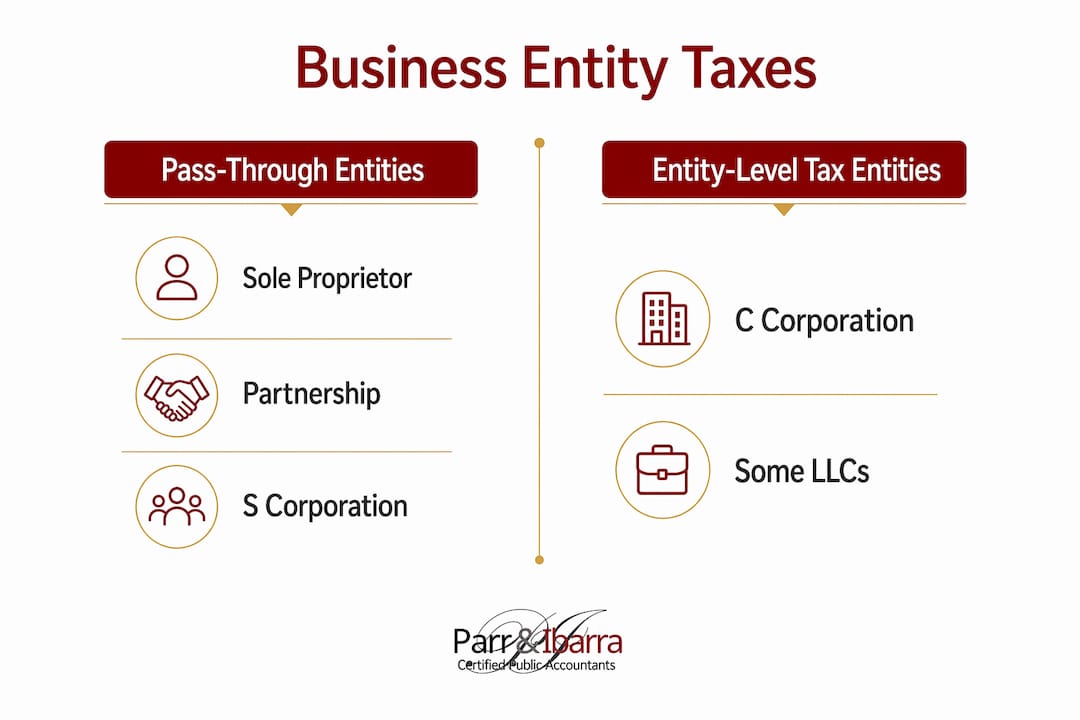

Business entity structure taxes determine how much you pay the IRS, what forms you file, and whether your profits are taxed once or twice. The IRS recognizes five main structures: sole proprietorship, partnership, LLC, S Corporation, and C Corporation. Each carries a distinct tax treatment, and choosing the wrong one costs real money. For small business owners in the Dallas-Fort Worth area and beyond, understanding these differences is the foundation of any sound financial plan.

What are the main types of business entities and their tax treatment?

Business structure determines the tax form filed, with sole proprietors filing Schedule C, partnerships filing Form 1065, S Corps filing Form 1120-S, and C Corps filing Form 1120. That single fact shapes your entire tax year.

Sole proprietorship is the default structure for any single-owner business. You report profit and loss on Schedule C, attached to your personal Form 1040. The IRS requires you to file Schedule SE if net earnings reach $400 or more. This structure is simple, but it offers no separation between your personal and business tax liability.

Partnerships and multi-member LLCs are pass-through entities. The business itself pays no income tax. Instead, each partner or member reports their share of profits on their personal return. This avoids entity-level taxation, though each partner still owes self-employment tax on their share of earnings.

LLCs deserve a closer look because they are flexible by design. LLC profits flow through to members, avoiding corporate-level taxation unless the owner elects C Corp tax status. A single-member LLC is taxed like a sole proprietorship by default. A multi-member LLC is taxed like a partnership. Owners can also elect S Corp or C Corp treatment, which changes the tax picture significantly.

S Corporations pass income through to shareholders, avoiding entity-level tax. The key distinction is that owners who work in the business must pay themselves a reasonable salary. Only the salary portion is subject to payroll taxes. Distributions above that salary are not, which is where the tax savings come from.

C Corporations pay income tax at the entity level, currently at a 21% corporate income tax rate. When the corporation distributes profits as dividends, shareholders pay tax again on those dividends. This is the double taxation problem that makes C Corps a poor fit for most small businesses.

Here is a quick comparison of how each structure handles income tax:

| Entity Type | Taxed at Entity Level? | Pass-Through to Owner? | Self-Employment Tax? |

|---|---|---|---|

| Sole proprietorship | No | Yes | Yes, on all net earnings |

| Partnership / multi-member LLC | No | Yes | Yes, on distributive share |

| Single-member LLC | No | Yes | Yes, on all net earnings |

| S Corporation | No | Yes | Only on reasonable salary |

| C Corporation | Yes (21%) | No (dividends taxed separately) | No |

State-level taxes add another layer. Some states impose franchise taxes or gross receipts taxes on top of federal obligations. These fees apply regardless of which federal structure you choose, and they can reduce the net benefit of a tax-efficient entity type.

