Let’s be honest. Most business owners don’t think about taxes until something goes wrong, a surprise bill in April, a notice from the IRS, or a conversation with a friend who just found out they overpaid by $40,000 for three years running. By then, the best opportunities are already gone.

2026 is different, and that’s not just something to say to get your attention. The tax code went through one of its most significant overhauls in years. Some of those changes are genuinely good news for Texas business owners. Others require you to take specific action before the year ends or you lose the benefit entirely.

This guide covers what actually changed, how those changes affect businesses in Dallas and across Texas, and what smart owners are doing right now to come out ahead.

Tax Compliance Is Not Just About Filing on Time

Here’s something most business owners get backwards: they treat taxes like a chore you deal with once a year. File the return, write the check, move on. That mindset costs real money.

Actual compliance, the kind that protects you and lowers your tax bill is something you manage all year. It’s how you’ve set up your entity, how you’re categorizing expenses, whether your payroll taxes are going out on time, whether you’re making quarterly estimated payments, and whether you actually know what records you’re required to keep for your business. That last part matters more than people realize. The IRS doesn’t just look at your return, they look at whether you can prove it.

For a Dallas owner running an LLC or S-Corp, compliance has a lot of moving pieces: quarterly estimates, payroll deposits, sales tax if applicable, and the annual return itself. Slip on any of those, and the penalties compound quickly. But here’s the other side of it, the same tax code that creates those penalties also builds in significant advantages for owners who plan ahead. The people who pay the least in taxes aren’t cheating. They’re just more organized and more proactive than everyone else.

What Actually Changed in 2026 (And Why It Matters for Texas)

A few things that shifted this year are worth your attention, not because they make for interesting reading, but because they require actual decisions on your part.

