Tax planning is the year-round process of making deliberate financial decisions to reduce what you owe the IRS and keep more of what you earn. It is not the same as filing your taxes. Tax filing is backward-looking compliance; tax planning is a forward-looking strategy that shapes your financial outcomes before the deadline arrives. Business owners and individuals who treat these two activities as one consistently pay more than they should. The decisions you make in january, april, and september matter far more than anything you do in march when the clock is running out.

What are the essential tax planning strategies for individuals and business owners?

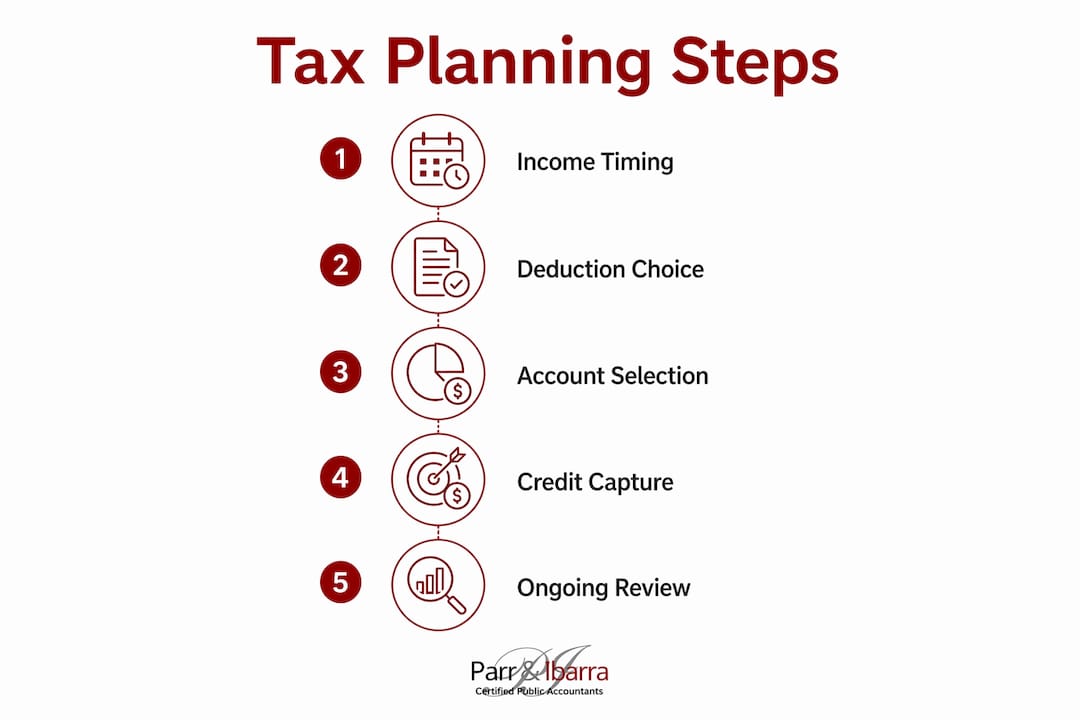

The four pillars of effective tax management are income timing, deduction optimization, account selection, and credit capture. Each one gives you a lever to pull before the tax year closes. Miss any of them and you leave money on the table.

Income timing means controlling when you receive or recognize income. A self-employed consultant who delays invoicing a december project until january pushes that income into the next tax year. A business owner who accelerates deductible expenses into the current year reduces this year’s taxable income. Both moves are legal, deliberate, and worth planning months in advance.

Deduction optimization starts with one decision: standard deduction or itemizing. The IRS sets the standard deduction each year, and most people take it without checking whether itemizing would save them more. Keeping tax records for at least 3 years gives you the documentation to defend itemized deductions if the IRS asks. If your deductible expenses fall just below the standard deduction threshold, charitable bunching can push you over it. Bunching means combining two years of charitable donations into one calendar year, then taking the standard deduction the next year.

Donating appreciated stock instead of cash is one of the most underused moves in individual tax advice. Donating appreciated stocks lets you deduct the full market value while avoiding capital gains tax on the appreciation. That dual benefit can yield significantly more value than selling the stock and donating the cash proceeds.

Account selection determines how much of your investment growth the IRS can touch. Contributions to a 401(k) or traditional IRA reduce your taxable income now. A Roth IRA or Roth 401(k) does the opposite: you pay tax now and withdraw tax-free later. Health Savings Accounts (HSAs) offer a triple tax benefit: contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Credit capture beats deductions dollar for dollar. A $1,000 tax credit reduces your bill by $1,000. A $1,000 deduction reduces your bill by $1,000 multiplied by your marginal rate, which is always less. Business owners should audit available credits annually, including the R&D credit, energy efficiency credits, and credits tied to hiring.

