If you own commercial property, a rental portfolio, or a business facility in Texas and you have not looked into cost segregation, there is a strong chance you are overpaying taxes every single year.

Most property owners depreciate their real estate over 27.5 or 39 years and call it a day. That is the default. But the IRS tax code offers a far more powerful option, one that lets you front-load depreciation deductions, recover cash faster, and reinvest capital into growing your business or portfolio.

Cost segregation is that strategy. It has been around for decades, it is fully IRS-approved, and with 100% bonus depreciation reinstated in 2026, it is one of the most valuable tax tools available right now. Leveraging bonus depreciation alongside cost segregation in the post-reform environment is how Texas property owners are capturing the most from this moment in the tax calendar.

This guide is written for Dallas entrepreneurs, Texas real estate investors, and small business owners who want to understand cost segregation at a deep level, know when it makes sense, and learn how to implement it correctly. Whether you are buying a new property, you recently completed a renovation, or you own real estate you acquired years ago, this article will walk you through everything you need to know.

What Is Cost Segregation?

Cost segregation is an IRS-approved tax strategy that involves reclassifying certain components of a commercial or residential rental property into shorter depreciation categories. Instead of treating the entire building as a single asset depreciated over 27.5 years (residential) or 39 years (commercial), a cost segregation study separates the property into its individual components, each with its own depreciation timeline.

Understanding how a cost segregation study works at a foundational level is the starting point for every property owner evaluating this strategy. Under standard rules, items like flooring, lighting fixtures, cabinetry, landscaping, parking lots, and specialized HVAC systems may qualify for 5-year, 7-year, or 15-year depreciation rather than the standard 39-year schedule. This acceleration means larger deductions in the early years of ownership, which translates directly into reduced taxable income and real cash savings.

The study itself is performed by a team that typically includes engineers and tax professionals. They conduct a physical inspection of the property, review construction cost documents, and produce a detailed report that categorizes each building component by its depreciation class life.

A well-executed cost segregation study does not change how much you depreciate. It changes when you take those deductions. And as any experienced CPA will tell you, maximizing deductions through depreciation, amortization, and expensing strategies is where timing makes the most measurable difference to your tax position.

Why Cost Segregation Matters More in 2026

The 2026 tax landscape has created a nearly perfect environment for cost segregation. Three major developments are working in property owners’ favor simultaneously, and the full picture of 2026 federal tax law changes is worth reviewing before making any major depreciation election this year.

100% Bonus Depreciation Is Back: After tapering down from 100% in 2022 to 60% in 2024, bonus depreciation has been fully reinstated at 100% for qualifying property. What the return of 100% bonus depreciation means for property investors is significant: when a cost segregation study identifies components with 5-year or 15-year class lives, those components can be fully expensed in year one. For a $2 million commercial property in Dallas, that could mean $400,000 or more in immediate deductions.

Tax Brackets Have Shifted: With an approximately 2.7% inflation adjustment to the 2026 brackets, some taxpayers will find themselves in lower marginal rates than expected. But high-income earners and investors are still facing meaningful federal tax liability, and large depreciation deductions are one of the cleanest ways to reduce that burden.

No State Income Tax in Texas: This is a permanent and significant advantage for Texas business owners. You are not paying state income tax on your earnings, which means your federal deductions carry even more weight. A $500,000 deduction in California saves you both federal and state tax. In Texas, that same deduction is applied entirely at the federal level, but the absence of state income tax means more of your overall income stays in your pocket year after year. Texas property owners investing in energy-efficient systems should also note that clean energy tax breaks available to businesses in 2026 can layer additional deductions on top of cost segregation benefits.

The SALT Cap Has Increased: The state and local tax deduction cap has been raised to $40,000 for 2026, with income-based phaseouts. This will not affect most Texas business owners the same way it affects residents of high-tax states, but it does matter for Texas investors with multi-state operations.

All of these factors together make cost segregation an especially timely strategy in 2026.

