Nobody enjoys opening a letter from the IRS. But for most Texas business owners, the dread that comes with those three letters is not really about guilt. It is about uncertainty. Did we document everything correctly? Did we miss something? Would our financials actually hold up if someone looked closely?

Here is the reality: businesses that work with experienced CPAs on audit and assurance services rarely panic when scrutiny arrives. That is because they have already done the hard work. Their books are clean, their records are organized, and their financial statements reflect what actually happened, not what was convenient to report.

In 2026, the stakes are higher than they have been in years. The IRS has expanded its digital compliance infrastructure, increased enforcement targeting pass-through entities and high-income earners, and deployed algorithmic screening tools that flag returns falling outside expected patterns faster than any human reviewer could. If your business financials would not hold up to scrutiny today, that gap is worth closing, and closing soon.

This guide walks Texas business owners, Dallas entrepreneurs, and investors through everything that matters about audit and assurance services: what they are, why they matter this year specifically, how to prepare, and when to bring in a CPA who knows the terrain.

Audit and Assurance: What the Terms Actually Mean

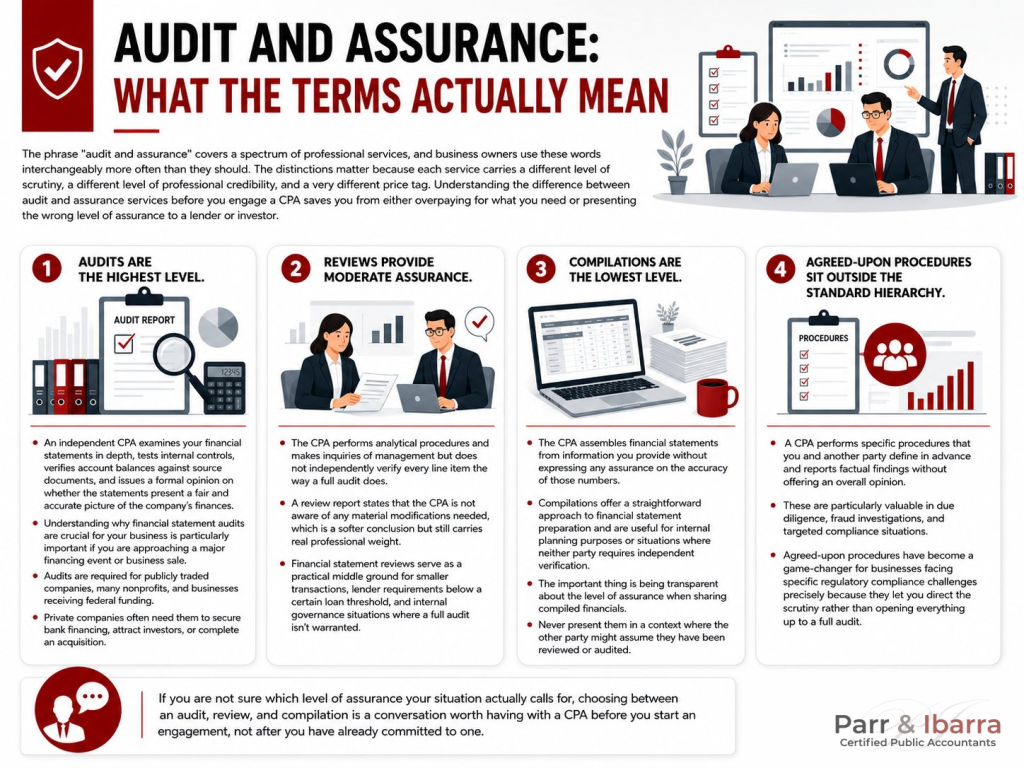

The phrase “audit and assurance” covers a spectrum of professional services, and business owners use these words interchangeably more often than they should. The distinctions matter because each service carries a different level of scrutiny, a different level of professional credibility, and a very different price tag. Understanding the difference between audit and assurance services before you engage a CPA saves you from either overpaying for what you need or presenting the wrong level of assurance to a lender or investor.

