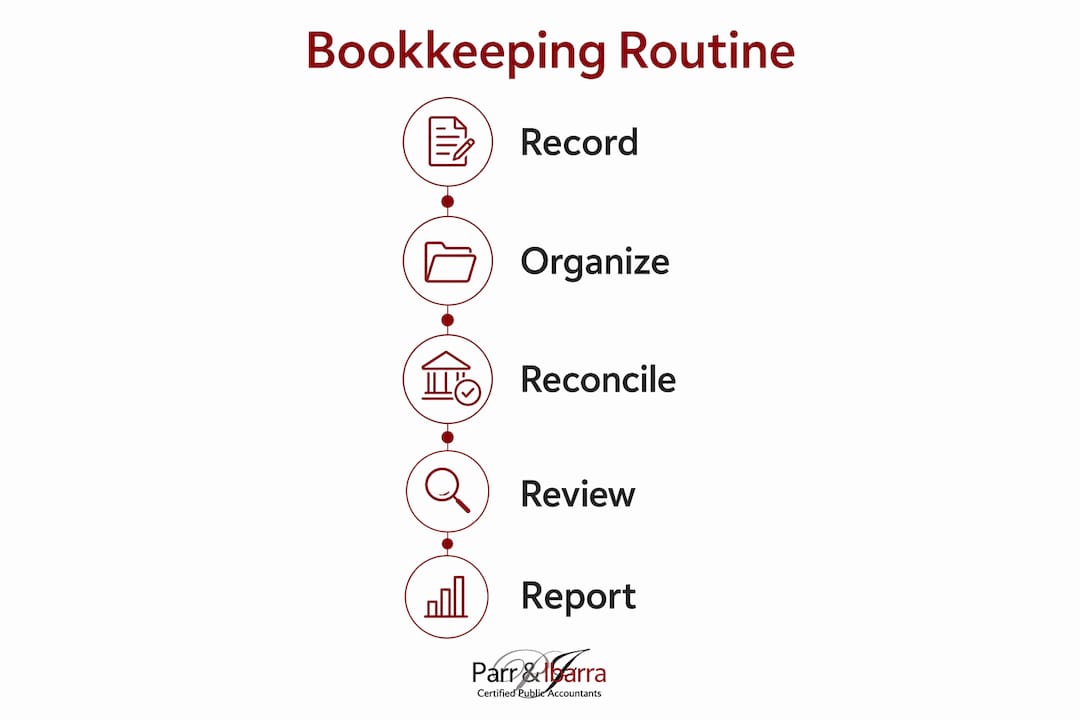

Bookkeeping is defined as the systematic process of recording, organizing, and maintaining every financial transaction a business makes. The IRS requires businesses to keep permanent records that substantiate income and expenses for tax reporting, though it prescribes no single system for doing so. Done correctly, bookkeeping gives you an accurate financial picture at any moment, supports tax compliance, and reveals whether your business is actually growing. The IRS goes further, stating that proper records correlate with more successful business outcomes by enabling progress monitoring, deductible tracking, and preparation of accurate financial statements. Bookkeeping is not accounting, though the two are closely related. Bookkeeping covers the data entry side: recording transactions, reconciling accounts, and organizing documents. Accounting builds on that foundation with analysis, tax strategy, and financial planning.

What bookkeeping tasks are essential for small business owners and freelancers?

The core of small business bookkeeping is recording every financial transaction as it happens. That means logging sales, tracking expenses, filing receipts, and categorizing each entry so your records reflect reality. Skipping even a few weeks creates a backlog that costs hours to untangle at tax time.

The essential daily and monthly tasks include:

- Recording income: Log every payment received, whether by check, card, or digital transfer. Note the date, amount, client, and payment method.

- Tracking expenses: Capture every business purchase, from software subscriptions to office supplies. Match each expense to a category like marketing, utilities, or professional services.

- Filing receipts and invoices: Store digital or physical copies of every receipt and invoice. The IRS requires receipts and supporting documents for any deduction you claim.

- Reconciling bank accounts: Compare your records against your bank statement at least once a month. Discrepancies often signal data entry errors or unauthorized charges.

- Reviewing accounts receivable: Check which invoices are unpaid and follow up on overdue accounts. Cash flow problems often start with ignored receivables.

A practical weekly workflow looks like this: spend 20–30 minutes each Friday logging that week’s transactions, filing receipts, and flagging any unusual charges. Monthly, set aside time to reconcile your bank account and review your profit and loss summary.

Pro Tip: Photograph receipts immediately with a mobile app and upload them to your records the same day. Receipts fade, and the IRS does not accept illegible documents as proof of a deduction.

How does bookkeeping differ from accounting, and why does it matter?