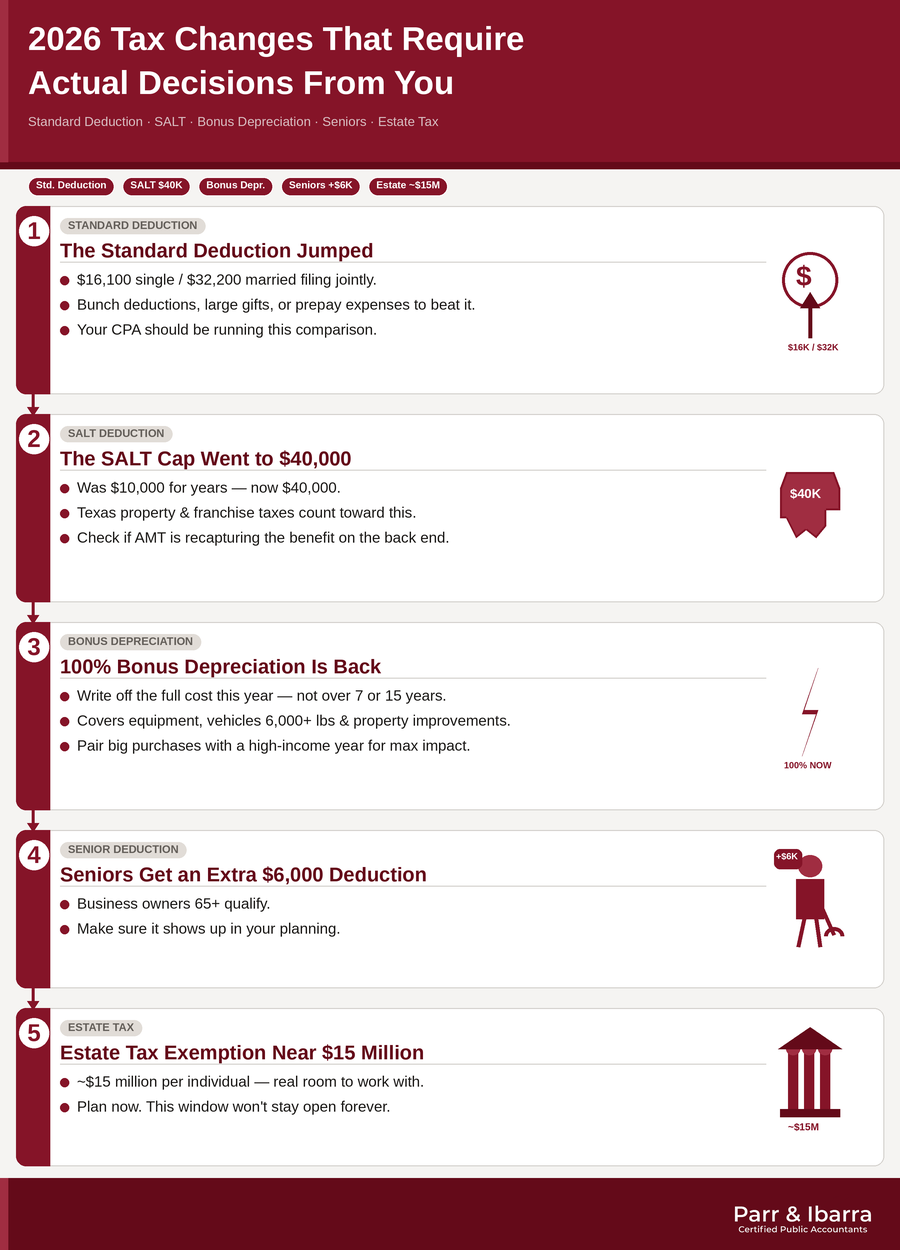

The Standard Deduction Jumped Significantly

It’s $16,100 now for single filers, $32,200 for married couples filing jointly. For business owners who used to itemize because it made sense, that math may have completely flipped. The smarter move in some situations is to bunch deductions into one year, make large charitable contributions, prepay certain expenses rather than spreading them evenly. Your CPA should be running this comparison for you, not leaving it as an afterthought.

The SALT Cap Went to $40,000

The State and Local Tax deduction was capped at $10,000 for years, which was a real problem for people in high-tax states. It’s now $40,000, with income-based phase-outs at higher levels. Texas doesn’t have a personal income tax, so the benefit looks different here than it does in California or New York, but it’s still meaningful. Texas businesses pay franchise tax. Texas property taxes are substantial. And many Dallas entrepreneurs own property or earn income in other states. The SALT increase helps in all of those situations. For higher earners, it’s also worth understanding whether you’re brushing up against Alternative Minimum Tax territory, the SALT change doesn’t help if AMT is recapturing it on the back end.

100% Bonus Depreciation Is Back

This one is significant. After phasing down from 100% in 2022 to 60% in 2024, full first-year bonus depreciation has been reinstated. That means if your business bought qualifying equipment, vehicles over 6,000 pounds GVWR, or certain property improvements in 2026, you can potentially write off the entire cost this year, not depreciate it over seven or fifteen years.

For a Dallas construction company adding equipment, or a medical practice investing in new technology, that’s a meaningful cash-flow difference. And the timing matters: pairing a large equipment purchase with a high-income year squeezes the most out of this.

Seniors Get an Extra $6,000 Deduction

Business owners 65 and older qualify for an additional $6,000 deduction this year. It sounds simple, but a surprising number of older Texas entrepreneurs who are winding things down or transitioning the business haven’t factored this in. If that’s you, make sure it shows up in your planning.

Estate Tax Exemption Is Near $15 Million Per Individual

For Texas business owners who are building something to pass on, the current exemption gives you meaningful room to work with. But these thresholds have changed before and likely will again. Understanding what business owners need to know about estate planning now while the exemption is high is considerably better than scrambling when it drops. The window may not stay open indefinitely.

The Core Tax Strategies That Actually Move the Needle

Get the Entity Structure Right First

Everything else sits on top of this. S-Corps, LLCs, C-Corps, and sole proprietorships don’t just have different names, they have genuinely different tax outcomes. What worked fine when you were making $150,000 may be costing you real money at $400,000.

A Dallas marketing agency earning $400,000 could realistically save $15,000 to $25,000 annually just by electing S-Corp status and structuring a reasonable salary rather than running everything through self-employment tax. That’s not aggressive, it’s standard planning. A C-Corp still makes sense if you’re reinvesting heavily and not taking distributions, since the 21% flat corporate rate is hard to beat in that scenario. But it creates double taxation on dividends, which changes the picture entirely for owners who need to pull cash out. A solid comparison of business entity structures and their tax implications is a good place to start if you haven’t revisited this in the last couple of years.

Don’t Underestimate Texas’s Tax Advantage, or Squander It

No personal state income tax is a big deal. A business owner clearing $500,000 a year is keeping $30,000 to $50,000 that their counterpart in California is writing a check for. But here’s what we see regularly: Texas owners who take that advantage for granted and then overpay federally because they haven’t bothered optimizing at that level. The savings at the state level can effectively disappear if your federal strategy isn’t working. Exploring tax strategies built specifically for high-income professionals often reveals deductions and structures that aren’t obvious without looking.