Audits are the highest level. An independent CPA examines your financial statements in depth, tests internal controls, verifies account balances against source documents, and issues a formal opinion on whether the statements present a fair and accurate picture of the company’s finances. Understanding why financial statement audits are crucial for your business is particularly important if you are approaching a major financing event or business sale. Audits are required for publicly traded companies, many nonprofits, and businesses receiving federal funding. Private companies often need them to secure bank financing, attract investors, or complete an acquisition.

Reviews provide moderate assurance. The CPA performs analytical procedures and makes inquiries of management but does not independently verify every line item the way a full audit does. A review report states that the CPA is not aware of any material modifications needed, which is a softer conclusion but still carries real professional weight. Financial statement reviews serve as a practical middle ground for smaller transactions, lender requirements below a certain loan threshold, and internal governance situations where a full audit isn’t warranted.

Compilations are the lowest level. The CPA assembles financial statements from information you provide without expressing any assurance on the accuracy of those numbers. Compilations offer a straightforward approach to financial statement preparation and are useful for internal planning purposes or situations where neither party requires independent verification. The important thing is being transparent about the level of assurance when sharing compiled financials. Never present them in a context where the other party might assume they have been reviewed or audited.

Agreed-Upon Procedures sit outside the standard hierarchy. A CPA performs specific procedures that you and another party define in advance and reports factual findings without offering an overall opinion. These are particularly valuable in due diligence, fraud investigations, and targeted compliance situations. Agreed-upon procedures have become a game-changer for businesses facing specific regulatory compliance challenges precisely because they let you direct the scrutiny rather than opening everything up to a full audit.

If you are not sure which level of assurance your situation actually calls for, choosing between an audit, review, and compilation is a conversation worth having with a CPA before you start an engagement, not after you have already committed to one.

Why 2026 Makes This Conversation More Urgent

Several things converging at once in 2026 make financial credibility and audit preparedness more consequential than they have been in recent years.

The IRS Is Watching More Efficiently

The IRS has significantly expanded its digital compliance infrastructure. Automated matching programs now cross-reference income reported on 1099s, K-1s, and W-2s against what appears on business and individual returns more efficiently than ever before. Pass-through entities, S-Corps, and businesses with large deductions relative to reported income are receiving more attention. Understanding what an IRS audit actually involves is useful context regardless of whether you expect to face one, because the preparation that prevents an audit and the preparation that helps you survive one are largely the same.

For a Dallas business owner who took substantial bonus depreciation deductions in 2026, which is entirely legal and actively encouraged, having clean underlying records to support those deductions is not optional. It is the cost of the strategy. With IRS audit risks shifting in ways that affect businesses at every revenue level, the value of year-round professional support has gone up considerably.

Lenders and Capital Markets Want Documentation

Tightening credit conditions have made lenders more conservative. If your Dallas business is seeking a commercial real estate loan, a line of credit above $2 million, or SBA financing, most lenders will require reviewed or audited financials. Businesses that have maintained clean books and worked with a CPA throughout the year move through underwriting faster and with fewer surprises.

Private equity groups and strategic buyers looking at Texas businesses conduct financial due diligence carefully. If your records are inconsistent or your revenue recognition doesn’t follow standard accounting principles, a deal can fall apart during due diligence, or you may leave significant value on the table in negotiations. Knowing how taxes and financial structure affect a merger or acquisition before you are in that process changes what you do years before the transaction closes.

Business Growth Compounds Financial Complexity

A Dallas entrepreneur running a $400,000 business faces a different accounting environment than one managing a $4 million operation. As businesses grow, the risk of material misstatements in the financials increases. Transactions get more complex. Revenue streams multiply. Payroll grows. Vendor relationships expand. Regular assurance engagements, even when a full audit is not required, help business owners stay ahead of that complexity rather than discovering problems after they have become material issues.

Types of Assurance Engagements and When You Need Each

Financial Statement Audits

If your business falls into any of the following categories, a full audit is either required or strongly advisable. You receive federal grants or contracts above $750,000, which triggers the Single Audit requirement under Uniform Guidance. You operate as a nonprofit and your state or bylaws require audited financials. Your lender requires audited statements as a loan covenant. You are preparing to sell and the buyer demands audited financials for the acquisition. You have investors, shareholders, or a board that requires independent verification.

