Choosing the right business entity is the single most consequential tax decision a Dallas-Fort Worth entrepreneur makes. Your entity structure determines how much self-employment tax you pay, whether you qualify for the 20% QBI deduction under IRC §199A, and how much of your profit you actually keep. A sole proprietor and an S-Corp owner earning the same $150,000 in net profit can face a difference of more than $11,000 in annual taxes. When you choose business entity tax savings correctly, that gap goes straight back into your business. Parr & Ibarra CPA works with Dallas-Fort Worth business owners every day to make exactly this call.

How different business entities impact your tax burden

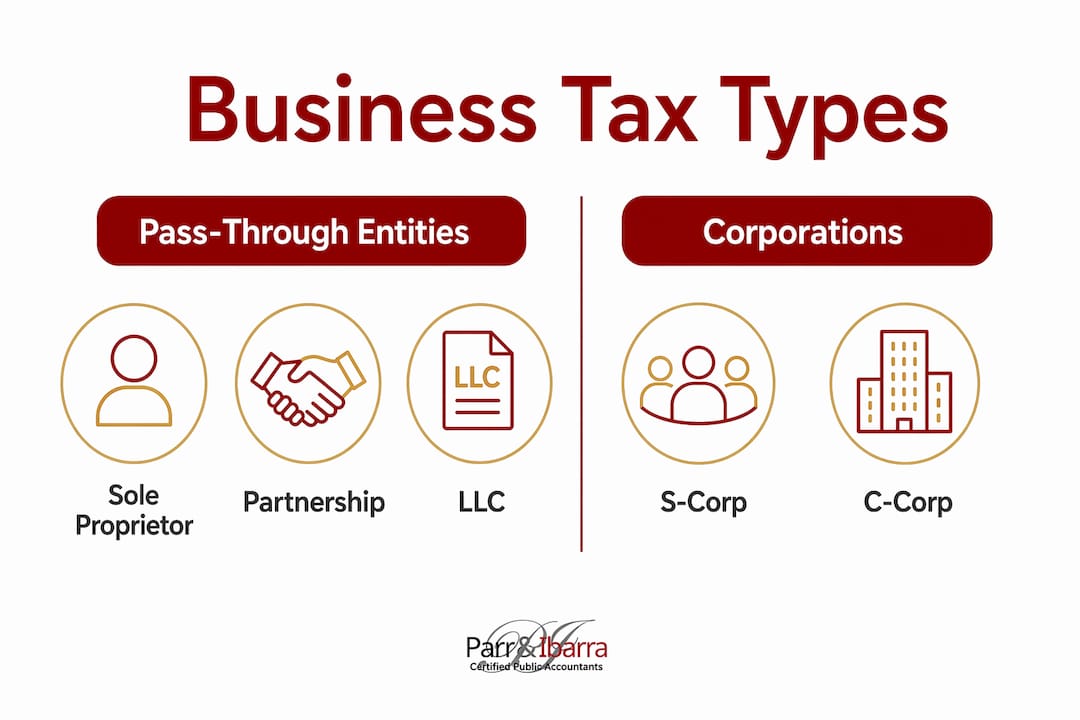

The entity you choose determines your tax classification, not just your legal structure. That distinction matters because the IRS taxes different structures in fundamentally different ways.

Sole proprietorships and default LLCs

A default single-member LLC pays taxes exactly like a sole proprietor. SE tax hits 15.3% on roughly 92.35% of your net profit, plus an additional 0.9% Medicare surtax above certain income thresholds. That means forming an LLC by itself does not lower your tax bill. The liability protection is real, but the tax benefit requires an additional election.

Partnerships and multi-member LLCs

Multi-member LLCs default to partnership taxation. Each partner reports their share of income on a Schedule K-1 and pays self-employment tax on their distributive share. The same 15.3% SE tax applies to active partners, making the default partnership structure one of the higher-tax options for profitable businesses.

S-Corporations

An S-Corp election changes the math significantly. The owner pays a reasonable salary, which is subject to payroll taxes, but takes additional profit as distributions that are not subject to self-employment tax. On a $150,000 net profit with a $70,000 salary, the annual SE tax savings reach approximately $11,000 after accounting for payroll and filing costs. That is the most common reason Dallas-Fort Worth business owners elect S-Corp status.

C-Corporations

C-Corps pay a flat 21% federal tax at the entity level, and shareholders pay tax again on dividends at 15–20%. That double taxation makes C-Corps a poor fit for most small profitable businesses. The exception is high earners seeking Qualified Small Business Stock (QSBS) benefits or businesses planning to retain large earnings for reinvestment rather than distribute them.