Understand the Texas Franchise Tax, It Bites People

Texas doesn’t have an income tax, but it does have a franchise tax, sometimes called the margin tax, and it catches business owners off guard more often than it should. If your revenue is above $2.47 million (the 2026 threshold), you’re filing and paying. The rate is 0.75% of taxable margin for most businesses, and 0.375% for qualifying wholesale and retail operations.

The tricky part is how you calculate taxable margin. You choose one of three methods: revenue minus cost of goods sold, revenue minus compensation, or 70% of total revenue. The right answer depends on your specific business, and picking the wrong method costs you. It’s not a complicated concept, but it requires someone who knows how the numbers fall for your particular operation.

Retirement Contributions: Still the Most Reliable Way to Reduce Income

Year after year, this is one of the highest-impact moves available to business owners, and it consistently gets underused. A SEP-IRA maxes out at $69,000 in 2026. A Solo 401(k) stacks contributions differently. A defined benefit plan can shelter significantly more for older, high-earning owners.

Consider a Dallas physician in private practice earning $750,000 annually. A well-designed defined benefit plan could shelter $200,000 or more, depending on age. At the 37% bracket, that’s over $70,000 in tax savings every single year. Working with a CPA to build a retirement strategy means the plan is actually calibrated to your income and entity structure, not just a generic contribution recommendation. If you operate as an S-Corp, the specifics around SEP-IRA contributions and how they work inside that structure matter more than most people realize.

Bonus Depreciation Needs to Be in Your Equipment Planning Right Now

If you’ve been sitting on a decision to upgrade vehicles, machinery, or technology, this is the year to act. With 100% bonus depreciation reinstated, a $120,000 equipment purchase is a $120,000 deduction taken entirely in the year of purchase. That’s not a spread-out benefit; that’s immediate.

For real estate investors and commercial property owners, pairing bonus depreciation with cost segregation amplifies this considerably. It’s one of the few strategies where timing your action correctly in a single year can shift your tax position by six figures.

Document Every Business Expense Seriously

This sounds basic because it is, but it’s also the single most common place we see money left on the table. The home office deduction. Vehicle mileage. Professional development. Health insurance premiums for self-employed owners. Business meals at 50%. These deductions exist, but only if you can prove them.

The IRS receipt requirements for self-employed deductions are specific, and “I have a rough estimate” doesn’t hold up under scrutiny. A Dallas real estate investor managing a property portfolio through an LLC might have $10,000 or more in legitimate deductions, management software, mileage, professional fees, a portion of phone and internet, that simply disappear if there’s no system for capturing them.

Strategies Worth Knowing If Your Income Is Above $300K

Tax Loss Harvesting

If you have a brokerage account alongside your business, strategic tax loss harvesting, selling positions that are down to offset gains elsewhere can trim your tax bill without materially changing your investment posture. At higher income levels, long-term capital gains get taxed at 20% plus a 3.8% Net Investment Income Tax. That adds up. For real estate owners in particular, there are additional strategies to reduce capital gains on property dispositions that go well beyond simple loss harvesting and are worth reviewing before any sale.

Charitable Giving Can Be Structured Smarter

Most people write a check to their favorite cause and call it a day. That works, but it’s not optimal. Channeling RSUs or appreciated stock into a donor-advised fund lets you take the deduction in a high-income year, avoid capital gains tax on the appreciation, and distribute the money to charities on your own timeline. For a Dallas business owner who just had a liquidity event like a business sale, a large real estate transaction, this is one of the best tools available for reducing taxable income in the year it spikes. The 2026 updates to charitable contribution rules are worth reviewing before you finalize your giving strategy for the year.

S-Corp Salary: Getting the Number Right Matters More Than You Think

The IRS expects S-Corp owners to pay themselves a reasonable salary, not a token one. Get it too low and you’re inviting scrutiny. Go too high and you’re paying unnecessary payroll taxes on income that could flow through as a distribution instead.

The right number depends on your industry, your role in the company, and what comparable positions actually pay. It’s not a guess. Getting this dialed in can mean several thousand dollars in self-employment tax savings annually, and it’s one of the areas where understanding the S-Corp tax benefits specific to your profession makes a real difference.