How does self-employment tax affect owners across entity types?

Self-employment tax is a 15.3% tax on net earnings from self-employment, covering Social Security and Medicare. It applies on top of income tax. For a sole proprietor earning $80,000 in net profit, that means roughly $12,240 in self-employment tax before a single dollar of income tax is calculated.

Sole proprietors and single-member LLC owners pay self-employment tax on all net earnings. There is no way around it under those structures. The tax hits every dollar of profit, which is why many owners feel the pinch as their business grows.

S Corp owners follow a different path. The IRS requires them to pay themselves a reasonable salary, and that salary is subject to payroll taxes, which are the employer-employee equivalent of self-employment tax. But distributions above the salary are not subject to those taxes. That gap is where meaningful savings appear.

Here is a concrete example showing how the structure changes the tax burden:

- Sole proprietor, $100,000 net profit. Pays 15.3% self-employment tax on the full $100,000, totaling roughly $15,300 in self-employment taxes alone.

- S Corp owner, $100,000 net profit, $60,000 reasonable salary. Pays payroll taxes only on the $60,000 salary. The remaining $40,000 is taken as a distribution, free of self-employment tax. Estimated savings: roughly $6,120.

- C Corp owner. Pays no self-employment tax personally, but the corporation pays 21% on its profits before any distribution reaches the owner.

The S Corp also qualifies for the 20% Qualified Business Income deduction under IRC Section 199A, which further reduces taxable income for eligible owners. That deduction stacks on top of the self-employment tax savings.

Pro Tip: Set your S Corp salary based on what the IRS considers reasonable for your role and industry. Paying yourself too little is a red flag. The IRS actively audits S Corp owners who take minimal salaries to avoid payroll taxes, and non-compliance risks back taxes and penalties.

When should you consider making an S-Corp election?

The S-Corp election makes financial sense once your net profit consistently exceeds $40,000. Below that threshold, the cost of running payroll, filing a separate corporate return, and maintaining compliance often exceeds the tax savings. Above it, the math shifts decisively in your favor.

At $60,000 in net profit, the self-employment tax savings from an S-Corp election typically outpace the added accounting and payroll costs by a meaningful margin. As profits climb toward $100,000 and beyond, the savings compound. S-Corp elections provide the strongest tax savings once net profit exceeds $40,000, by reducing the 15.3% self-employment tax on distributions above a reasonable salary.

Before electing S-Corp status, confirm you meet the eligibility requirements:

- The business must be a domestic corporation or LLC.

- You can have no more than 100 shareholders.

- All shareholders must be U.S. citizens or permanent residents.

- Only one class of stock is permitted.

- Certain entity types, including partnerships and most corporations, cannot be shareholders.

These restrictions matter. If you plan to bring in investors, especially institutional ones, the S-Corp structure may not fit. Venture capital firms typically require C Corp status because they need preferred stock and complex ownership arrangements.

The payroll obligations for S-Corp owners also require quarterly payroll tax deposits and year-end W-2 filings. That is real administrative work. Factor in the cost of a payroll service or CPA support before committing to the election.

Pro Tip: If you are currently a single-member LLC earning above $40,000 net, you can elect S-Corp tax treatment without forming a new entity. File IRS Form 2553 to make the election. Timing matters, so work with a CPA to hit the correct deadline.

What are the tax implications of C Corps versus pass-through entities?

C Corporations pay income tax at the entity level. The current federal corporate rate is 21%. After paying that tax, any profits distributed to shareholders as dividends get taxed again at the shareholder’s personal rate. That is double taxation, and it is the primary reason C Corps are a poor fit for most small business owners.

Pass-through entities, including S Corps, partnerships, and LLCs, avoid entity-level tax entirely. Profits flow directly to the owner’s personal return. The owner pays income tax once, at their individual rate, with no second layer of taxation on distributions.

C Corps do offer specific advantages worth knowing:

- They can issue multiple classes of stock, which attracts venture capital.

- They have no shareholder limits or citizenship restrictions.

- They are better suited for businesses planning complex international operations.

- Retained earnings can be reinvested at the 21% corporate rate, which may be lower than the owner’s personal rate in high-income years.

C Corps remain the standard for venture capital funding because of complex ownership structures and separate entity taxation. If you are building a business to raise institutional capital or go public, C Corp is the right structure. For most local and regional small businesses, it is not.

An LLC can elect C Corp tax treatment without changing its legal structure. This gives owners flexibility to shift tax treatment as the business evolves, though the decision should never be made without a full projection of the tax impact.

How do state taxes and compliance costs affect your entity choice?

Federal tax treatment is only part of the picture. State-level taxes can significantly change the net benefit of any entity structure. State taxes sometimes apply regardless of profitability, which means an LLC that loses money in a given year may still owe the state a fee or tax.