Pro Tip: A $5,000 tax savings invested over 20 years can grow to $200,000 or more. Multi-year planning compounds your results in ways that single-year thinking never will.

How does ongoing monitoring and adjustment improve tax planning effectiveness?

Most tax surprises are preventable. Proactive mid-year adjustments prevent large year-end bills and penalties far more reliably than any last-minute filing tactic. Waiting until december to review your tax position is like checking your GPS after you’ve already missed the exit.

The IRS requires quarterly estimated tax payments on four deadlines each year: april 15, june 16, september 15, and january 15. Missing these deadlines triggers underpayment penalties even if you pay your full balance when you file. The fix is straightforward once you know the rule.

Here is how to stay on track throughout the year:

- Calculate your prior year tax liability in january. This is your baseline. The IRS safe harbor rule says you avoid underpayment penalties by paying at least 100% of last year’s tax, or 110% if your prior year adjusted gross income exceeded $150,000.

- Review your income projection in april. Compare actual income to your projection. If income is running higher than expected, increase your june estimated payment.

- Update your W-4 in june or july. Employees who receive a bonus, start a side business, or change jobs mid-year often end up under-withheld. A mid-year W-4 update corrects the trajectory before year-end.

- Run a tax projection in october. This is your last real opportunity to make moves. You can still max out retirement contributions, harvest investment losses, and time deductible expenses.

- Finalize year-end moves in november and december. Execute the decisions from your october projection. Do not wait until january to act on december opportunities.

Pro Tip: Treat your tax projection like a cash flow forecast. Knowing your estimated liability in october gives you 60 days to fund retirement accounts, make charitable contributions, and adjust withholding before the year closes.

The most common mistake business owners make is treating tax as a once-a-year event. A quarterly review with a CPA takes less than an hour and consistently produces better outcomes than a frantic year-end scramble.

What role do tax-advantaged accounts and investment decisions play in effective tax planning?

Tax-advantaged accounts are the most reliable tools for reducing taxable income year after year. The IRS sets contribution limits annually, and those limits represent real money you can shelter from current taxation.

Comparing key account types

| Account | Tax treatment on contributions | Tax treatment on growth | Tax treatment on withdrawals |

|---|---|---|---|

| Traditional 401(k) | Pre-tax (reduces current income) | Tax-deferred | Taxed as ordinary income |

| Roth 401(k) | After-tax (no current deduction) | Tax-free | Tax-free (qualified) |

| Traditional IRA | Pre-tax (income limits apply) | Tax-deferred | Taxed as ordinary income |

| Roth IRA | After-tax (income limits apply) | Tax-free | Tax-free (qualified) |

| HSA | Pre-tax | Tax-free | Tax-free (medical expenses) |

Roth 401(k) conversions and strategic contribution timing are advanced tools that manage future tax liabilities, not just current ones. A Roth conversion makes the most sense in a year when your income is temporarily lower, such as a business transition year or early retirement. You pay tax on the converted amount now and lock in tax-free growth for decades.

Investment decisions inside taxable accounts also carry significant tax consequences. The two most powerful techniques are:

- Tax-loss harvesting: Selling investments at a loss to offset capital gains elsewhere in your portfolio. You can also offset up to $3,000 of ordinary income per year with net capital losses.

- Asset location: Placing tax-inefficient investments (like bonds or REITs) inside tax-deferred accounts and tax-efficient investments (like index funds) inside taxable accounts. This reduces the drag of annual taxable distributions.

Catch-up contributions are available to individuals aged 50 and older. They allow additional contributions above the standard limit to 401(k)s and IRAs. For high-income earners approaching retirement, maxing out catch-up contributions is one of the highest-return moves available in a given tax year.

Pro Tip: Check your capital gains tax exposure before december 31. Harvesting losses before year-end can offset gains you’ve already realized and reduce your bill without changing your long-term investment strategy.

How should business owners integrate tax planning into their operational decisions?

Tax strategy belongs in the boardroom, not just the accounting department. Business tax leaders must have a seat at the table to influence deal structures, cash flow decisions, and business model choices before they are locked in. A business owner who structures a sale, acquisition, or partnership without tax input often discovers the cost of that oversight at filing time.

The most impactful areas where tax strategy intersects with business operations include:

- Deal structuring: Whether a transaction is structured as an asset sale or a stock sale changes the tax outcome for both buyer and seller. Tax input before a letter of intent is signed can save six figures.