How a Cost Segregation Study Works: A Step-by-Step Breakdown

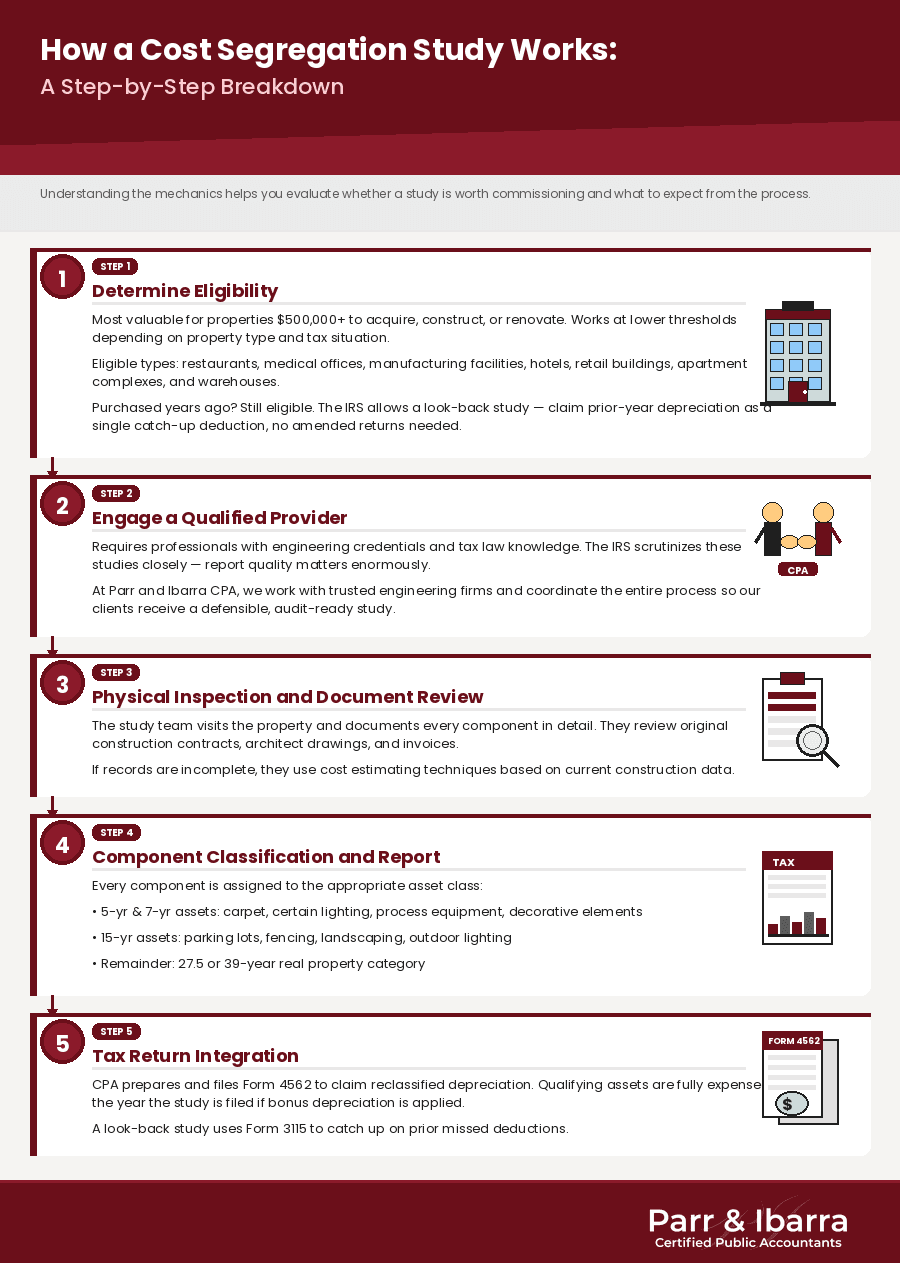

Understanding the mechanics helps you evaluate whether a study is worth commissioning and what to expect from the process. A complete guide to the cost segregation process covers every stage in detail, but the overview below gives you the framework.

Step 1: Determine Eligibility

Cost segregation is most valuable for properties that cost $500,000 or more to acquire, construct, or renovate. That said, studies can make financial sense at lower thresholds depending on the property type and your tax situation. Properties that tend to generate the strongest results include restaurants, medical offices, manufacturing facilities, hotels, retail buildings, apartment complexes, and warehouse or distribution centers.

If you purchased a property years ago, you are still eligible. The IRS allows a look-back study, which captures the depreciation you could have claimed in prior years as a single catch-up deduction in the current year, without filing amended returns.