Texas adds one more layer. Texas imposes no state income tax, which shifts the focus almost entirely to federal planning. Franchise taxes and local regulations still apply, but the absence of a state income tax makes federal entity strategy even more impactful for DFW business owners.

| Entity type | Self-employment tax | Pass-through income | Double taxation |

|---|---|---|---|

| Sole proprietor / default LLC | 15.3% on net profit | Yes | No |

| S-Corp elected LLC | Only on salary portion | Yes | No |

| Partnership / multi-member LLC | 15.3% on active share | Yes | No |

| C-Corporation | None at owner level | No | Yes (21% + dividend tax) |

What is the QBI deduction and who qualifies?

The 20% QBI deduction under IRC §199A permanently reduces taxable income for eligible pass-through entities as of 2026. That means sole proprietors, partnerships, S-Corps, and single-member LLCs can all deduct up to 20% of their qualified business income before calculating their federal income tax.

Here is what qualifies and what limits the deduction:

- Eligible entities: Sole proprietorships, partnerships, S-Corps, and LLCs taxed as any of the above

- Income thresholds: Phase-outs begin at higher income levels for specified service trades or businesses (SSTBs), including law, consulting, and financial services

- W-2 wage limits: At higher income levels, the deduction is limited by the W-2 wages paid by the business or the unadjusted basis of qualified property

- Non-SSTBs: Businesses like retail, construction, and manufacturing face fewer restrictions and can often claim the full 20%

The interaction between S-Corp salary and the QBI deduction is where planning gets critical. A lower salary increases distributions and reduces payroll taxes, but it also reduces W-2 wages, which can limit the QBI deduction at higher income levels. Getting the salary-to-distribution ratio right requires running actual projections, not guessing.

Pro Tip: If your business qualifies for the full QBI deduction, combining it with an S-Corp election creates a two-layer tax reduction. You cut SE tax through the salary-distribution split and cut income tax through the 20% QBI deduction simultaneously.

When does an S-Corp election actually make sense?

The S-Corp election is not right for every business. The break-even point sits around $75,000 in annual net profit. Below that level, payroll and tax prep costs of $3,500–$5,000 per year can wipe out the SE tax savings entirely.

Here is the process and what to expect:

- File Form 2553 with the IRS to elect S-Corp status. The deadline is March 15 for the election to apply to the current tax year, or within 75 days of forming your entity.

- Set a reasonable salary. The IRS requires that owner-employees receive compensation comparable to what the market pays for their role. Reasonable salary is assessed using industry compensation data, the owner’s specific duties, and time spent in the business.

- Run payroll. You must process payroll for yourself, withhold federal and state payroll taxes, and file quarterly payroll returns. This is where the $3,500–$5,000 annual compliance cost comes from.

- Take distributions. Profit above your salary is distributed to you as an owner distribution, which is not subject to self-employment tax.

- File Form 1120-S annually. The S-Corp files its own informational return, and you receive a Schedule K-1 to report on your personal return.

Pro Tip: S-Corp election is revocable, but timing restrictions apply. Consult a CPA before electing or revoking. A poorly timed revocation can lock you out of re-electing for five years.

The table below shows how the numbers work at different profit levels for a Dallas-Fort Worth business owner with a $70,000 reasonable salary:

| Net profit | SE tax (default LLC) | SE tax (S-Corp) | Estimated annual savings |

|---|---|---|---|

| $75,000 | ~$10,600 | ~$7,100 | ~$3,500 (near break-even) |

| $100,000 | ~$14,100 | ~$7,100 | ~$7,000 |

| $150,000 | ~$21,200 | ~$7,100 | ~$11,000+ |

Numbers are approximate and do not include compliance costs of $3,500–$5,000 per year.

Practical steps to pick the best business structure for tax savings

Choosing the right structure is a decision that combines your current profit, your growth plans, your risk exposure, and your tolerance for administrative work. Follow these steps to make the call clearly.

- Calculate your current net profit. If you clear less than $60,000 annually, a default LLC or sole proprietorship is likely your lowest-cost option. The SE tax burden is real, but S-Corp compliance costs will exceed your savings.

- Project your next two to three years. If you expect to cross $75,000–$100,000 in net profit, plan the S-Corp election before you hit that threshold. Retroactive elections are possible but limited.

- Assess your liability exposure. Any business with employees, client contracts, or physical assets needs the liability protection of an LLC or corporation regardless of the tax outcome.

- Compare total tax burden, not just entity tax. Factor in the QBI deduction, retirement plan contributions, and deductible business expenses. Retirement contributions like a Solo 401(k) can shelter significant income and often produce larger savings than entity choice alone.