For most small and mid-size Texas businesses, audits are not an annual requirement, but they become necessary at key inflection points. Planning for those moments before they arrive saves time, money, and the specific kind of stress that comes from being on a deadline with disorganized books.

Reviews

A reviewed financial statement is the most common assurance level in small to mid-size business transactions in Texas. Many community banks and regional lenders require reviewed financials for commercial loans in the $500,000 to $3 million range. A review also adds credibility when entering a new partnership, negotiating a significant vendor contract, or presenting to prospective investors at an early stage. The cost is substantially lower than an audit, the timeline is shorter, and for most transactional purposes, the assurance it provides is sufficient.

Compilations

If you want professionally formatted financial statements for internal planning or to share with a business partner who is not requiring a formal engagement, a compilation serves that purpose. Know its limits, though. A compilation carries no assurance. If numbers are wrong, the CPA’s involvement does not indicate they were verified. Be explicit about the level of assurance when sharing compiled financials.

Agreed-Upon Procedures for Targeted Issues

For Texas businesses with 20 to 50 employees and a growing operations team, an annual agreed-upon procedures engagement focused on expense reporting, payroll accuracy, or vendor payments can serve as a meaningful fraud deterrent and a discovery tool for procedural errors. The cost is far lower than a full audit, and the findings are targeted to the areas that matter most to you. Knowing what audit protection actually means and why it matters is the framing that makes these engagements feel less like a compliance obligation and more like a business intelligence tool.

How to Prepare Your Business for an Audit in 2026

Preparation is where audits are won or lost. Businesses that scramble to assemble records after the engagement begins face delays, higher fees, and sometimes adverse findings that proper preparation would have avoided entirely.

Keep Clean, Current Books Throughout the Year

This sounds obvious, but the number of Texas businesses that arrive at an audit engagement with 18 months of unreconciled bank statements is genuinely surprising. Monthly bank reconciliations, consistent transaction coding, and timely recording of all entries are the foundation of audit readiness. Bookkeeping basics for small businesses outline the minimum systems every business should have in place, and maintaining those systems year-round is the single most effective thing you can do to reduce audit costs and complications.

A bookkeeping service that keeps your general ledger current is not just convenient. It is an audit infrastructure. If your books are six months behind when an engagement begins, you will pay for the cleanup in both time and professional fees.

Document Your Internal Controls

Auditors assess not just whether the numbers are right but whether the systems that produce those numbers are reliable. Internal controls include segregation of duties (the person writing checks is not the same person reconciling the bank account), approval workflows for expenses above a certain threshold, inventory counting procedures, and controls over access to accounting systems.

For a small Dallas business with a lean team, some of these controls will be less formal. They should still exist and be documented. Auditors want to understand how things work, not just see the outputs. How poor financial practices can put your LLC liability shield at risk covers the downstream consequences of weak financial systems in more detail, and many of those vulnerabilities show up clearly in an audit context.

Organize Your Supporting Documentation

Every significant number in your financial statements needs to trace back to a source document. Revenue ties to invoices and bank deposits. Expenses tie to receipts, vendor contracts, or purchase orders. Fixed asset additions require purchase records and depreciation schedules. Knowing what records you are required to keep and organizing them in a retrievable system throughout the year makes an audit engagement faster and less expensive for everyone involved.

In 2026, digital documentation is fully acceptable. Cloud-based receipt capture, digital invoice archives, and electronic bank statements all satisfy auditor requirements. What matters is that the documentation exists, is organized, and can be retrieved quickly on request.

Get Revenue Recognition Right Before the Engagement Starts

Revenue recognition errors are among the most common findings in audit and review engagements. When exactly is revenue recognized? If you are a service business billing monthly retainers, is income recognized when billed or when the service is delivered? If you take deposits for future services, when does that deferred revenue become earned?

Getting this right before an engagement begins prevents awkward adjustments and restatements. It also prevents the kind of corrected financials that raise questions with lenders or buyers who see the original version alongside the amended one.

Using Assurance Services Strategically, Not Just Defensively

Most business owners think of audits as something that happens to them. Sophisticated owners use assurance services as a competitive tool.