Step 2: Engage a Qualified Provider

This is not a study you should attempt to DIY or delegate to someone without engineering credentials. A proper cost segregation study requires professionals who understand both construction cost allocation and tax law. The IRS scrutinizes these studies closely, and understanding how an IRS audit works and what documentation it expects makes clear why the quality of the engineering report matters enormously.

At Parr and Ibarra CPA, we work with trusted engineering firms and coordinate the entire process so our clients receive a defensible, audit-ready study that stands up to IRS review.

Step 3: Physical Inspection and Document Review

The study team visits the property and documents every component in detail. They review original construction contracts, architect drawings, and invoices. If records are incomplete, they use cost estimating techniques based on current construction data.

Step 4: Component Classification and Report

Every component is assigned to the appropriate asset class. Personal property components (5-year and 7-year assets) include things like carpet, certain lighting, process equipment, and decorative elements. Land improvements (15-year assets) include parking lots, fencing, landscaping, and outdoor lighting. The remainder stays in the 27.5 or 39-year real property category.

Step 5: Tax Return Integration

Your CPA prepares and files Form 4562 to claim the reclassified depreciation. If bonus depreciation is applied, those qualifying assets are fully expensed in the year the study is filed. A look-back study uses Form 3115 to catch up on prior missed deductions. The real-world financial impact of cost segregation studies shows exactly what this looks like when the numbers are applied to actual properties.

A Dallas Real-World Example (illustrative)

Let us walk through a scenario that is common in Dallas right now.

A Dallas entrepreneur purchases a 10,000-square-foot medical office building for $3 million. Under standard depreciation, they would divide the building value of roughly $2.8 million (after land allocation) by 39 years and deduct approximately $71,800 per year. Over the first five years, that is about $359,000 in total deductions.

After a cost segregation study, the engineer identifies $700,000 in 5-year personal property components and $210,000 in 15-year land improvements. With 100% bonus depreciation in effect, all $910,000 of those components can be expensed immediately in year one. The remaining $1.89 million is still depreciated over 39 years.

In year one alone, the owner now has access to deductions of roughly $958,000 instead of $71,800. Assuming a combined effective federal tax rate of 37%, that is an additional $326,000 in tax savings in the first year, cash that can be used to fund operations, acquire another property, or build reserves.

The tangible benefits of cost segregation in real estate investment are demonstrated clearly in scenarios like this one. And for investors who want to understand how the IRS views the property owner’s role in generating those results, how the IRS classifies real estate dealers versus investors directly shapes which deductions are available and how aggressively they can be applied.

This is not a loophole. This is exactly what the tax code was designed to allow.