Common state-level obligations to account for:

- Franchise taxes: Charged for the privilege of operating as a certain entity type in a state. Texas, for example, imposes a franchise tax on most business entities.

- Gross receipts taxes: Applied to total revenue, not profit. These hit businesses even in low-margin years.

- Annual report fees: Most states charge a filing fee to keep your entity in good standing.

- State income taxes: Some states tax pass-through income at rates that rival the federal savings from an S-Corp election.

Small business owners frequently overlook state franchise taxes or gross receipts taxes, which can erode the federal tax savings offered by certain entity types. A structure that saves $8,000 in federal self-employment tax may net only $5,000 after state fees are factored in.

Pro Tip: Before finalizing your entity choice, get a full state-specific tax analysis. A CPA familiar with your state’s tax code can calculate the true net savings, not just the federal number. Parr & Ibarra CPA works with Dallas-Fort Worth business owners on exactly this kind of comprehensive review.

Compliance costs also matter. S Corps require separate payroll, a corporate tax return, and ongoing bookkeeping. Those costs are real and recurring. Build them into your annual budget before assuming the entity switch is a net win.

Key Takeaways

The right business entity structure for taxes depends on your net profit, growth plans, and state-level obligations, not just the federal tax rate.

| Point | Details |

|---|---|

| Sole proprietors pay the most | All net earnings face the 15.3% self-employment tax with no structural relief. |

| S-Corp election saves at $40,000+ | Self-employment tax savings on distributions exceed compliance costs above this profit level. |

| C Corps create double taxation | Entity-level tax plus dividend tax makes C Corps costly for most small businesses. |

| State taxes reduce federal savings | Franchise and gross receipts taxes can significantly cut the net benefit of any entity choice. |

| Reasonable salary is an IRS target | S-Corp owners must set a defensible salary or risk audit, back taxes, and penalties. |

Why I tell every new client to start with their profit number

Most business owners pick an entity based on what they heard from a friend or read in a forum. That is the wrong starting point. The right question is: what is your current net profit, and what do you realistically expect in the next three years?

I have seen owners form S Corps when they were earning $25,000 a year in profit. After payroll service fees, a separate corporate return, and state franchise taxes, they paid more than they saved. The structure was technically correct but financially wrong for their stage.

The opposite mistake is just as common. A sole proprietor earning $120,000 in net profit and paying full self-employment tax on every dollar, when an S-Corp election could have saved them $9,000 or more annually. That is money left on the table every single year.

The reasonable salary issue is the one I watch most carefully. The IRS knows that S-Corp owners are incentivized to minimize salary and maximize distributions. Auditors look at industry compensation data, the owner’s role, and the business’s revenue. A $1 salary on a $500,000 revenue business is not defensible. A well-documented, industry-appropriate salary is.

Quarterly estimated tax payments are the other area where I see owners get hurt. Every entity type requires them. Missing a quarter triggers penalties that add up fast. Build the payment schedule into your calendar from day one, regardless of which structure you choose.

Tax strategy and liability protection are not separate conversations. The entity you choose affects both. An LLC gives you liability protection with pass-through taxation. An S-Corp adds payroll tax savings but requires more structure. A C-Corp protects you and opens capital markets but costs more in taxes for most small businesses. Make the decision with both lenses open.

— Adan

How Parr & Ibarra CPA helps you choose the right structure

Choosing a business entity is not a one-time decision. It is a financial strategy that should be revisited as your profit grows and your goals shift.

Parr & Ibarra CPA works with small business owners across the Dallas-Fort Worth area to run entity-specific tax projections, evaluate S-Corp election timing, and build year-round tax plans that account for both federal and state obligations. The team includes over 20 professionals, with multiple CPAs who specialize in small business tax strategy. Whether you are launching a new venture or reconsidering your current structure, the IRS tax filing guidance and personalized planning at Parr & Ibarra CPA give you a clear picture of what each choice actually costs. Visit aibarra.cpa to schedule a consultation and get a projection built around your numbers.

FAQ

What is the best business entity for reducing taxes?

For most profitable small businesses, an S-Corp election provides the strongest tax savings once net profit exceeds $40,000, by reducing self-employment tax on distributions above a reasonable salary.

Do LLCs pay self-employment tax?

Yes. Single-member and multi-member LLC owners pay self-employment tax on all net earnings by default, unless the LLC elects S-Corp tax treatment.

What is double taxation in a C Corporation?

A C Corporation pays income tax at the entity level at a 21% federal rate. Shareholders then pay personal income tax on dividends received, creating two layers of tax on the same profit.

How does the S-Corp reasonable salary rule work?

S-Corp owners who work in the business must pay themselves a salary that reflects fair market compensation for their role. The IRS audits owners who set artificially low salaries to shift income to tax-free distributions.

Do state taxes affect which business entity I should choose?

Yes. States may impose franchise taxes, gross receipts taxes, or annual fees that apply regardless of profitability. These costs can reduce or eliminate the federal tax savings from a particular entity structure, making state-specific analysis a necessary part of the decision.