Bookkeeping and accounting serve different functions, and confusing the two leads to either overpaying for services you do not need or underpreparing for ones you do. Bookkeeping handles day-to-day record keeping and basic financial reporting. Accounting interprets those records, provides strategic advice, and manages complex tax services.

| Function | Bookkeeping | Accounting |

|---|---|---|

| Primary role | Recording transactions | Analyzing financial data |

| Output | Ledgers, reconciliations | Financial statements, tax returns |

| Frequency | Daily or weekly | Monthly, quarterly, or annually |

| Typical cost | Lower | Higher |

| When you need it | Always, from day one | When making major financial decisions |

Bookkeeping involves day-to-day recording and generally costs less than accounting, which focuses on financial analysis and tax strategy. That cost difference matters for freelancers and startups watching every dollar. A freelancer with straightforward income and expenses may only need a bookkeeper and a CPA at tax time. A business with employees, inventory, or multiple revenue streams benefits from ongoing accounting support year-round.

Bookkeepers handle daily record keeping and basic financial reporting, while accountants provide interpretation, strategic advice, and complex tax services. Understanding this distinction lets you hire the right professional at the right time, which controls costs without sacrificing compliance.

Pro Tip: Start with a bookkeeper or a solid bookkeeping system. Add a CPA for quarterly tax planning once your revenue grows past the point where a single annual filing feels risky.

What are the IRS requirements for recordkeeping and document retention?

The IRS sets clear expectations for what records you must keep and for how long. Failing to meet these requirements leaves you exposed during an audit and unable to substantiate deductions you have already claimed.

- Keep records as long as they are material. The IRS general rule is to retain records for at least 3 years from the date you filed the return or the due date, whichever is later. This covers the standard statute of limitations for filing a claim for credit or refund.

- Retain employment tax records for 4 years. The IRS requires employment tax records to be kept for at least 4 years after the tax is due or paid. Payroll records fall into a separate, longer retention category.

- Document all income sources. Keep bank statements, deposit slips, invoices, and sales receipts. These prove your reported income matches what actually came in.

- Document all deductible expenses. Retain receipts, canceled checks, account statements, and credit card records for every expense you deduct. The burden of proof in an audit falls on you, not the IRS.

- Store records in an organized, accessible format. Digital storage is acceptable. Use clearly labeled folders by year and category. Cloud backups protect against physical loss.

Your IRS tax filing obligations connect directly to the quality of your records. A disorganized filing system does not just slow you down at tax time. It can cost you deductions you legitimately earned because you cannot find the proof.

What methods and tools can simplify bookkeeping for small businesses?

The right system depends on your business size, transaction volume, and comfort with technology. Three main approaches exist: manual ledgers, spreadsheets, and cloud accounting software.

Manual ledgers work for very small operations with minimal transactions. They require no technology but create significant risk of human error and offer no automation.

Spreadsheets (such as Microsoft Excel or Google Sheets) give you more flexibility and are free or low cost. They work well for freelancers with simple finances but become unwieldy as transaction volume grows.

Cloud accounting software is the most practical choice for most small business owners. These platforms automate bank feeds, categorize transactions, generate reports, and integrate with payroll systems. They reduce data entry time and minimize errors.

Key features to look for in any bookkeeping system:

- Bank feed integration: Automatically imports transactions from your bank, reducing manual entry.

- Expense categorization: Tags transactions by type so your reports are accurate without extra work.

- Invoice management: Creates, sends, and tracks invoices from one place.

- Tax report generation: Produces profit and loss statements and expense summaries ready for your CPA.

- Multi-user access: Lets your bookkeeper or CPA log in without sharing your banking credentials.

Starting bookkeeping early with the right system and maintaining a consistent routine prevents time-consuming catch-ups and costly errors. The biggest mistake new business owners make is choosing no system at all and then scrambling to reconstruct a full year of records in april.

One critical rule applies regardless of which system you choose: never mix personal and business finances. Co-mingling personal and business finances increases bookkeeping time by 50–70%. A dedicated business checking account and business credit card eliminate that problem immediately.

Pro Tip: Open a dedicated business bank account before you make your first business purchase. Every dollar that flows through a single account is a dollar you do not have to sort out later.

How to maintain a bookkeeping routine that saves time and avoids errors

Consistency is the single biggest factor in effective financial record keeping. Consistent bookkeeping routines reduce errors and save time compared to catching up all at once. A monthly reconciliation typically takes 2–3 hours when records are current. It can take days when they are not.

A practical routine for small business owners and freelancers:

- Weekly (15–30 minutes): Log all transactions, upload receipts, and flag any charges that need clarification.