Advanced Strategies to Maximize the Benefit

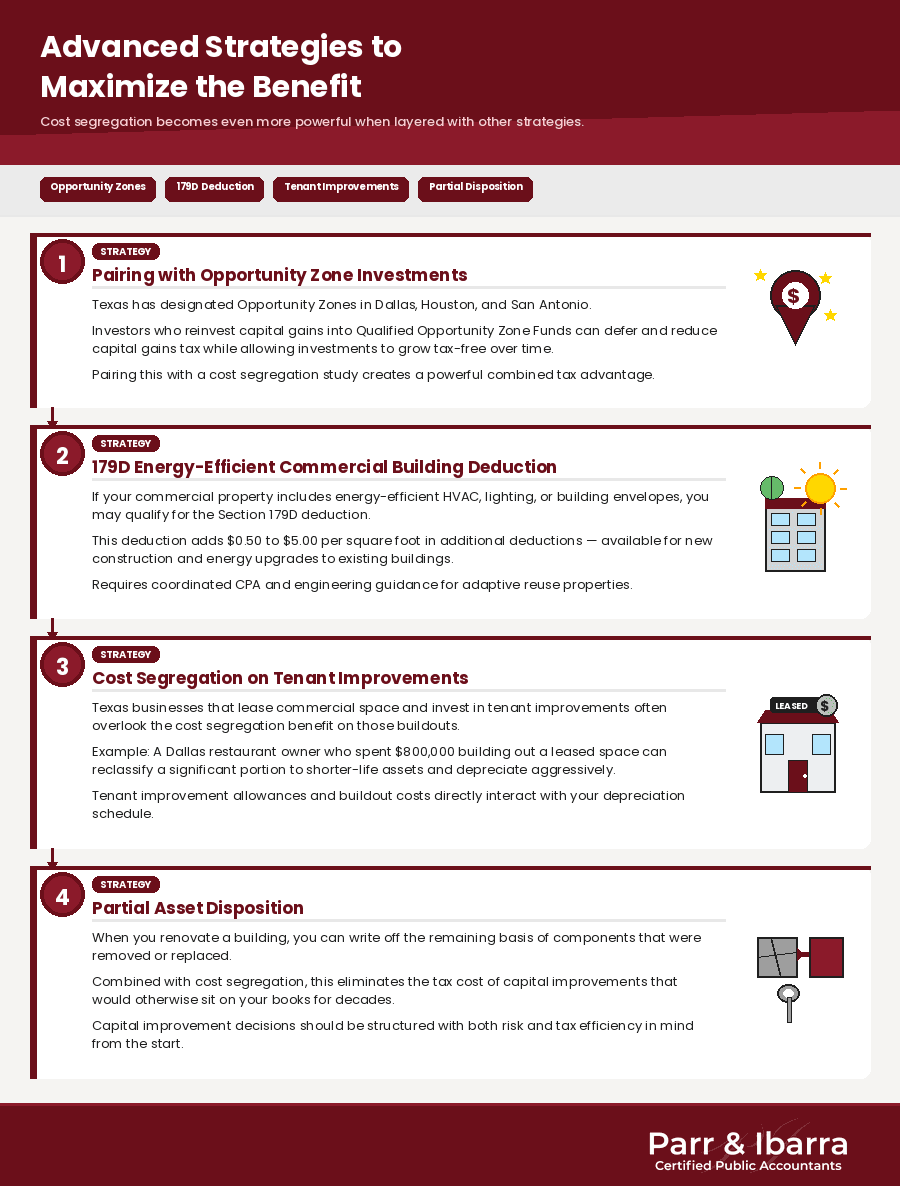

Cost segregation is powerful on its own, but it becomes even more powerful when layered with other strategies.

Pairing with Opportunity Zone Investments

Texas has several designated Opportunity Zones, including areas in Dallas, Houston, and San Antonio. Investors who reinvest capital gains into Qualified Opportunity Zone Funds can defer and reduce capital gains tax while allowing investments to grow tax-free over time. How the most recent legislation reshaped Qualified Opportunity Zones and what it means for 2026 clarifies exactly where the planning opportunities now sit for Texas investors pairing this with a cost segregation study.

179D Energy-Efficient Commercial Building Deduction

If your commercial property includes energy-efficient HVAC systems, lighting, or building envelopes, you may qualify for the Section 179D deduction in addition to cost segregation benefits. This deduction can add $0.50 to $5.00 per square foot in additional deductions, and it is available for both new construction and certain energy upgrades to existing buildings. For investors acquiring or developing adaptive reuse properties, GAAP accounting considerations for adaptive reuse real estate projects add another layer of complexity that requires coordinated CPA and engineering guidance.

Cost Segregation on Tenant Improvements

Texas businesses that lease commercial space and invest in tenant improvements often overlook the cost segregation benefit on those buildouts. If you are a Dallas restaurant owner who spent $800,000 building out a leased space, a significant portion of those improvements can be reclassified to shorter life assets and depreciated aggressively. For landlords managing these arrangements from the property owner side, a comprehensive tax guide for landlords and real estate investors covers how tenant improvement allowances and buildout costs interact with your depreciation schedule.

Partial Asset Disposition

When you renovate a building, you can write off the remaining basis of components that were removed or replaced. Combined with cost segregation, this eliminates the tax cost of capital improvements that would otherwise sit on your books for decades. Pairing this with insurance strategies for real estate investors that protect properties while maximizing tax deductions ensures that your capital improvement decisions are structured with both risk and tax efficiency in mind from the start.