Use Reviews to Negotiate Better Financing Terms

Lenders price risk. A business presenting reviewed financials with consistent revenue trends, healthy margins, and clean supporting schedules is a lower-risk borrower than one presenting unreviewed accounting software exports. That difference in perceived risk can translate into a lower interest rate or more favorable loan terms.

A Dallas commercial real estate developer seeking a $2.5 million construction loan negotiated a better rate by presenting two years of reviewed financials that clearly demonstrated financial consistency. The cost of two years of review engagements was recovered many times over in interest savings on a single deal.

Prepare for a Business Sale Well in Advance

If you think you might sell in the next three to five years, start treating your financials as if a buyer’s CPA will scrutinize every line. That means consistent revenue recognition, clean expense categorization, no personal expenses running through the business, and ideally one to two years of reviewed or audited statements in place before you go to market. A guide to preparing for a financial statement audit is a useful framework for thinking about what that preparation actually involves. Businesses with clean reviewed financials command higher multiples in acquisitions. Buyers pay a premium for certainty, and audited or reviewed statements provide it in a way that unreviewed tax returns simply cannot. Knowing which exit strategy is right for your business is a related conversation, because the financial preparation that maximizes audit credibility and the preparation that maximizes exit value are largely the same work.

Use Agreed-Upon Procedures to Get Ahead of Fraud

Agreed-upon procedures engagements are significantly underused by small and mid-size Texas businesses. They allow you to direct a CPA to test specific areas of concern, whether that is payroll processing, vendor payments, expense reimbursements, or cash handling, without commissioning a full audit. For businesses with growing operations teams, this kind of targeted engagement serves as both a fraud deterrent and a procedural error discovery tool. What employers should watch for around 401(k) plan fraud is one example of a specific risk area where agreed-upon procedures can surface problems before they become material.

Common Mistakes That Cost Texas Businesses Real Money Around Audits

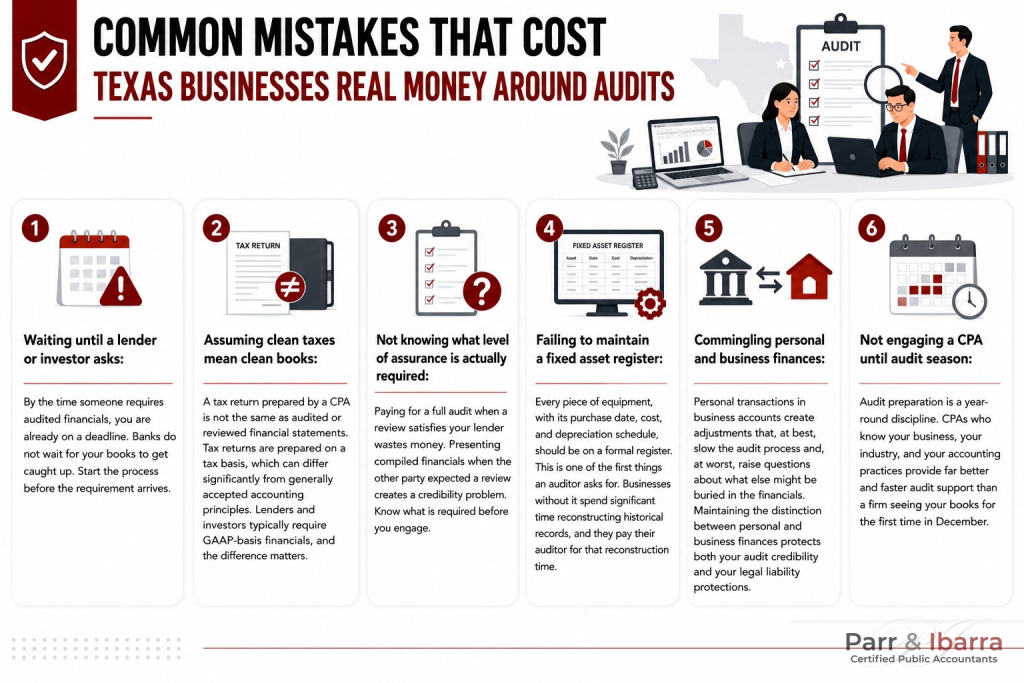

Waiting until a lender or investor asks: By the time someone requires audited financials, you are already on a deadline. Banks do not wait for your books to get caught up. Start the process before the requirement arrives.