- Monthly (1–3 hours): Reconcile bank and credit card accounts, review your profit and loss statement, and check accounts receivable for overdue invoices.

- Quarterly: Review your financial reports for trends, estimate your quarterly tax obligations, and adjust your budget if needed.

- Annually: Compile year-end reports, organize documents for your CPA, and archive the prior year’s records.

Common bookkeeping errors to avoid:

- Skipping bank reconciliation for multiple months in a row

- Failing to record small cash purchases

- Misclassifying expenses, which distorts your profit and loss report

- Ignoring accounts receivable until cash flow becomes a crisis

- Treating bookkeeping as a once-a-year tax prep task rather than an ongoing practice

Many small businesses treat bookkeeping as an annual tax prep task. That approach leads to errors and IRS penalties that a simple monthly routine would have prevented. Treating your records as a live financial dashboard, rather than a year-end obligation, changes how you make decisions throughout the year.

Key Takeaways

Accurate bookkeeping, maintained on a consistent weekly and monthly schedule, is the foundation of tax compliance, cash flow clarity, and sound business decisions for small business owners and freelancers.

| Point | Details |

|---|---|

| Define your system early | Choose a bookkeeping method before your first transaction to avoid costly catch-ups later. |

| Separate business and personal finances | A dedicated business account reduces bookkeeping time by up to 70% and simplifies reporting. |

| Follow IRS retention rules | Keep most business records for at least 3 years; employment tax records require 4 years. |

| Maintain a weekly routine | Logging transactions weekly takes 15–30 minutes and prevents month-end backlogs. |

| Know when to add an accountant | Bookkeeping covers daily records; bring in a CPA for tax strategy, audits, and major financial decisions. |

What I’ve learned from watching business owners avoid their books

Most business owners do not avoid bookkeeping because they are lazy. They avoid it because no one ever showed them a system that actually fits their life. I have worked with freelancers who kept every receipt in a shoebox and business owners who had not reconciled their accounts in 18 months. The pattern is always the same: the longer you wait, the more it costs, both in time and in missed deductions.

The owners who get this right treat their books the way they treat their calendar. They block 20 minutes on Friday afternoon, they never skip it, and they never have a tax season crisis. The ones who struggle treat bookkeeping as something to deal with “later.” Later always arrives in a panic.

One thing I tell every client: your books are not just a compliance tool. They are the clearest signal you have about whether your business is actually working. A profit and loss statement reviewed monthly tells you which services are profitable, which clients cost you money, and whether you can afford to hire. That information is worth far more than the time it takes to maintain it.

If you are a freelancer just starting out, the bar is low. A dedicated bank account, a simple spreadsheet or entry-level software, and 20 minutes a week will keep you in good shape. As your business grows, the system needs to grow with it. That is when a professional bookkeeper or a firm like Parr & Ibarra CPA becomes worth every dollar.

— Adan

Parr & Ibarra CPA: bookkeeping support built for small businesses

Parr & Ibarra CPA works with small business owners and freelancers across the Dallas-Fort Worth area who need more than a once-a-year tax filing. The firm’s bookkeeping services are integrated with payroll support, proactive tax planning, and CFO advisory, so your financial records connect directly to your broader business strategy.

The team at Parr & Ibarra CPA includes over 20 professionals, with multiple CPAs who specialize in the financial challenges that small business owners face year-round. Whether you need help setting up a system from scratch, catching up on months of disorganized records, or preparing for an IRS audit, the firm provides hands-on support tailored to your situation. Review the IRS tax filing guide to understand what your records need to cover, then reach out to Parr & Ibarra CPA to put the right system in place.

FAQ

What is bookkeeping, exactly?

Bookkeeping is the process of recording, organizing, and maintaining a business’s financial transactions on a regular basis. It provides the accurate financial data needed for tax compliance and business decision-making.

How long does the IRS require you to keep business records?

The IRS requires most business records to be kept for at least 3 years from the filing date. Employment tax records must be retained for at least 4 years after the tax is due or paid.

Do I need a bookkeeper or an accountant?

Bookkeepers handle daily transaction recording and basic reporting, while accountants provide financial analysis, tax strategy, and complex filings. Most small businesses benefit from both, starting with a bookkeeper and adding a CPA as revenue and complexity grow.

How often should I update my books?

Logging transactions weekly and reconciling accounts monthly is the most effective routine for small business owners. This approach takes 2–3 hours per month when maintained consistently and prevents costly year-end errors.

Can I do my own bookkeeping as a freelancer?

Yes. Freelancers with straightforward income and expenses can manage their own records using a spreadsheet or entry-level cloud accounting software. The key requirements are a dedicated business bank account, consistent weekly logging, and organized document storage.