Common Mistakes Texas Property Owners Make

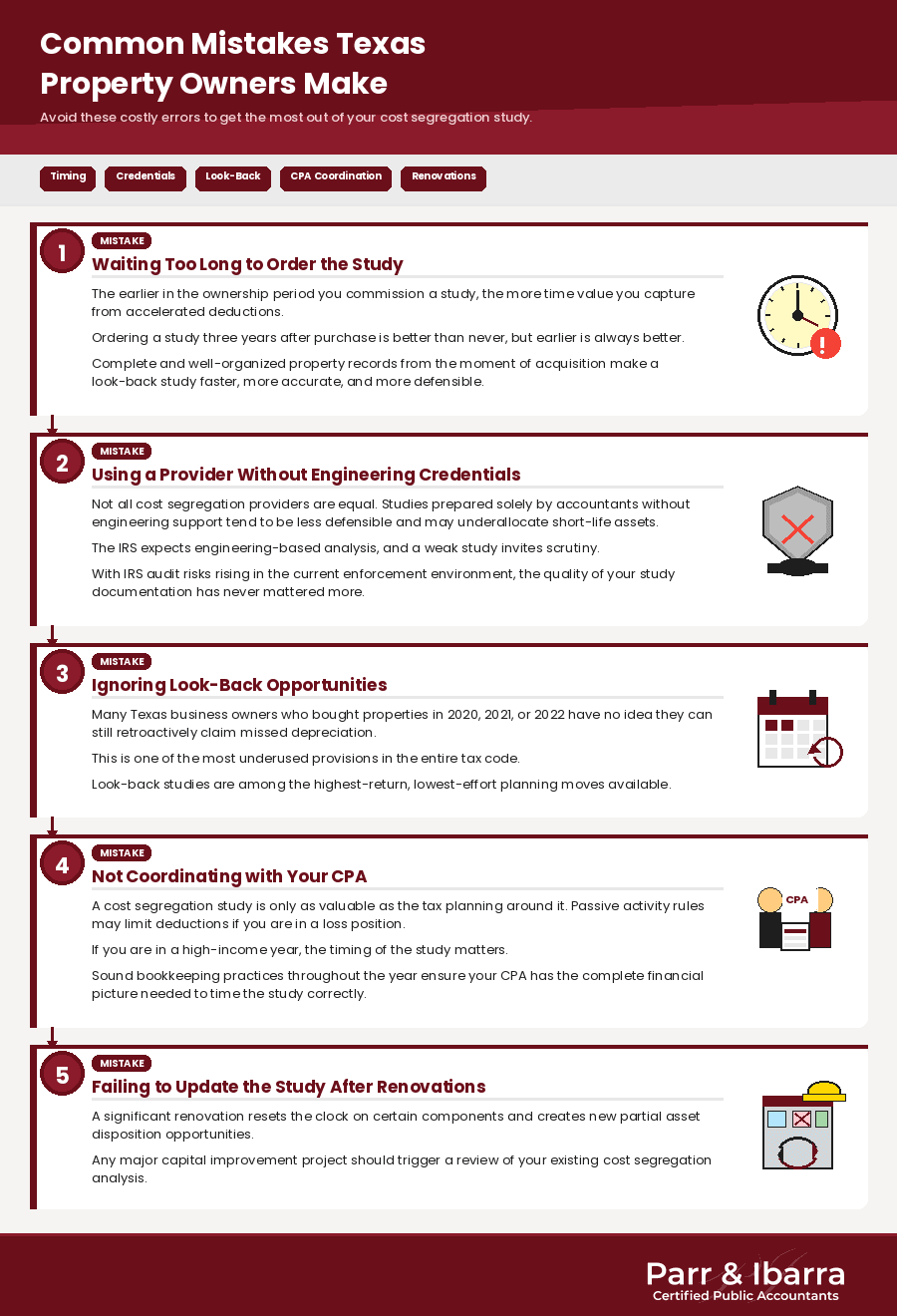

Waiting too long to order the study: The earlier in the ownership period you commission a study, the more time value you capture from accelerated deductions. Ordering a study three years after purchase is better than never, but earlier is always better. Keeping complete and well-organized business and property records from the moment of acquisition is the infrastructure that makes a look-back study faster, more accurate, and more defensible.

Using a provider without engineering credentials: Not all cost segregation providers are equal. Studies prepared solely by accountants without engineering support tend to be less defensible and may underallocate short-life assets. The IRS expects engineering-based analysis, and a weak study invites scrutiny. With IRS audit risks rising in the current enforcement environment, the quality of your study documentation has never mattered more.

Ignoring look-back opportunities: Many Texas business owners who bought properties in 2020, 2021, or 2022 have no idea they can still retroactively claim missed depreciation. This is one of the most underused provisions in the entire tax code. Smart deduction strategies for real estate professionals consistently identify look-back studies as among the highest-return, lowest-effort planning moves available.