Assuming clean taxes mean clean books: A tax return prepared by a CPA is not the same as audited or reviewed financial statements. Tax returns are prepared on a tax basis, which can differ significantly from generally accepted accounting principles. Lenders and investors typically require GAAP-basis financials, and the difference matters.

Not knowing what level of assurance is actually required: Paying for a full audit when a review satisfies your lender wastes money. Presenting compiled financials when the other party expected a review creates a credibility problem. Know what is required before you engage.

Failing to maintain a fixed asset register: Every piece of equipment, with its purchase date, cost, and depreciation schedule, should be on a formal register. This is one of the first things an auditor asks for. Businesses without it spend significant time reconstructing historical records, and they pay their auditor for that reconstruction time.

Commingling personal and business finances: Personal transactions in business accounts create adjustments that, at best, slow the audit process and, at worst, raise questions about what else might be buried in the financials. Maintaining the distinction between personal and business finances protects both your audit credibility and your legal liability protections.

Not engaging a CPA until audit season: Audit preparation is a year-round discipline. CPAs who know your business, your industry, and your accounting practices provide far better and faster audit support than a firm seeing your books for the first time in December.

How This Plays Out in Practice (illustrative)

The Dallas healthcare practice with four physicians and $3.2 million in annual billings had never needed an audit before approaching a regional bank for a $1.8 million expansion loan. The lender required two years of reviewed financial statements. Because the practice had worked with a CPA throughout the year, the review engagement was straightforward. The CPA identified two revenue recognition issues during the process, both immaterial to the loan but important to correct going forward. How CPAs support healthcare practices covers this kind of ongoing relationship in more detail. The reviewed financials were delivered in three weeks and the loan closed on schedule.

The Fort Worth logistics company with $8 million in revenue and a private equity buyer lined up faced a requirement for three years of audited financials in the LOI. The first year’s audit uncovered inconsistent depreciation methods and a deferred revenue item misclassified as earned income. Correcting these required restating one year of financials and delayed the transaction by 45 days, but it did not kill the deal. The corrected financials ultimately supported a higher valuation than the original records would have. The owner said afterward that he wished he had started 18 months earlier.

The Dallas nonprofit receiving a $900,000 federal grant triggered the Single Audit requirement under Uniform Guidance. Because the finance director had maintained the books with a CPA throughout the year, the Single Audit process was efficient. The auditors found no material weaknesses in internal controls and issued a clean opinion. Understanding tax-exempt status and what it requires from a compliance standpoint is foundational for any nonprofit organization operating at this level. The organization used the audited financials in its next grant application as evidence of financial stewardship, which the program officer cited as a key factor in approving a second award. For nonprofits concerned about the stability of federal funding, how nonprofits can avoid a federal funding freefall addresses the compliance and documentation standards that protect that funding relationship.

When to Hire a CPA for Audit and Assurance Work

The trigger is not always an external requirement. Sometimes it is simply the right time to bring your financial house in order.

Consider engaging a CPA for assurance services if you are approaching a significant financing event in the next 12 to 24 months. If you have new investors or partners wanting financial transparency, the time is now. If your business is approaching $1 million in annual revenue and has never had external eyes on the books, an agreed-upon procedures engagement or a compilation at minimum gives you a baseline to work from.

If you operate as a nonprofit, a government contractor, or in a regulated industry, you may already have a mandatory requirement you have been deferring. The cost of waiting is almost always higher than the cost of acting. Lenders who encounter disorganized financials mid-process slow deals, reduce loan amounts, or walk away entirely. Buyers who discover accounting issues in due diligence negotiate harder. And IRS examiners who encounter incomplete records during an examination have the authority to use estimation methods that rarely favor the taxpayer.

About Parr & Ibarra CPA

Audit and assurance work requires more than technical competence. It requires a CPA who understands the business environment their clients operate in, communicates clearly about findings and implications, and helps clients use the process as a strategic asset rather than a compliance checkbox.