- Get a tax projection from a CPA. A side-by-side projection comparing your current structure against an S-Corp election, with actual numbers from your business, is the only reliable way to make this decision.

Key factors to weigh before making any entity change:

- Current and projected annual net profit

- Cost of payroll services and additional tax filings

- Eligibility for the QBI deduction under your income level

- Whether your business qualifies as an SSTB under IRC §199A

- Your plans to bring on partners, investors, or employees

Parr & Ibarra CPA provides these projections as part of proactive tax planning for Dallas-Fort Worth business owners, so you see the real numbers before committing to any structural change.

Key Takeaways

The most effective approach to business entity tax savings combines the right entity election, the QBI deduction, and retirement contributions into a single coordinated plan.

| Point | Details |

|---|---|

| Default LLC does not cut SE tax | Forming an LLC alone provides no tax reduction; S-Corp election is required to lower self-employment tax. |

| S-Corp election breaks even near $75K | Payroll and filing costs of $3,500–$5,000 per year make S-Corp elections worthwhile only above ~$75,000 net profit. |

| QBI deduction stacks with S-Corp | Eligible pass-through owners can claim a 20% QBI deduction on top of S-Corp SE tax savings for a two-layer reduction. |

| Texas has no state income tax | DFW business owners focus entirely on federal planning, making entity and QBI strategy even more impactful. |

| Reasonable salary is non-negotiable | The IRS audits S-Corp owners who pay below-market salaries; setting it correctly protects your savings and your filing. |

What I’ve learned from watching business owners get this wrong

Most of the entity-selection mistakes I see come from treating the decision as a one-time checkbox rather than an ongoing calculation. A business owner forms an LLC, hears that S-Corps save on taxes, and files Form 2553 without running the numbers. Then they spend $4,500 a year on payroll services to save $3,200 in SE tax. That is not a win.

The other pattern I see constantly is over-focusing on entity choice while ignoring retirement contributions. A well-funded Solo 401(k) or defined benefit plan can shelter far more income than the SE tax savings from an S-Corp election. The best outcomes come from combining both: elect S-Corp status when the math supports it, then layer in retirement contributions and the QBI deduction on top.

I also want to be direct about reasonable salary. I have seen business owners set their S-Corp salary at $25,000 on $200,000 in profit because someone told them to “keep it low.” That is an audit waiting to happen. The IRS has clear guidance on what constitutes reasonable compensation, and underpaying yourself is not a gray area. Set the salary correctly, document your reasoning, and the savings are real and defensible.

The entity decision is not the finish line. It is the starting point for a broader tax plan that includes retirement plan contributions, QBI optimization, and quarterly estimated tax management. Get all three working together and the savings compound year over year.

— Adan

How Parr & Ibarra CPA helps DFW business owners keep more profit

Parr & Ibarra CPA works with Dallas-Fort Worth entrepreneurs who want a real tax plan, not just a filed return. The team runs side-by-side entity projections, handles S-Corp election filings, and sets up payroll so the compliance side does not eat your savings.

With over 20 professionals including multiple CPAs, Parr & Ibarra CPA covers every layer of the tax picture: entity structure, QBI deduction planning, retirement contributions, and quarterly estimated taxes. If you are earning above $75,000 in net profit and still filing as a default LLC, you are likely leaving thousands on the table each year. The team at Parr & Ibarra CPA can show you exactly how much with a personalized tax planning consultation built around your 2026 numbers.

FAQ

What is the best business structure for tax savings?

The best structure depends on your net profit level. For owners earning above $75,000 annually, an LLC with an S-Corp election typically produces the most federal tax savings by reducing self-employment tax on distributions.

Does forming an LLC reduce my taxes?

A default LLC does not reduce self-employment tax. Default single-member LLCs pay 15.3% SE tax on net profit, the same as a sole proprietor. Tax savings require an S-Corp election on top of the LLC structure.

What is the QBI deduction and do I qualify?

The QBI deduction allows eligible pass-through business owners to deduct up to 20% of qualified business income from their taxable income. Most sole proprietors, LLC owners, and S-Corp owners qualify, though income phase-outs apply to certain service businesses.

When should I elect S-Corp status for my LLC?

Elect S-Corp status when your annual net profit consistently exceeds $75,000. Below that threshold, payroll and filing costs of $3,500–$5,000 per year typically offset the self-employment tax savings.

Does Texas have a state income tax that affects my entity choice?

Texas has no personal state income tax, which means Dallas-Fort Worth business owners focus their entity planning entirely on federal taxes. Local franchise taxes still apply, but the absence of state income tax makes federal entity strategy the primary driver of overall tax savings.