Cost Segregation for Real Estate Owners

If you own commercial real estate and you haven’t explored cost segregation, this is worth a conversation. A cost segregation study reclassifies parts of a building like wiring, flooring, fixtures, certain improvements into shorter depreciation schedules. With 100% bonus depreciation back in play, that reclassified property can be deducted immediately.

A Dallas investor who acquired a $1.5 million commercial property might identify $300,000 to $400,000 in assets eligible for accelerated depreciation. Understanding how the cost segregation process actually works before you commission a study helps you know what you’re getting and whether it pencils out for your situation. The real-world financial impact these studies produce is well-documented for the right property, it’s one of the most effective tax strategies available.

The Mistakes We See Over and Over

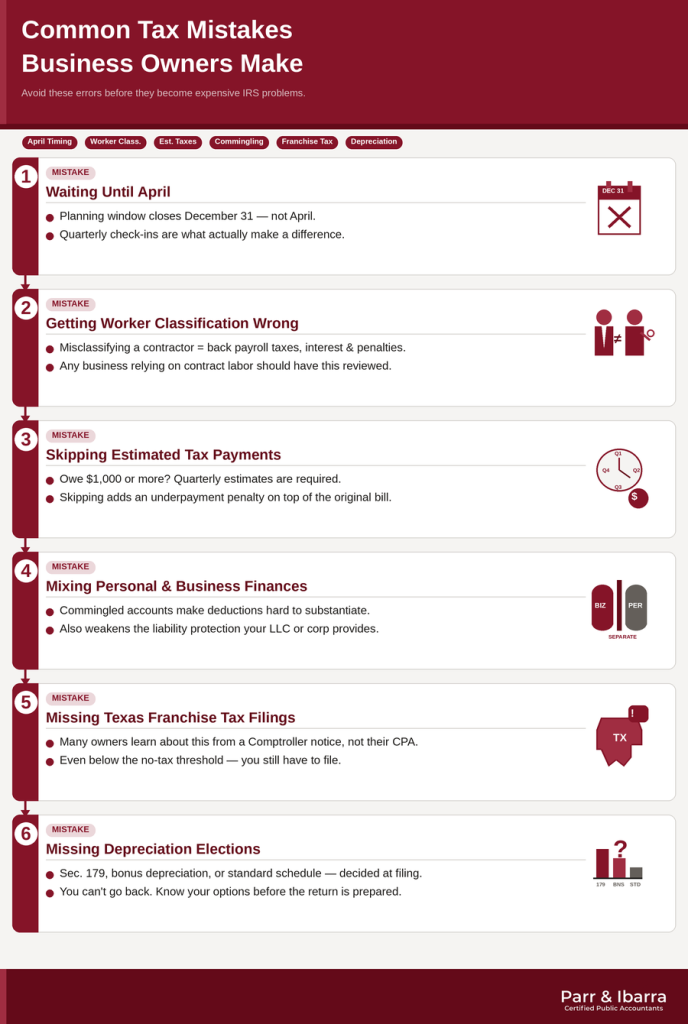

Waiting until April: By the time you’re filing, the planning window is closed. Quarterly check-ins are what make a difference.

Getting worker classification wrong: Misclassifying an employee as a contractor isn’t just a technicality, it triggers back payroll taxes, interest, and penalties. The tax implications of employees versus 1099 contractors are significant enough that any business relying heavily on contract labor should have this reviewed by a professional.

Skipping estimated tax payments: If you expect to owe $1,000 or more, quarterly estimates are required. Skipping them doesn’t delay the bill, it adds an underpayment penalty on top of it. Understanding the types of payroll and business taxes that require regular deposits keeps you from getting caught short.

Mixing personal and business finances: This one is partly a compliance issue and partly a liability issue. Commingled accounts make it nearly impossible to substantiate deductions cleanly, and they weaken the liability protections that your LLC or corporation is supposed to provide.

Not knowing about the Texas franchise tax filing requirement: A surprising number of Texas business owners find out about this obligation from a Comptroller notice rather than their accountant. Even if you’re below the no-tax threshold, you still have to file.

Missing depreciation elections: The decision between Section 179, bonus depreciation, and standard schedules has to be made at filing. You can’t go back. Knowing your options on depreciation, amortization, and expensing strategies before the return is prepared, not after. It is the only way to make sure you’re not leaving a deduction on the table permanently.