- Expense timing: Accelerating deductible expenses into the current year or deferring income to the next year are decisions that require coordination between operations, finance, and tax.

- Entity structure: S-corps, C-corps, LLCs, and sole proprietorships each carry different tax treatment. Reviewing your entity structure annually ensures you are not overpaying due to an outdated setup.

- Payroll tax planning: Business owners who pay themselves a salary from an S-corp must set a reasonable compensation level. Getting this wrong triggers IRS scrutiny. Understanding your payroll tax obligations is a non-negotiable part of business tax optimization.

Coordinating tax with finance and IT during digital transformation is increasingly critical. Businesses that adopt new software, change revenue recognition methods, or expand into new states create new tax obligations. Catching these early costs far less than correcting them after the fact.

Pro Tip: Before any major business decision, ask one question: what are the tax implications? Involving your CPA at the planning stage of a merger, expansion, or ownership change costs a fraction of what it costs to unwind a tax-inefficient structure after closing. See how taxes affect M&A decisions before you sign anything.

Key Takeaways

Effective tax planning requires year-round decisions across income timing, account selection, deduction optimization, and credit capture to consistently reduce tax liability and build after-tax wealth.

| Point | Details |

|---|---|

| Plan year-round, not at filing | Decisions made throughout the year produce the biggest tax savings. |

| Use the safe harbor rule | Pay 100% (or 110% if income exceeds $150,000) of prior year tax to avoid penalties. |

| Max out tax-advantaged accounts | 401(k)s, Roth IRAs, and HSAs shelter income and reduce taxable growth. |

| Involve tax expertise in business decisions | Deal structure, entity type, and expense timing all carry major tax consequences. |

| Harvest losses before year-end | Offsetting capital gains with losses reduces your bill without changing long-term strategy. |

Why reactive tax filing costs you more than you think

Most people I work with come in having filed their taxes faithfully for years. They are not doing anything wrong. They are just doing the minimum. Filing is compliance. Planning is the part that actually changes your financial outcome.

The biggest misconception I see is that tax planning is only for wealthy people or large corporations. That is wrong. A self-employed graphic designer, a restaurant owner with three locations, and a dual-income household with a rental property all have meaningful planning opportunities that a standard filing workflow will never surface. The difference between a client who plans and one who just files is often thousands of dollars per year, compounded over a career.

Procrastination is the single most expensive tax habit I encounter. Business owners who wait until march to think about the prior year have already lost every opportunity that existed in october, november, and december. The IRS does not give refunds for missed planning windows.

Technology has made year-round monitoring far more accessible than it was a decade ago. Real-time bookkeeping, automated payroll, and quarterly projection tools mean there is no longer a good excuse for being caught off guard at filing time. The clients who get the best outcomes are the ones who treat their CPA as a year-round partner, not a seasonal vendor.

— Adan

How Parr & Ibarra CPA approaches tax planning for you

Parr & Ibarra CPA works with business owners and individuals in the Dallas-Fort Worth area who want more than a tax return. The team of over 20 professionals, including multiple CPAs, builds year-round tax strategies that cover estimated payments, deduction planning, retirement account timing, and business structure reviews.

Whether you are a first-time business owner figuring out quarterly payments or an established operator preparing for a major transaction, Parr & Ibarra CPA brings the same depth of expertise to every engagement. Start with the 2026 IRS tax filing guide to understand your obligations, then connect with the team for a personalized strategy session. You can also review critical tax deadlines to make sure nothing slips through the cracks this year.

FAQ

What is tax planning, exactly?

Tax planning is the proactive process of making financial decisions throughout the year to legally reduce your tax liability. It is distinct from tax filing, which records what already happened.

How often should I review my tax strategy?

A quarterly review is the industry standard. Reviewing in April, June, September, and December aligns with IRS estimated payment deadlines and gives you time to act on findings.

What is the safe harbor rule for estimated taxes?

The safe harbor rule lets you avoid underpayment penalties by paying at least 100% of your prior year tax liability, or 110% if your prior year adjusted gross income exceeded $150,000.

Which tax-advantaged accounts should I prioritize?

Max out your HSA first if you are eligible, then your 401(k) up to the employer match, then your IRA. The HSA’s triple tax benefit makes it the most tax-efficient account available.

When should a business owner involve a CPA in a business decision?

Before any major decision, including hiring, acquiring a business, changing your entity structure, or expanding to a new state. Tax implications identified early cost far less to address than those discovered after the fact.