Not coordinating with your CPA: A cost segregation study is only as valuable as the tax planning around it. If you are in a loss position, the deductions may be limited by passive activity rules. If you are in a high-income year, the timing of the study matters. Sound bookkeeping practices throughout the year are what make that coordination possible and ensure your CPA has the complete financial picture needed to time the study correctly.

Failing to update the study after renovations: A significant renovation resets the clock on certain components and creates new partial asset disposition opportunities. Any major capital improvement project should trigger a review of your existing cost segregation analysis.

Texas Franchise Tax: A Brief but Important Note

Texas does not have a personal income tax, but it does impose a franchise tax on most businesses operating in the state. For most businesses, the franchise tax is based on total revenue minus a deduction for either cost of goods sold or compensation. This is distinct from federal income tax planning, but it matters.

Texas business owners should work with a CPA who understands both the federal and state tax picture. How Texas state-level business tax obligations interact with federal planning decisions is a layer that out-of-state advisors frequently miss. Strategies that reduce federal taxable income do not automatically reduce Texas franchise tax liability, and how tariffs and other federal changes affect state sales and use tax obligations is a related consideration for Texas investors with multi-state operations. Parr and Ibarra CPA serves clients across the Dallas-Fort Worth area with a full understanding of both systems.

Who Benefits Most from Cost Segregation?

Small Business Owners

If you own your business property, either outright or through a related entity, cost segregation can generate deductions that offset active business income. Understanding how business entity structures affect your overall tax position is the foundation of determining how cost segregation deductions flow through to your personal return. Under certain circumstances, real estate professionals can use real property losses to offset non-passive income, which creates even greater tax reduction potential.

Commercial Real Estate Investors

Investors with multiple properties can stack cost segregation benefits across their portfolio, creating large deductions that offset rental income. The S-Corporation structure carries specific tax advantages for real estate professionals that interact directly with how cost segregation deductions are classified and applied. Combined with the 2026 reinstatement of 100% bonus depreciation, a strategic acquisition and study can dramatically reduce or eliminate tax on rental income for several years.

Entrepreneurs Who Recently Completed a Build-Out

If you built a new commercial facility, renovated an existing one, or signed a lease and funded a significant tenant improvement, you likely have substantial short-life assets sitting in the wrong depreciation category. Essential tax strategies for founders and early-stage business owners consistently identify the post-build-out period as one of the highest-value windows to commission a cost segregation study.

High-Income Earners with Real Estate Holdings

The 2026 tax brackets mean that the top marginal federal rate applies to ordinary income above approximately $626,350 for single filers and $751,600 for married filing jointly. For high earners with significant real estate holdings, tax strategies designed specifically for high-income professionals identify cost segregation as one of the most effective tools for reducing exposure at the top bracket. For those building multi-entity real estate structures, using a family limited partnership as part of your financial and estate strategy adds a layer of planning that determines how cost segregation deductions pass through to individual owners.

When Should You Hire a CPA?

If you are reading this and thinking it sounds complicated, that instinct is correct. Cost segregation intersects with passive activity rules, at-risk rules, bonus depreciation elections, entity structure, estate planning, and state tax, all at once. Getting one piece wrong can eliminate the benefit or create downstream problems.

You should work with a CPA if you own or are acquiring commercial or rental property worth $500,000 or more. You should also engage professional guidance if you are planning a significant renovation, if you have not previously worked with a cost segregation provider, or if you recently had a major change in income or business structure. The difference between a CPA who prepares returns and a tax strategist who builds plans is exactly the distinction that determines whether cost segregation is executed correctly or left on the table.

The right time to bring in a CPA is before you make the decision, not after. Too many Dallas entrepreneurs come to us after the fact, looking to undo elections or recover from planning errors that could have been avoided entirely. For investors thinking about the longer-term picture, what business owners need to know about estate planning and wealth transfer adds critical context to any major depreciation decision that will affect your portfolio for years to come.

Why Choose Parr & Ibarra CPA?

Parr and Ibarra CPA is a Dallas-based firm serving business owners, investors, and professionals across Texas. We understand the Dallas commercial real estate market, the nuances of Texas franchise tax, and the strategic tax planning needs of high-growth businesses and high-income individuals.

Our approach goes beyond compliance. We act as strategic advisors who proactively identify opportunities like cost segregation, look-back studies, and bonus depreciation elections before tax season forces a rushed decision. Having audit protection in place before the IRS comes knocking is part of how we structure every client engagement. For investors managing growing portfolios, CFO-level financial guidance is increasingly essential for scaling a real estate operation in a market as active and competitive as DFW.