How This Plays Out in Practice (illustrative)

A SaaS founder in Dallas had been filing as a sole proprietor for three years, paying self-employment tax on every dollar of profit. After electing S-Corp status, setting a reasonable salary of $120,000, and maxing out a Solo 401(k), his tax savings in year one exceeded $35,000. None of that required anything aggressive. It required someone who noticed the opportunity.

A commercial real estate investor in Fort Worth owned three properties and had been using standard depreciation schedules across the board. A cost segregation study on her newest acquisition of a $2.2 million industrial property surfaced $480,000 in assets eligible for bonus depreciation. Combined with passive activity planning, it offset a significant portion of her consulting income. The investor’s guide to maximizing tax savings with cost segregation covers the mechanics behind exactly this kind of approach.

A restaurant group owner in Dallas with two locations was already running a tight operation, but his CPA helped him capture deductions he’d been missing from minimis equipment, staff meals, uniforms, and set up a SIMPLE IRA that reduced his taxable income while improving staff retention. On the franchise tax side, the compensation deduction method came out lower than the alternatives. Small decisions, compounded.

When Does It Actually Make Sense to Hire a CPA?

Once your revenue is above $150,000, the answer is almost always yes. Once you have employees, investment accounts, real estate, or complex deductions, it’s not really a question anymore. The math usually works out: most business owners who work with an experienced CPA save more in taxes than they spend in fees, often significantly more.

Beyond the savings, the risk picture has shifted. IRS audit exposure has changed in ways that affect businesses at every revenue level, and having a professional who has kept your records clean and your filings defensible is worth considerably more than it used to be.

The situations where it’s especially important to act now: you recently started a business and haven’t settled your entity structure, your income increased meaningfully this year, you’re planning to sell a business or real estate, you received anything from the IRS, or you honestly can’t remember the last time someone looked at your tax strategy with fresh eyes.

About Parr & Ibarra CPA

Parr & Ibarra CPA works with business owners, investors, and professionals across Dallas, Fort Worth, and throughout Texas. The practice was built specifically for this market, not as a national franchise, not as a seasonal tax prep service, but as a firm that works with clients year-round and actually understands what it takes to run a business here.

The work covers compliance, strategy, and the kind of ongoing communication that lets clients make good financial decisions in real time, not just in April. Industries served include real estate, professional services, healthcare, technology, construction, and retail.

If you’re looking for a CPA in Dallas Texas who treats your business like it matters, reach out and schedule a consultation.

Frequently Asked Questions

What are the biggest 2026 tax changes for Texas business owners?

The return of 100% bonus depreciation, the SALT cap increasing to $40,000, higher standard deductions, the new $6,000 deduction for seniors, and expanded family credits are the headline changes. For Texas specifically, the SALT increase benefits owners with property taxes and franchise tax obligations, and bonus depreciation is particularly valuable for commercial real estate investors and businesses purchasing capital equipment this year.

How do I reduce my business taxes legally in 2026?

Maximize retirement contributions, take advantage of bonus depreciation if you’re buying qualifying property, review whether your entity structure is still right for your income level, document and deduct all legitimate business expenses, and consider charitable vehicles like donor-advised funds if you’re having a high-income year. These aren’t loopholes, they’re the tax code working as designed.

Does Texas’s lack of state income tax affect how I should approach federal taxes?

Yes. The state tax savings are real, but they don’t automatically transfer to your federal return. Many Texas owners save at the state level and then give it back federally because they haven’t optimized it there. The two should be planned together.

Is bonus depreciation really 100% again in 2026?

Yes, it was reinstated after phasing down to 60% in 2024. New and used qualifying property with a depreciation life of 20 years or less is eligible. That covers most equipment, business vehicles over 6,000 pounds, technology hardware, and certain improvements. The building structure itself doesn’t qualify, which is why cost segregation studies are so valuable for real estate investors, they surface the components that do.

Who has to file the Texas franchise tax?

Most entities doing business in Texas. If your revenue is above $2.47 million (the 2026 threshold), you’re calculating and paying based on taxable margin. Below that threshold, most businesses still need to file a No Tax Due report. Missing this entirely is more common than it should be.

When is professional CPA help worth it versus tax software?

Tax software is fine for a simple W-2 return. Once you have a business, employees, real estate, investment accounts, or any complexity, the stakes are too high and the potential savings too real to leave it to a program. The value of professional planning compounds over time, it’s rarely just about one year’s return.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.Tax Planning Strategies for Texas Businesses in 2026IRS Guides & Tax Filing in 2026