Parr & Ibarra CPA serves business owners, investors, and organizations across Dallas, Fort Worth, and throughout Texas, with a practice that covers the full spectrum of assurance services: audits, reviews, compilations, and agreed-upon procedures. The firm’s year-round approach means clients are not strangers who arrive with a box of receipts in the fall. They are ongoing relationships. That familiarity makes assurance engagements faster, more accurate, and more insightful.

The firm also bridges the gap between assurance and tax planning, where the most strategic value tends to live. If a review engagement surfaces an accounting adjustment with tax implications, the same team handles the conversation. Nothing falls between the cracks.

For a CPA in Dallas Texas with genuine expertise in audit and assurance, schedule a consultation and speak with a team that treats your financial credibility as seriously as you do.

Frequently Asked Questions

What is the difference between an audit, a review, and a compilation?

An audit is the highest level of assurance, involving independent verification of financial statements and a formal CPA opinion. A review provides moderate assurance through analytical procedures and management inquiries but does not verify every line item independently. A compilation involves the CPA assembling financial statements from management-provided data without providing any assurance on accuracy. The level you need depends on your lender, investor, or regulatory requirements, and a CPA can help you determine the right engagement for your situation.

How has the IRS changed its audit approach in 2026?

The IRS has significantly expanded its use of automated digital matching systems that cross-reference income reported across 1099s, K-1s, and W-2s with what appears on business and individual returns. The agency has also increased resources focused on pass-through entities, high-income earners, and businesses claiming large deductions, including the 100% bonus depreciation that returned in 2026. This makes clean documentation and consistent financial records more important than ever, because discrepancies are now flagged algorithmically before a human examiner is involved.

Do Texas businesses have specific audit considerations that differ from other states?

Yes. Texas businesses must comply with franchise tax filings in addition to federal requirements, and errors in how taxable margin is calculated can trigger notices from the Texas Comptroller. Businesses that receive Texas grants, operate in regulated industries under state oversight, or have Texas-specific licensing requirements may have additional assurance obligations. Businesses operating across multiple states also need to ensure their financials correctly reflect the Texas-only portion of activity.

When do I need audited versus reviewed financial statements?

Audited financials are typically required for federal funding above $750,000, publicly traded entities, certain nonprofit state filings, and business acquisitions above a certain size. Reviewed financials are commonly required for commercial loans in the $500,000 to $3 million range, smaller M&A transactions, and situations where lenders want independent assurance without the cost and timeline of a full audit. Your lender’s term sheet or your attorney’s due diligence requirements will typically specify which level is needed.

How can I prepare my Dallas business for an audit without overspending?

The most cost-effective audit preparation happens year-round rather than in the weeks before the engagement begins. Maintain monthly bank reconciliations, keep supporting documentation organized in a cloud-based system, maintain a complete fixed asset register, and ensure your revenue recognition policies are consistent and documented. Businesses that hand auditors a clean, organized package at the start of an engagement pay meaningfully less in audit fees than those requiring the auditor to reconstruct records. Working with a CPA for ongoing bookkeeping also makes the audit process faster because the auditor already knows your accounts.

Is bonus depreciation relevant to an audit engagement?

Yes. Significant first-year deductions created by bonus depreciation need to be supported by clear documentation. For an audit, the CPA will want to see purchase records, placed-in-service dates, evidence that the property qualifies for bonus treatment, and the depreciation schedule showing how the deduction was calculated. Businesses that used bonus depreciation aggressively in 2026 and are later examined by the IRS need to produce this documentation on demand, which is straightforward if the records were maintained properly from the start.

What does a clean opinion in an audit report actually mean?

A clean opinion, technically called an unmodified opinion, means the CPA has determined the financial statements present the company’s financial position fairly and in accordance with generally accepted accounting principles. It is the most favorable audit result possible and is viewed by lenders, investors, and regulatory bodies as a strong affirmation of financial integrity. Modified opinions, adverse opinions, or disclaimers of opinion signal problems that can affect loan approvals, investor confidence, and regulatory standing in ways that are difficult and time-consuming to resolve after the fact.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.