We work with clients who own everything from single-tenant commercial properties in Uptown Dallas to multi-family portfolios spanning the DFW metro. We bring engineering partners into the cost segregation process to ensure every study is accurate, defensible, and filed correctly.

Our clients value the combination of deep tax knowledge, genuine accessibility, and a firm that stays current with every IRS update. When bonus depreciation rules changed in 2026, we were already briefing clients on the implications. When SALT limits shifted, we were updating planning strategies before most firms had read the legislation.

For investors considering capital gains management alongside depreciation planning, seven proven strategies to reduce capital gains tax on real estate and how to minimize capital gains tax across investment dispositions round out the advisory picture we bring to every client conversation.

If you are a Texas business owner or investor looking for a CPA in Dallas who treats your tax strategy as seriously as you treat your business, we would like to talk.

Conclusion: Stop Depreciating the Slow Way

Cost segregation is not a niche strategy for big developers. It is an IRS-approved method for accelerating real cash savings that every qualified property owner in Texas should be evaluating. With 100% bonus depreciation reinstated in 2026, the window to maximize these benefits is open right now.

Whether you are a Dallas entrepreneur who just completed a commercial build-out, a real estate investor expanding your Texas portfolio, or a business owner who has owned property for years without ever looking at this strategy, there is likely money on the table that belongs to you. Maximizing tax savings through a cost segregation study designed specifically for real estate investors is the practical next step for any investor ready to act before year-end.

The first step is a conversation. Schedule a consultation with Parr and Ibarra CPA today and find out exactly what a cost segregation study could mean for your tax position this year.

Visit aibarra.cpa or call our Dallas office to speak with a CPA who understands your market, your goals, and the 2026 tax landscape inside and out.

Frequently Asked Questions

What changed in 2026 that makes cost segregation more valuable?

The most significant change is the full reinstatement of 100% bonus depreciation for qualifying property. This means that assets identified through a cost segregation study with 5-year, 7-year, or 15-year class lives can be fully expensed in the year they are placed in service, rather than depreciated over time. Combined with adjusted tax brackets and higher estate tax exemptions, 2026 is an especially favorable environment for property owners who have not yet commissioned a study.

Can Texas businesses benefit specifically from cost segregation?

Yes, and in some ways more than businesses in high-tax states. Because Texas has no state income tax, every dollar of accelerated depreciation generates savings at the federal level without the complexity of state tax implications. Texas franchise tax is calculated differently and is not directly affected by depreciation elections, but the net federal tax savings flow directly to the bottom line.

Is bonus depreciation still available in 2026?

Yes. After a phase-down that reduced bonus depreciation to 60% in 2024, it has been fully restored to 100% for 2026 and qualified property placed in service after the effective date. This applies to components identified through a cost segregation study that fall into 5-year, 7-year, or 15-year asset classes.

What if I bought my property several years ago? Is it too late?

No. The IRS allows look-back cost segregation studies for properties you have already owned. Using a Form 3115 change in accounting method, you can claim all the missed accelerated depreciation in a single catch-up deduction in the current tax year, without amending prior returns. Many Texas investors who acquired property during the 2019 to 2022 period are candidates for significant look-back benefits.

Do I need an engineer to perform the cost segregation study?

You do not need to hire an engineer directly, but the study provider should include engineering expertise in their methodology. The IRS expects asset classification to be based on construction cost analysis and engineering principles, not estimates. A study prepared without engineering support is more likely to be challenged in an audit and less likely to capture the full benefit available.

How much does a cost segregation study cost, and is it worth it?

Study fees typically range from $5,000 to $15,000 for properties in the $500,000 to $5 million range, depending on property type and complexity. For most commercial properties, the first-year tax savings far exceed the study fee, often by a factor of 10 to 30 or more. The study cost is also deductible as a professional services expense.

When should I talk to a CPA about cost segregation?

Ideally, before you close on a property or complete a major renovation. Early engagement allows your CPA to coordinate the study timing with your overall tax strategy, plan for passive activity rule implications, and ensure bonus depreciation elections are filed correctly. If you already own property and have never explored this, the second-best time to act is now.

This article is intended for informational purposes and reflects general tax principles as of 2026. Tax situations vary. Consult a qualified CPA like Parr & Ibarra CPA before making tax or investment decisions.