security thresholds | Keep provisional income below $34,000 (single) or $44,000 (married) to limit Social Security taxation. |

| Small business owners have extra tools | SECURE 2.0 credits cover up to $15,000 in startup costs and $1,000 per employee per year in contribution credits. |

The retirement tax mistake i see most often

After working with hundreds of clients at Parr & Ibarra CPA, the pattern I see most often is not reckless spending or bad investments. It is a complete lack of coordination between account types.

People spend decades building a 401(k) and nothing else. Then they retire, start pulling from that single account, and discover that every dollar is taxed as ordinary income at rates they never anticipated. They had the discipline to save. They just never had a plan for how to spend it efficiently.

The fix is not complicated, but it requires starting earlier than most people think. I tell clients in their mid-50s to start building a Roth balance alongside their traditional accounts, even if the contributions are smaller. The goal is to have options at retirement, not obligations. When you only have one type of account, you have no flexibility to manage your bracket.

I also push back on the idea that Roth conversions are only for young people. A targeted conversion in your early 60s, before Social Security begins and before required minimum distributions force income on you, can permanently reduce your future tax exposure. The math often works in your favor even if you pay a modest tax bill today.

The clients who retire with the most financial clarity are the ones who treated tax planning as a year-round discipline, not a once-a-year filing exercise. Working with a CPA who understands both the tax code and your personal situation is not a luxury. For anyone with meaningful retirement assets, it is the highest-return investment you can make.

— Adan

How parr & ibarra CPA can help you keep more in retirement

Retirement tax planning is not a one-time conversation. It requires ongoing adjustments as tax laws change, account balances grow, and your income needs shift.

Parr & Ibarra CPA works with individuals approaching retirement across the Dallas-Fort Worth area to build personalized tax strategies that go beyond annual filing. The team helps you identify the right contribution mix for 2026, evaluate Roth conversion opportunities, and structure withdrawals to minimize your lifetime tax exposure. Whether you need help with retirement deduction strategies or a full mid-year tax review, Parr & Ibarra CPA brings the depth of a large firm with the attention of a local partner. Schedule a strategy session today and put your retirement savings to work more efficiently.

FAQ

What is the 401(k) contribution limit in 2026?

The 2026 401(k) elective deferral limit is $23,500, with a $7,500 catch-up contribution for those age 50 and older, bringing the total to $31,000. Solo 401(k) plans allow combined contributions up to $69,000, or $76,500 with the catch-up.

How do roth IRA withdrawals differ from traditional IRA withdrawals?

Roth IRA qualified withdrawals are completely tax-free after a five-year holding period and age 59½, while traditional IRA withdrawals are taxed as ordinary income at rates from 10% to 37% in 2026.

What is the pro-rata rule and why does it matter?

The pro-rata rule requires the IRS to treat all your traditional IRA assets as a single pool when calculating taxes on a Roth conversion. If you have pre-tax IRA funds, rolling them into a 401(k) first lets you convert after-tax funds cleanly without an unexpected tax bill.

Can small business owners get tax credits for starting a retirement plan?

Yes. Under SECURE 2.0, businesses with 50 or fewer employees can claim up to $15,000 in tax credits over three years for plan startup costs, plus up to $1,000 per employee per year for five years for employer contributions made to the plan.

When is the best time to start a roth conversion strategy?

The best window for Roth conversions is typically in your early 60s, after you stop working but before Social Security begins and before required minimum distributions force taxable income on you. Converting during this low-income window often produces the lowest possible tax cost on the conversion.